Downloaded 1,440 times

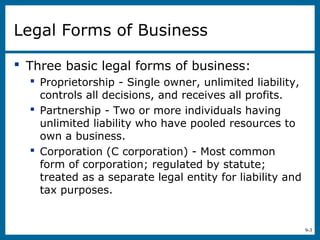

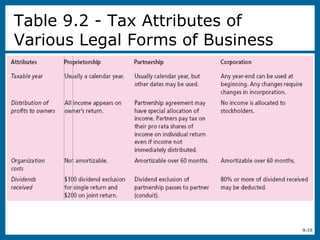

This document discusses different aspects of developing an organizational plan for a new business venture, including: 1) Developing the management team to operate the business full-time with modest salaries to demonstrate commitment. 2) The three main legal forms of business - proprietorship, partnership, and corporation - and their characteristics. 3) Factors to consider when choosing a legal structure, such as limited liability, taxes, and regulations. 4) The roles and responsibilities of a board of directors and board of advisors in advising and governing the organization.