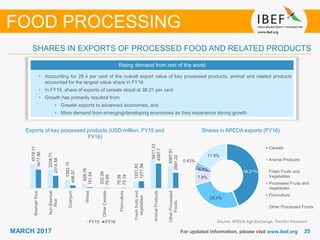

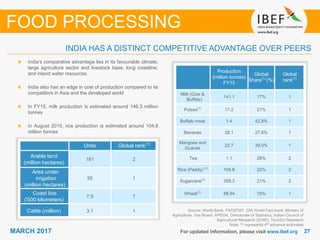

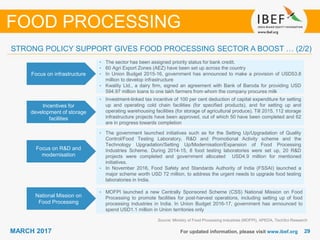

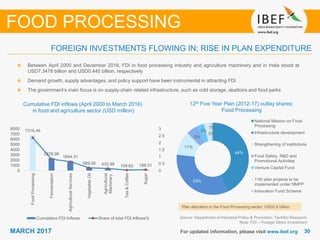

Download as PDF, PPTX

The document provides information on India's food processing sector. Some key points: - India has a large agriculture sector and is the largest producer of milk and second largest producer of fruits and vegetables globally. - The food processing industry is one of India's largest industries, accounting for around 14% of manufacturing GDP and expected to reach $482 billion by 2020. - Major segments include fruits and vegetables, milk, meat and poultry, marine products, and grain processing. The organized sector accounts for around 70% of the industry. - Notable trends include rising domestic and international demand, entry of international companies, changing consumer preferences towards healthier options, and increasing exports.