Download to read offline

![This talk will draw on four papers:

[CDG]. “Pareto e¢ ciency for the concave order and mul-

tivariate comonotonicity”. Guillaume Carlier, Alfred Gali-

chon and Rose-Anne Dana. Journal of Economic Theory,

2012.

[CGH] “"Local Utility and Multivariate Risk Aversion”.

Arthur Charpentier, Alfred Galichon and Marc Henry.

Mimeo.

[GH] “Dual Theory of Choice under Multivariate Risks”.

Alfred Galichon and Marc Henry. Journal of Economic

Theory, forthcoming.

[EGH] “Comonotonic measures of multivariate risks”. Ivar

Ekeland, Alfred Galichon and Marc Henry. Mathematical

Finance, 2011.](https://image.slidesharecdn.com/galichonjds-120525080009-phpapp02/85/Galichon-jds-2-320.jpg)

![By the rearrangement inequality (Hardy-Littlewood),

n

X n

X

max xiy (i) = xi y i :

permutation

i=1 i=1

More generally, X and Y are comonotonic if and only if

h i

~

max E X Y = E [XY ] :

~

Y =d Y](https://image.slidesharecdn.com/galichonjds-120525080009-phpapp02/85/Galichon-jds-5-320.jpg)

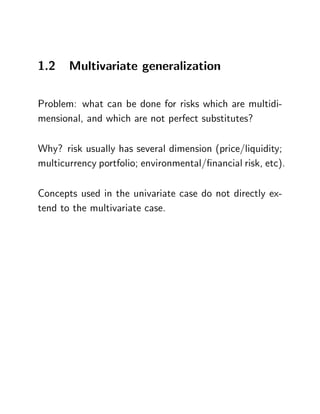

![Example. Consider

! !1 !2

P (! ) 1=2 1=2

X (! ) +1 1

Y (! ) +2 2

~

Y (! ) 2 +2

X and Y are comonotone.

~

Y has the same distribution as Y but is not comonotone

with X .

One has

h i

E [XY ] = 2 > ~

2 = E XY :](https://image.slidesharecdn.com/galichonjds-120525080009-phpapp02/85/Galichon-jds-6-320.jpg)

![Hardy-Littlewood inequality. The probability space is

now [0; 1]. Assume U (t) = (t), where is nonde-

creasing.

Let P a probability distribution, and let

X (t) = FP 1(t):

~ ~

For X : [0; 1] ! R a r.v. such that X P , one has

Z 1 h i

1 ~

E [XU ] = (t)FP (t)dt E XU :

0

Thus, letting

Z 1 n o

1 ~ ~

%( X ) = (t)FX (t)dt = max E[XU ]; X =d X

0 n o

~ ~

= max E[X U ]; U =d U :](https://image.slidesharecdn.com/galichonjds-120525080009-phpapp02/85/Galichon-jds-7-320.jpg)

![A geometric characterization. Let be an absolutely

continuous distribution; two random variables X and Y

are comonotone if for some random variable U , we

have

n o

~

~ ~

U 2 argmaxU E[X U ]; U , and

n o

~

~ ~

U 2 argmaxU E[Y U ]; U :

Geometrically, this means that X and Y have the same

projection of the equidistribution class of =set of r.v.

with distribution .](https://image.slidesharecdn.com/galichonjds-120525080009-phpapp02/85/Galichon-jds-8-320.jpg)

![The variational characterization given above will be the

basis for the generalized notion of comonotonicity given

in [EGH].

De…nition ( -comonotonicity). Let be an atomless

probability measure on Rd. Two random vectors X and

Y in L2 are called -comonotonic if for some random

d

vector U , we have

n o

~

~

U 2 argmaxU E[X U ]; ~

U , and

n o

~

U 2 argmax ~ E[Y U ]; ~

U

U

equivalentely:

X and Y are -comonotonic if there exists two convex

functions V1 and V2 and a random variable U such

that

X = rV1 (U )

Y = rV2 (U ) :

Note that in dimension 1, this de…nition is consistent with

the previous one.](https://image.slidesharecdn.com/galichonjds-120525080009-phpapp02/85/Galichon-jds-10-320.jpg)

![Monge-Kantorovich problem and Brenier theorem

Let and P be two probability measures on Rd with

second moments, such that is absolutely continuous.

Then

sup E [hU; Xi]

U ;X P

where the supremum is over all the couplings of and P if

attained for a coupling such that one has X = rV (U )

almost surely, where V is a convex function Rd ! R

which happens to be the solution of the dual Kantorovich

problem

Z Z

inf V (u) d (u) + W (x) dP (x) :

V (u)+W (x) hx;ui

Call QP (u) = rV (u) the -quantile of distribution P .](https://image.slidesharecdn.com/galichonjds-120525080009-phpapp02/85/Galichon-jds-11-320.jpg)

![Comonotonicity and transitivity.

Puccetti and Scarsini (2010) propose the following de…n-

ition of comonotonicity, called c-comonotonicity: X and

Y are c-comonotone if and only if

n o

~

~ ~

Y 2 argmaxY E[X Y ]; Y Y

or, equivalently, i¤ there exists a convex function u such

that

Y 2 @u (X )

that is, whenever u is di¤erentiabe at X ,

Y = ru (X ) :

However, this de…nition is not transitive: if X and Y are

c-comonotone and Y and Z are c-comonotone, and if the

distributions of X , Y and Z are absolutely continuous,

then X and Z are not necessarily c-comonotome.

This transivity (true in dimension one) may however be

seen as desirable.](https://image.slidesharecdn.com/galichonjds-120525080009-phpapp02/85/Galichon-jds-12-320.jpg)

![Importance of . In dimension one, one recovers the

classical notion of comotonicity regardless of the choice of

. However, in dimension greater than one, the comonotonic-

ity relation crucially depends on the baseline distribution

, unlike in dimension one. The following lemma from

[EGH] makes this precise:

Lemma. Let and be atomless probability measures

on Rd. Then:

- In dimension d = 1, -comonotonicity always implies

-comonotonicity.

- In dimension d 2, -comonotonicity implies -comonotonicity

if and only if = T # for some location-scale transform

T (u) = u + u0 where > 0 and u0 2 Rd. In other

words, comonotonicity is an invariant of the location-

scale family classes.](https://image.slidesharecdn.com/galichonjds-120525080009-phpapp02/85/Galichon-jds-14-320.jpg)

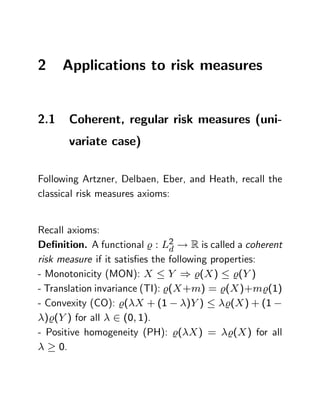

![De…nition. % : L2 ! R is called a regular risk measure

if it satis…es:

~

- Law invariance (LI): %(X ) = %(X ) when X X . ~

- Comonotonic additivity (CA): %(X + Y ) = %(X ) +

%(Y ) when X; Y are comonotonic, i.e. weakly increasing

transformation of a third randon variable: X = 1 (U )

and Y = 2 (U ) a.s. for 1 and 2 nondecreasing.

Result (Kusuoka, 2001). A coherent risk measure % is

regular if and only if for some increasing and nonnegative

function on [0; 1], we have

Z 1

%(X ) := (t)FX 1(t)dt;

0

where FX denotes the cumulative distribution functions

of the random variable X (thus QX (t) = FX 1(t) is the

associated quantile).

% is called a Spectral risk measure. For reasons explained

later, also called Maximal correlation risk measure.](https://image.slidesharecdn.com/galichonjds-120525080009-phpapp02/85/Galichon-jds-16-320.jpg)

![A representation result.

The following result is given in [EGH].

Theorem. The following propositions about the func-

tional % on L2 are equivalent:

d

(i) % is a strongly coherent risk measure;

(ii) % is a max correlation risk measure, namely there

exists U 2 L2 , such that for all X 2 L2 ,

d d

n o

~ ~

%(X ) = sup E[U X ] : X X ;

(iii) There exists a convex function V : Rd ! R such

that

%(X ) = E [U rV (U )]](https://image.slidesharecdn.com/galichonjds-120525080009-phpapp02/85/Galichon-jds-21-320.jpg)

![3 Application to e¢ cient risk-sharing

Consider a risky payo¤ X (for now, univariate) to be

shared between 2 agents 1 and 2, so that in each contin-

gent state:

X = X1 + X2

X1 and X2 are said to form an allocation of X.

Agents are risk averse in the sense of stochastic domi-

nance: Y is preferred to X if every risk-averse expected

utility decision maker prefers Y to X:

X cv Y i¤ E[u(X )] E[u(Y )] for all concave u

Agents are said to have concave order preferences. These

are incomplete preferences: it can be impossible to rank

X and Y.](https://image.slidesharecdn.com/galichonjds-120525080009-phpapp02/85/Galichon-jds-23-320.jpg)

![“better”states of the world, every agent should be better

of than in “worse” state of the world – otherwise there

would be some mutually agreeable transfer.

This leads to the concept of comonotone allocations. The

precise connection with stochastic dominance is due to

Landsberger and Meilijson (1994). Comonotonicity has

received a lot of attention in recent years in decision the-

ory, insurance, risk management, contract theory, etc.

(Landsberger and Meilijson, Ruschendorf, Dana, Jouini

and Napp...).

Theorem (Landsberger and Meilijson). Any allocation

of X is dominated by a comonotone allocation. More-

over, this dominance can be made strict unless X is al-

ready comonotone. Hence the set of e¢ cient allocations

of X coincides with the set of comonotone allocations.

This result generalizes well to the multivariate case. Up

to technicalities (see [CDG] for precise statement), ef-

…cient allocations of a random vector X is the set of](https://image.slidesharecdn.com/galichonjds-120525080009-phpapp02/85/Galichon-jds-25-320.jpg)

![The following result is from Landsberger and Meilijson

(1994):

Proposition (Landsberger and Meilijson). A random

variable X has Bickel-Lehmann less dispersed distribution

than a random variable Y if and only i¤ there exists Z

comonotonic with X such that Y =d X + Z .

The concept of -comonotonicity allows to generalize this

notion to the multivariate case as done in [CGH].

De…nition. A random vector X is called -Bickel-Lehmann

less dispersed than a random vector Y , denoted X % BL

Y , if there exists a convex function V : Rd ! R such

that the -quantiles QX and QY of X and Y satisfy

QY (u) QX (u) = rV (u) for -almost all u 2 [0; 1]d.

As de…ned above, -Bickel-Lehmann dispersion de…nes a

transitive binary relation, and therefore an order. Indeed,

if X % BL Y and Y % BL Z , then QY (u) QX (u) =](https://image.slidesharecdn.com/galichonjds-120525080009-phpapp02/85/Galichon-jds-28-320.jpg)

![rV (u) and QZ (u) QY (u) = rW (u). Therefore,

QZ (u) QX (u) = r(V (u) + W (u)) so that X % BL

Z . When d = 1, this de…nition simpli…es to the classical

de…nition.

[CGH] propose the following generalization of the Landsberger-

Meilijson characterization .

Theorem. A random vector X is -Bickel-Lehmann less

dispersed than a random vector Y if and only if there

exists a random vector Z such that:

(i) X and Z are -comonotonic, and

(ii) Y =d X + Z .](https://image.slidesharecdn.com/galichonjds-120525080009-phpapp02/85/Galichon-jds-29-320.jpg)

This document discusses the generalization of comonotonicity to multivariate risks. [1] Comonotonicity in one dimension means two risks are maximally correlated through a common underlying risk factor. The document explores generalizing this concept to multiple dimensions when risks have several components. [2] -Comonotonicity is introduced as a generalization where two multivariate risks are -comonotonic if they can be expressed as functions of a common underlying risk vector through convex functions. [3] -Comonotonicity reduces to classical comonotonicity in one dimension but depends on the baseline distribution - in higher dimensions. Applications to risk measures and efficient risk sharing are discussed.