Downloaded 42 times

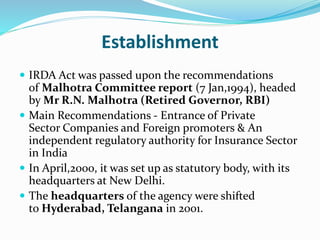

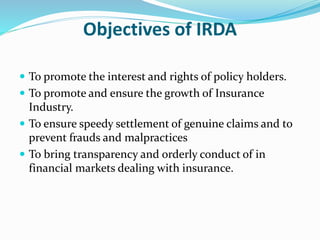

IRDA is the statutory, independent body that governs and supervises the insurance industry in India. It was established in 2000 by the Insurance Regulatory and Development Authority Act, 1999. IRDA regulates the insurance industry, issues licenses, protects policyholders, and promotes growth of the insurance sector. It aims to ensure speedy settlement of claims, prevent fraud and malpractices, and bring transparency to the insurance market. The organization is headed by a Chairman and has 10 members. IRDA seeks to balance effective regulation with ensuring the development of the insurance industry in India.