Download as PDF, PPTX

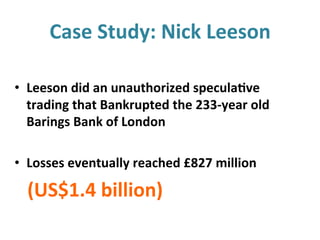

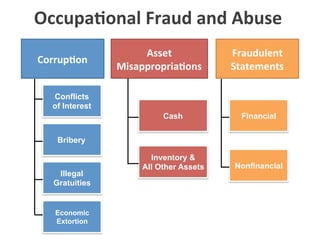

This document summarizes a fraud awareness workshop presented by Iyad Mourtada. The workshop covered case studies of occupational fraud, including Nick Leeson whose unauthorized speculative trading bankrupted Barings Bank. It discussed lessons learned around controls, monitoring, and segregation of duties. It defined fraud and internal controls, and examined the roles and responsibilities in maintaining controls. It also looked at different types of fraud schemes, how fraud is committed and detected, profiles of fraud perpetrators, and the certification process for becoming a Certified Fraud Examiner.