Downloaded 40 times

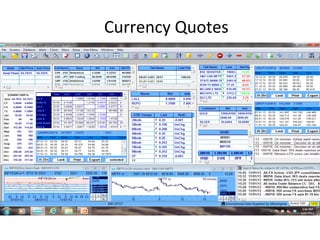

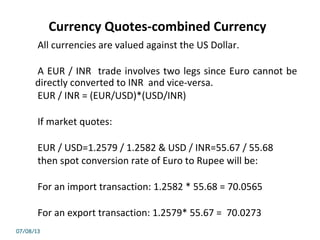

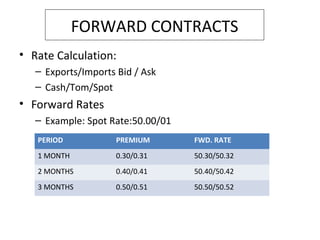

The document discusses various concepts related to foreign exchange including: 1) Exchange rates reflect how much one currency values against another and are expressed using currency codes like USD/INR. 2) Direct quotes express exchange rates for a foreign currency in units of the home currency, while indirect quotes use the local currency. 3) Currency trades between currencies that cannot be directly converted, like EUR/INR, involve two exchange rates through the USD. 4) Forward rates are used to hedge currency risk for trades settling beyond the spot date and can involve premiums or discounts depending on interest rate differentials.