Download as PDF, PPTX

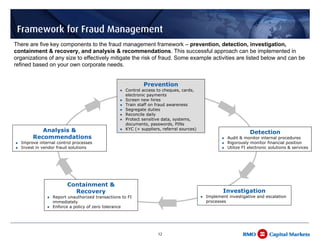

The presentation covered payment fraud trends and strategies for combating fraud. It discussed how fraud is increasing with the economic downturn and criminals are targeting various payment methods like checks, cards, and electronic payments. The speaker outlined a fraud management framework of prevention, detection, investigation, containment/recovery, and analysis. Statistics showed most organizations experienced fraud attempts in 2008. Common fraud types involved checks, cards, and electronic methods. The presentation provided strategies for organizations to strengthen internal controls and leverage tools from financial institutions to reduce fraud risks and losses across different payment types.