Download to read offline

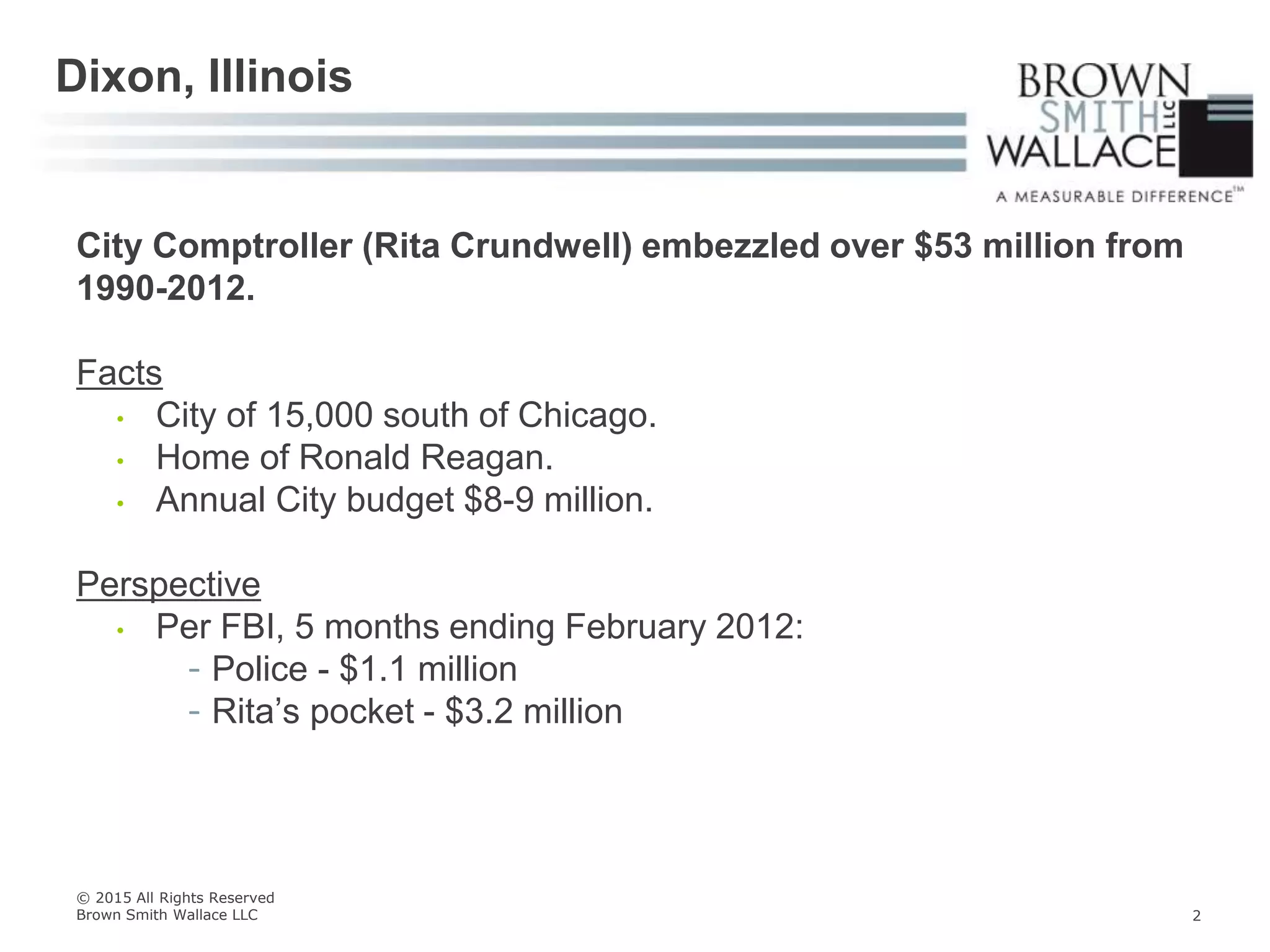

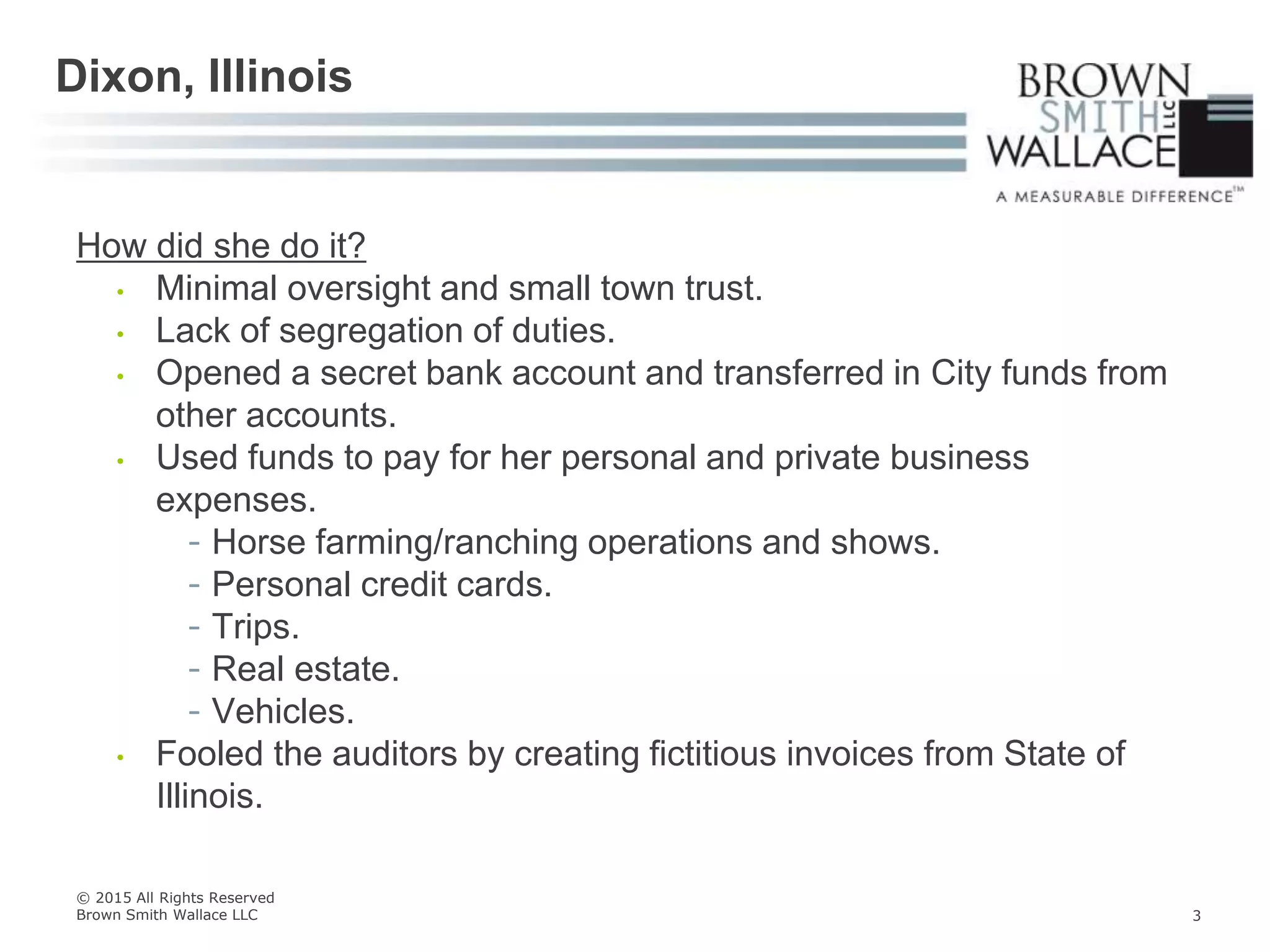

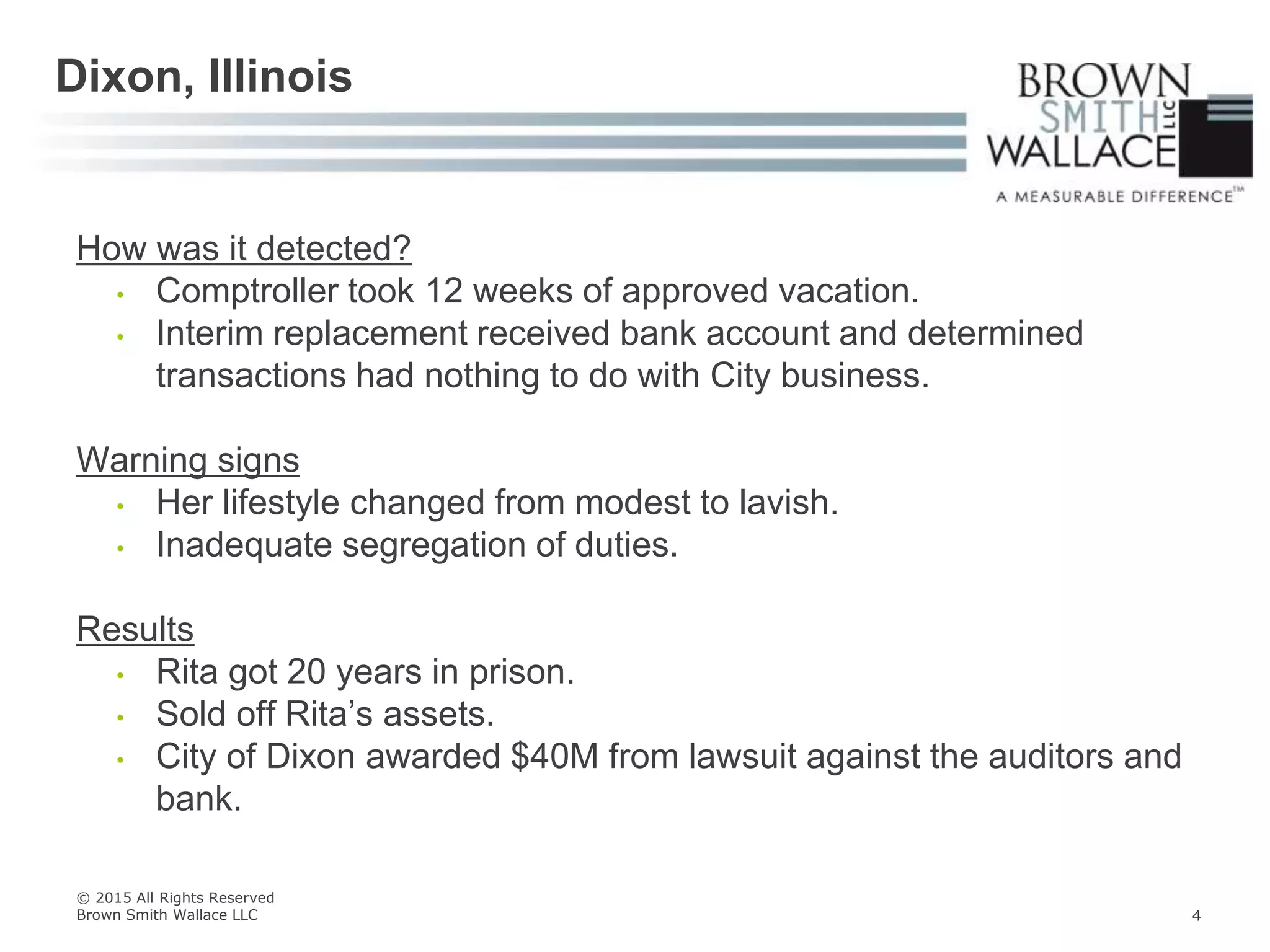

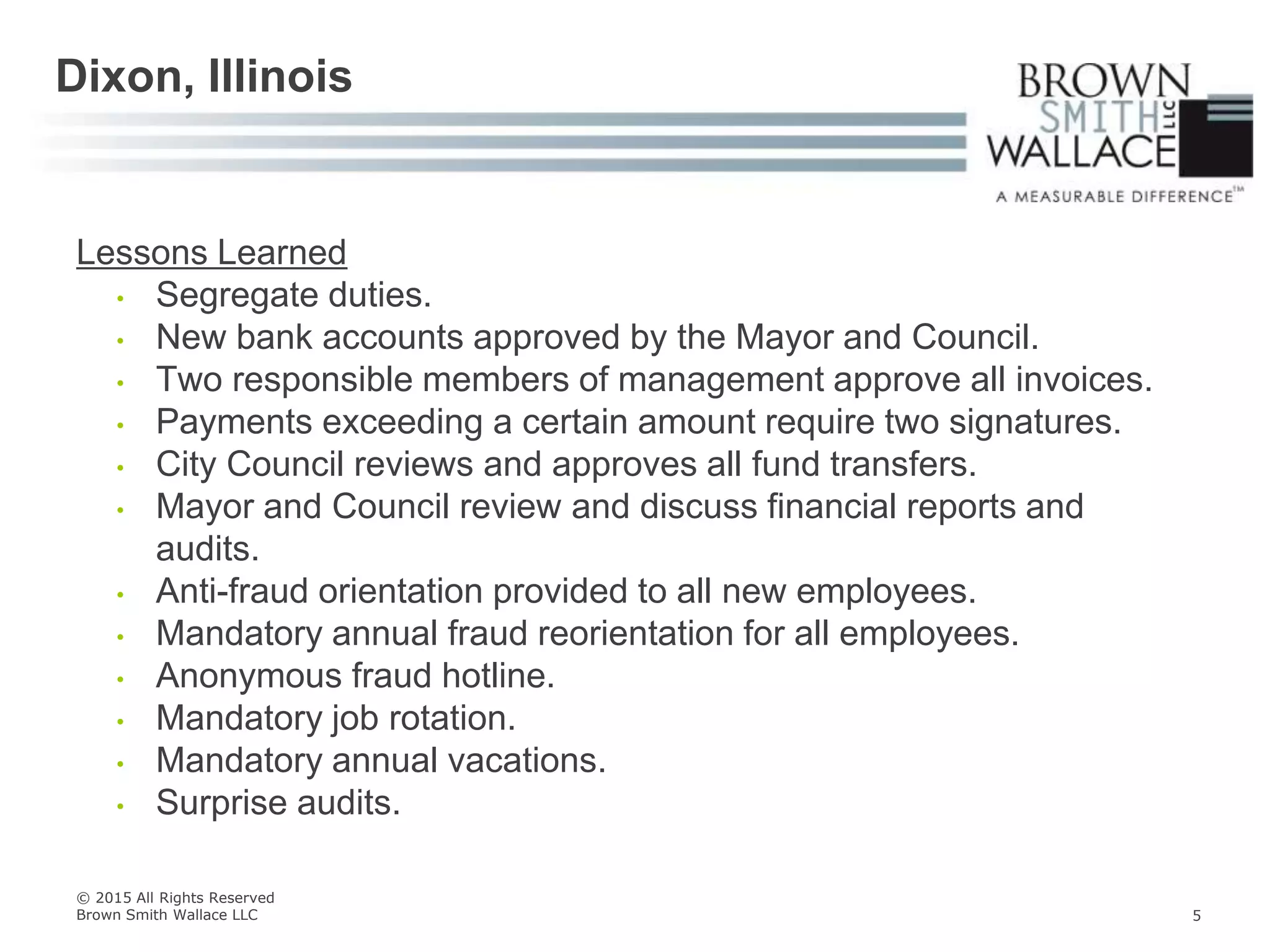

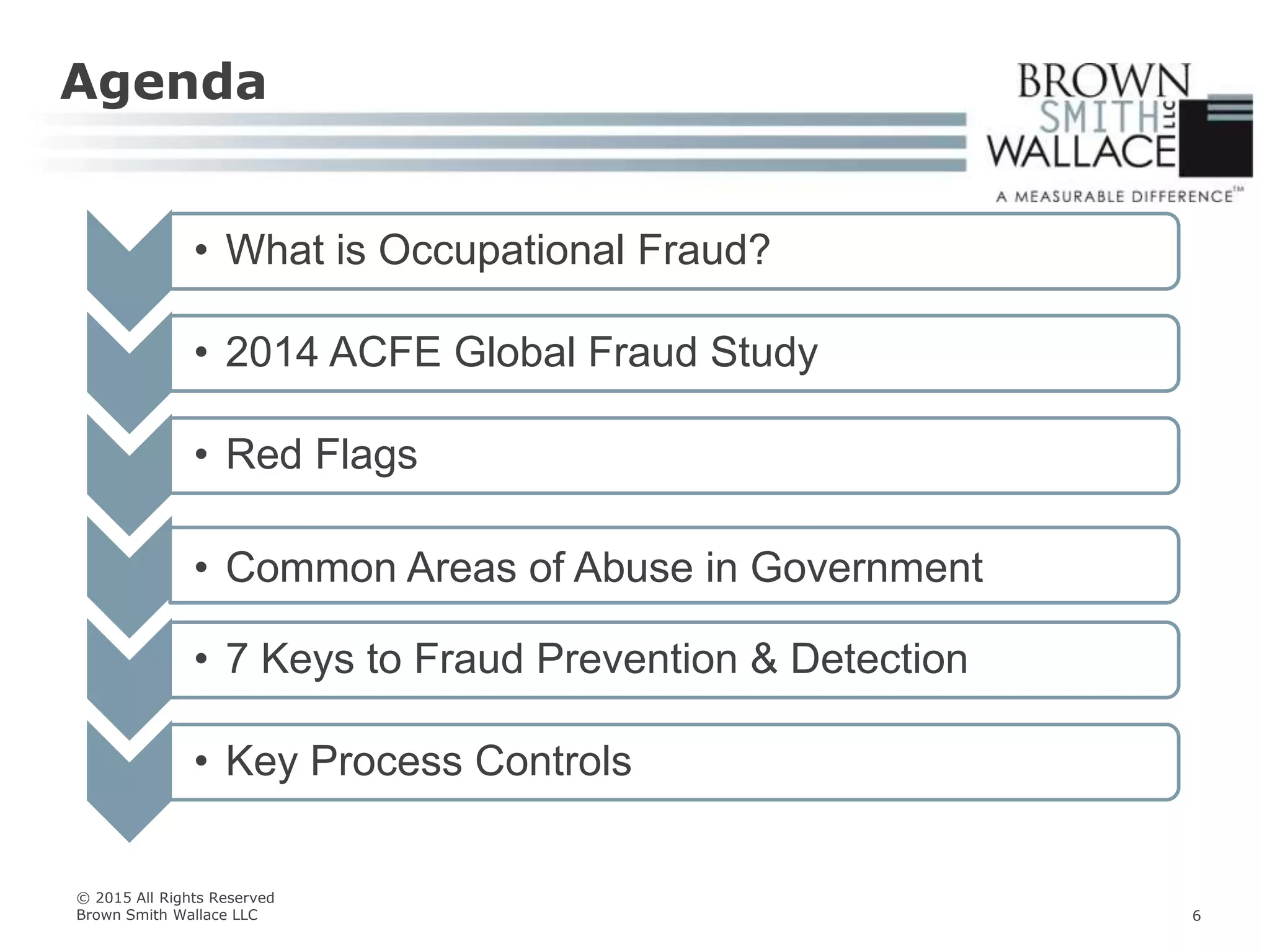

The document discusses steps to prevent and detect occupational fraud in government. It begins by providing an example of the largest municipal fraud in US history, where the comptroller of Dixon, Illinois embezzled over $53 million from 1990-2012. It then outlines common areas of fraud like skimming, check tampering, billing schemes, and payroll fraud. Finally, it discusses lessons learned like segregating duties, increasing oversight of funds, and establishing controls like mandatory vacations and job rotation.