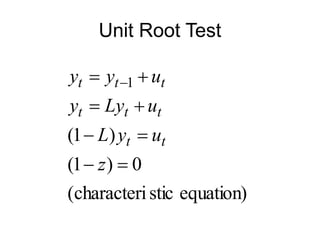

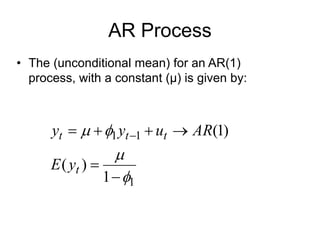

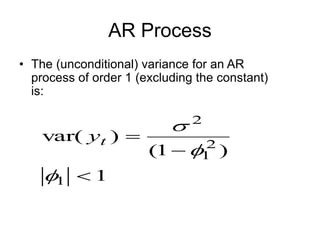

The document discusses ARIMA modeling and forecasting, emphasizing the importance of stationarity in the autoregressive (AR) process and the Box-Jenkins methodology for model identification and estimation. It outlines various forecasting types and methods to evaluate forecast accuracy, including metrics like Mean Squared Error (MSE) and financial loss functions related to sign predictions. Ultimately, the effectiveness of AR models is judged by their ability to forecast and the stability of the series based on its stationarity.

![ARIMA Models - [Lab 3]](https://cdn.slidesharecdn.com/ss_thumbnails/ydqcxn5vtqizjoun2as1-signature-e1de5ad681d661531c2467ca0d3e475440809ccfdbcb78c5369a1bb749945888-poli-141230090527-conversion-gate01-thumbnail.jpg?width=640&height=640&fit=bounds)