Download to read offline

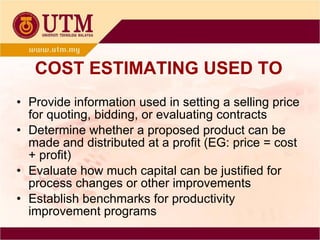

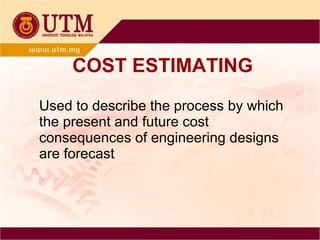

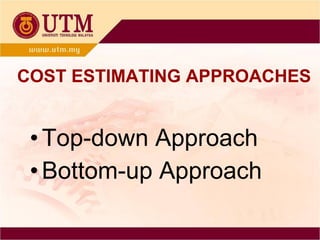

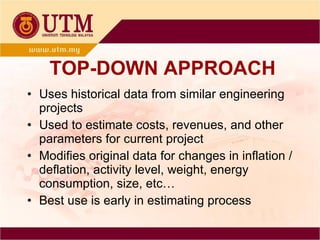

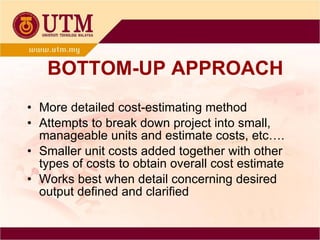

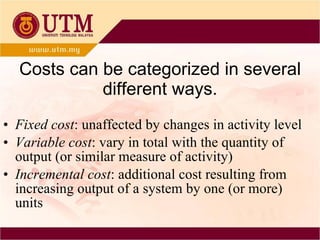

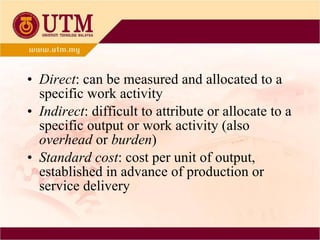

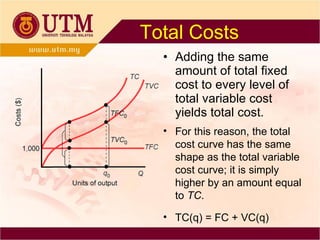

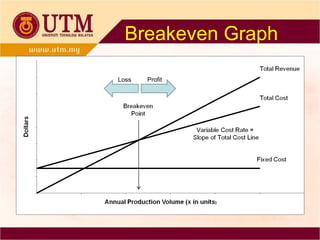

Cost estimating is used to determine the price of a product, evaluate capital investments, and establish benchmarks for productivity. There are two main approaches - top-down uses historical data from similar projects while bottom-up breaks down costs into small units. Costs can be categorized as fixed, variable, incremental, direct, indirect and more. Standard costs represent established costs per unit while life-cycle costs consider all costs over a product's lifespan. Breakeven analysis determines the sales volume needed for total revenue to equal total costs.