Download to read offline

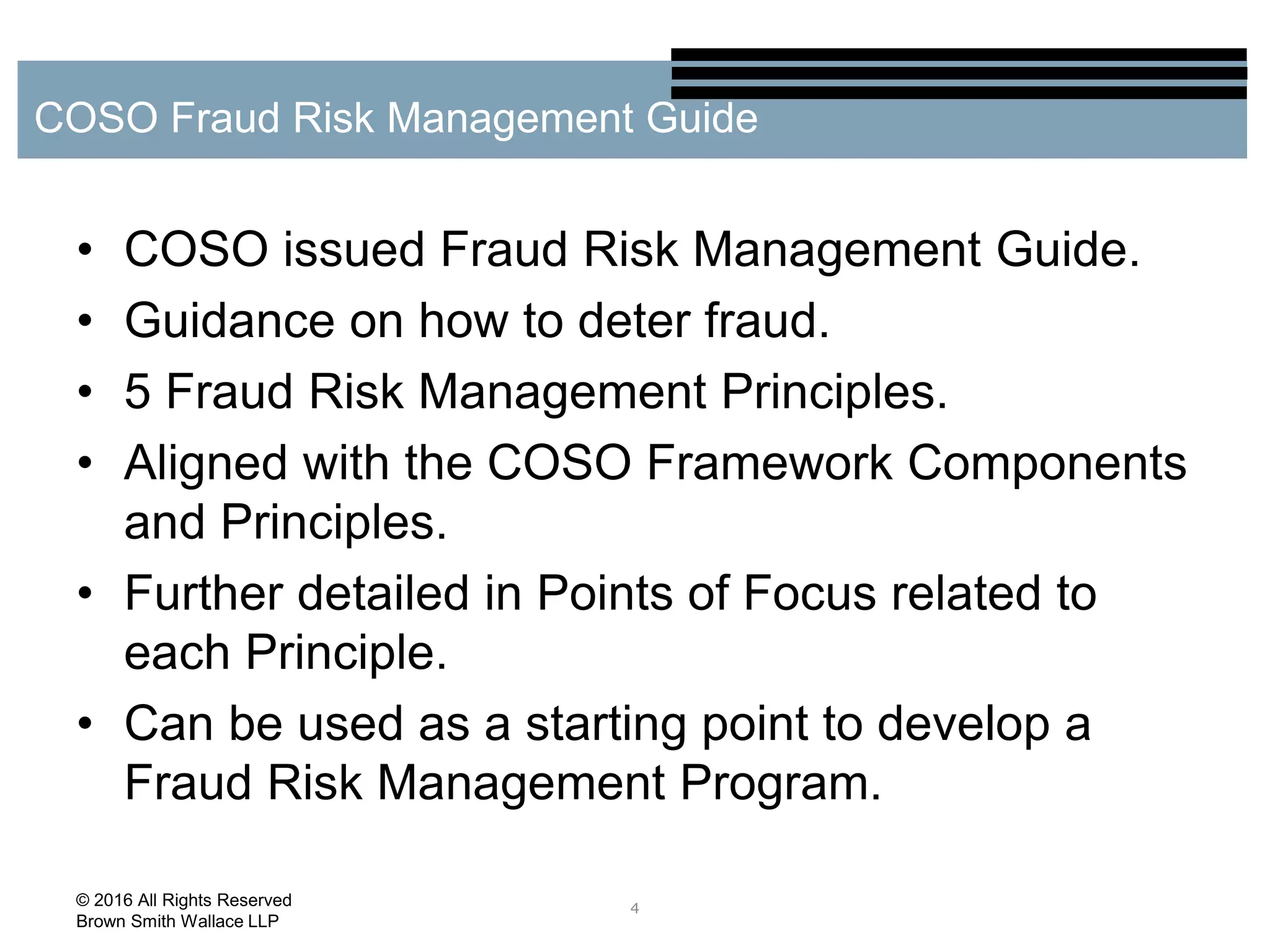

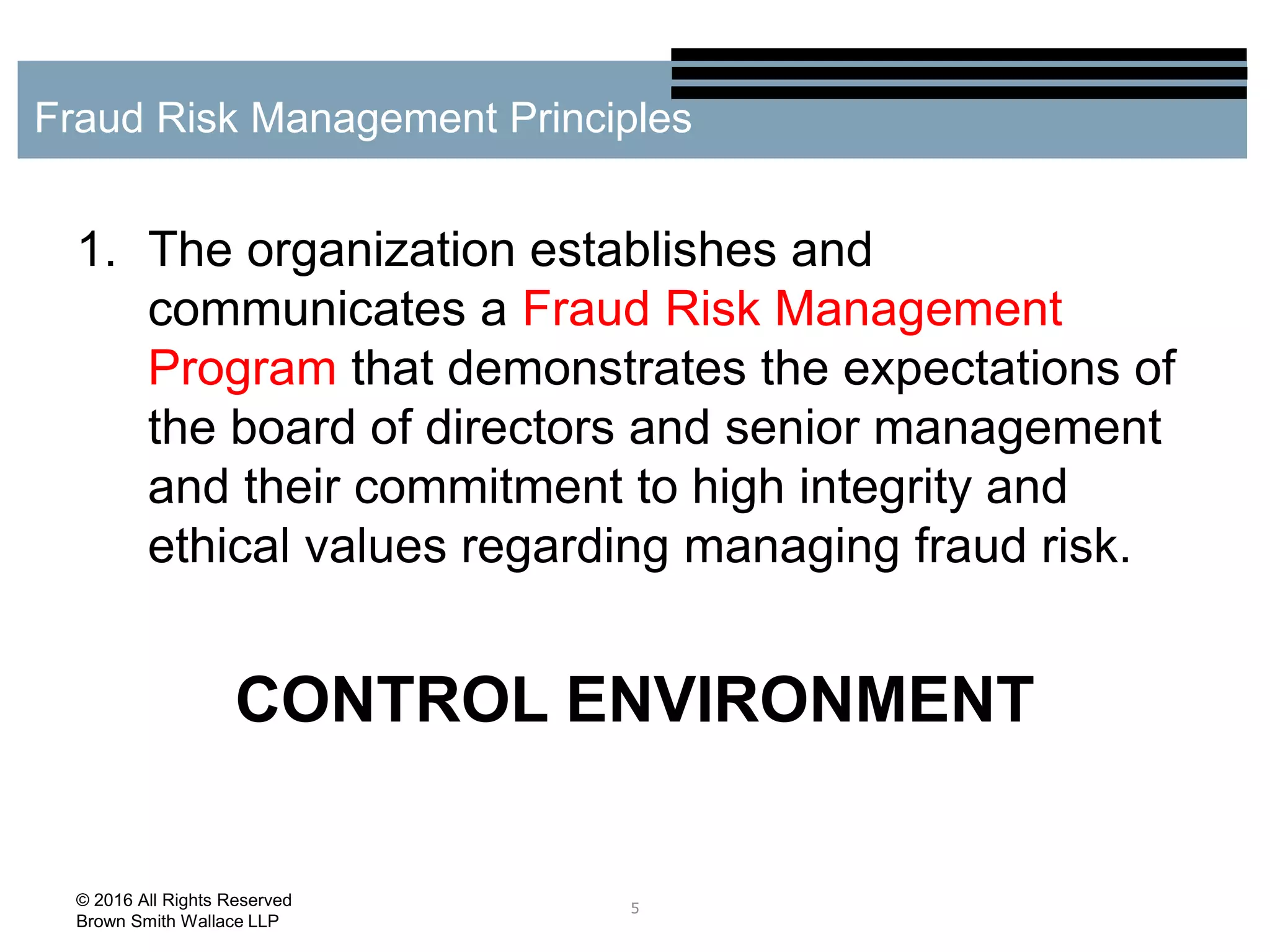

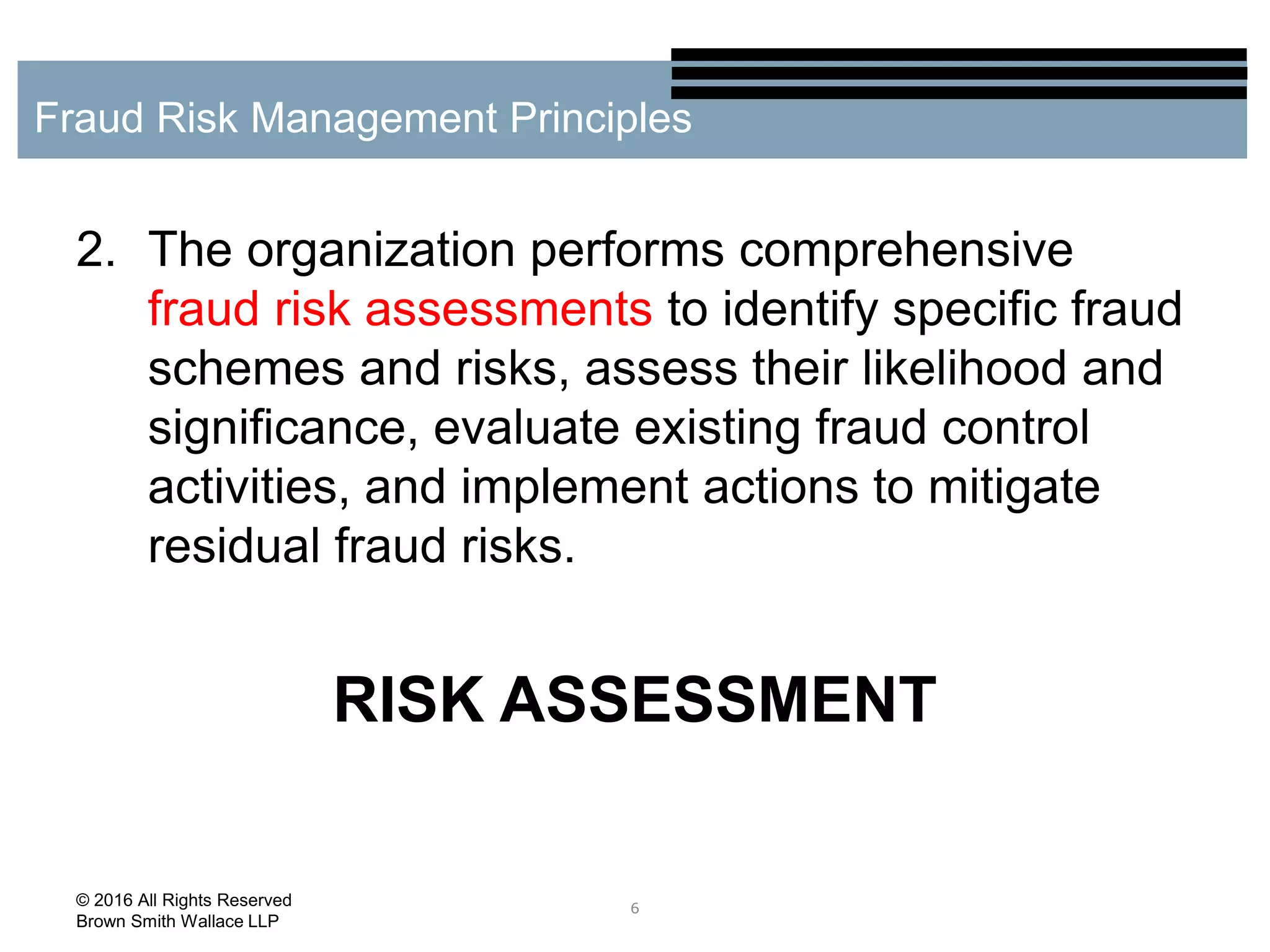

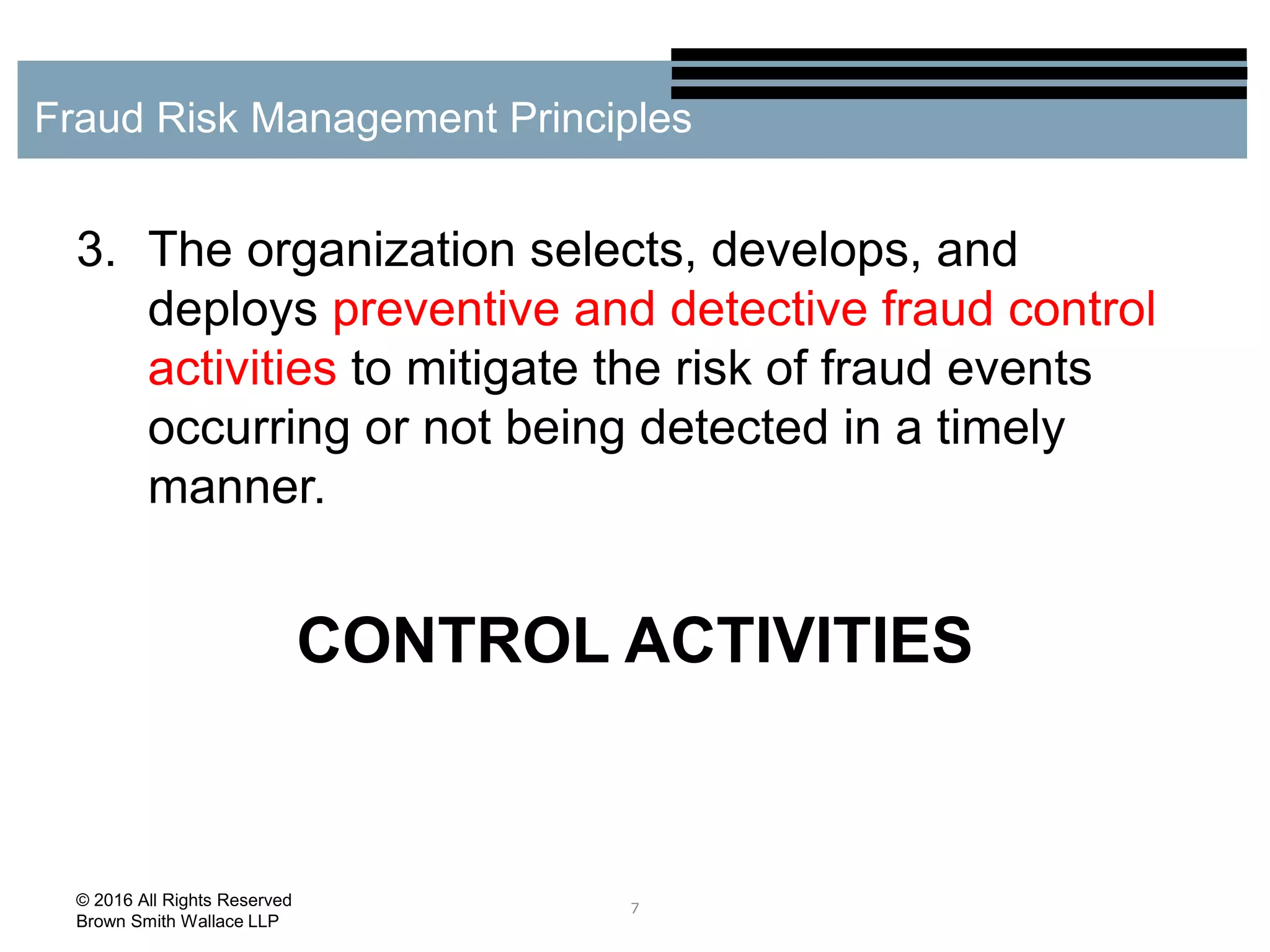

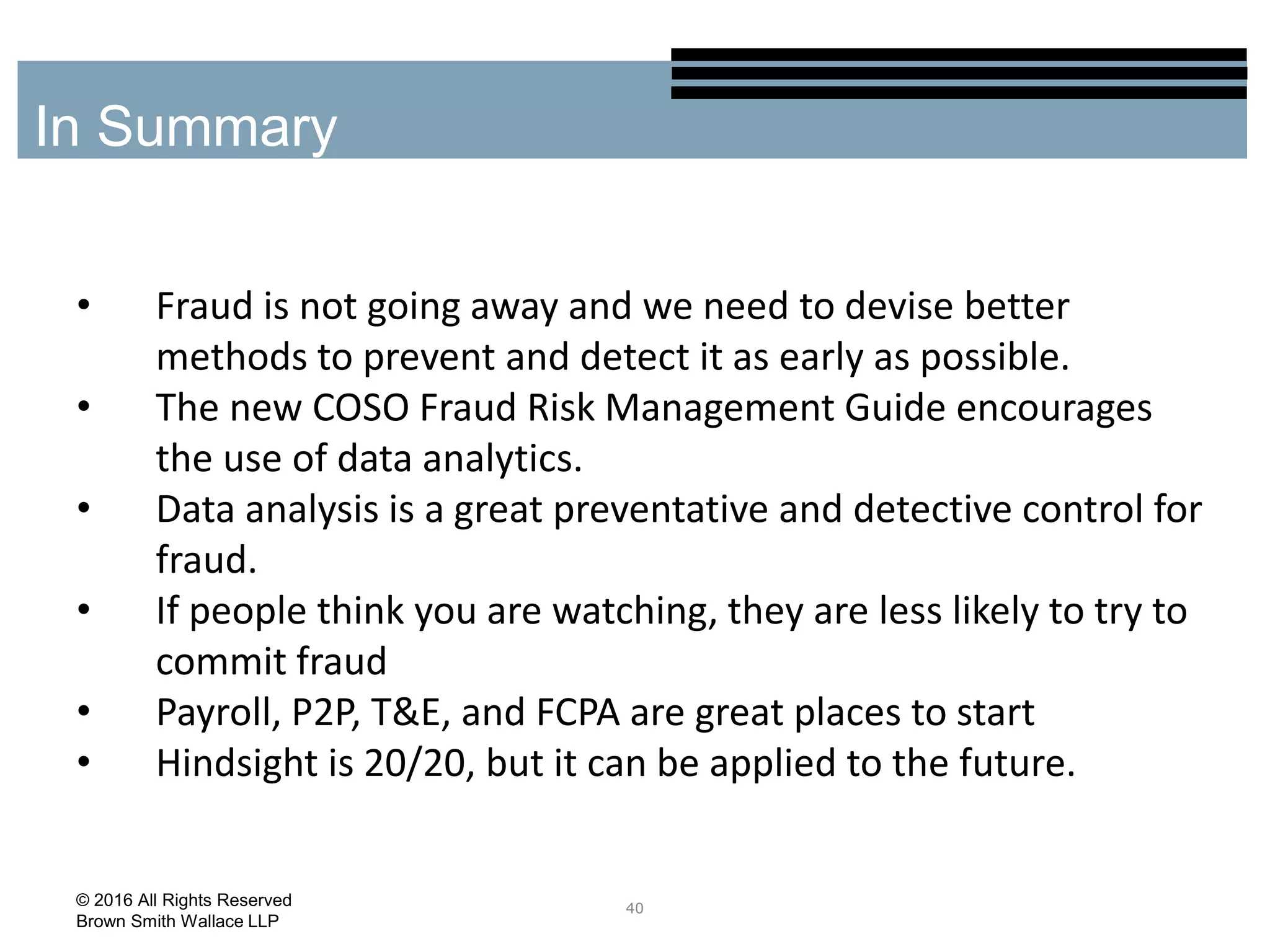

The document discusses using data analytics to identify fraud indicators. It provides an overview of COSO's fraud risk management principles and how data analysis fits within those principles. Several fraud risk areas are identified that are well-suited for data analytic techniques, including payroll, accounts payable, travel and entertainment, procurement cards, and foreign corrupt practices. Examples of specific fraud indicators that could be identified through data analysis for each risk area are also provided.