Download as PDF, PPTX

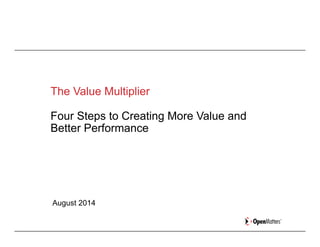

![21%

21%

19%

15%

14%

Our

CEO

sets

a

clear

vision

for

digital

in

our

business

We

have

the

right

people

to

define

our

digital

strategy

We

have

the

necessary

technology

to

execute

our

digital

strategy

We

have

the

necessary

people

and

skill

to

execute

our

digital

strategy

We

have

the

necessary

processes

to

execute

our

digital

strategy

“Assessing

your

organiza-on’s

digital

readiness,

how

much

do

you

agree

with

the

following

statements?”

(8,

9,

or

10

on

a

scale

of

1

[completely

disagree]

to

10

[

completely

agree])

Base: 1,254 executives in companies with 250 or more employees

*Forrester/Russell

Reynolds

2014

Digital

Business

Survey

But, Forrester Research says few companies are ready](https://image.slidesharecdn.com/valuemultipliercurriculum081014-140811060240-phpapp02/85/Increase-Your-Company-s-Value-Use-the-Value-Multiplier-6-320.jpg)

The document discusses how business models are disrupted by technological revolutions. It outlines four major revolutions: the Industrial Revolution, Services Revolution, Information Revolution, and current Digital Revolution. Each revolution shifts the focus of businesses and requires new financial and operating measures. The Digital Revolution in particular is built upon networks and relationships rather than assets. It favors models where many producers make and sell goods rather than centralized production models. However, the document notes most companies still lack readiness for digital transformation.