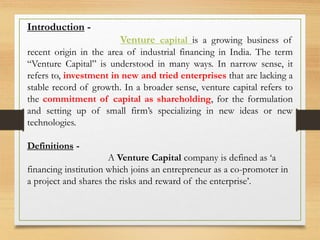

This document provides an overview of a presentation on venture capital. It includes definitions of venture capital, the nature and scope of venture capital, regulatory framework, problems with venture capital, the venture capital investment process, the current scenario in India, global experience, and conclusions. The document outlines topics that will be covered in the presentation and provides background information on venture capital concepts.