Downloaded 14 times

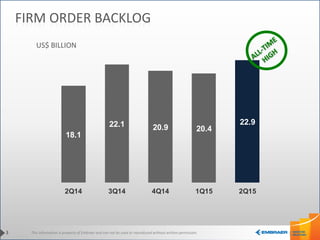

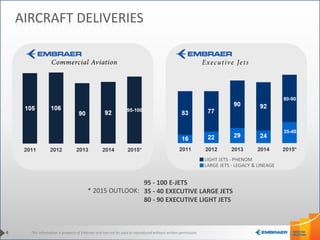

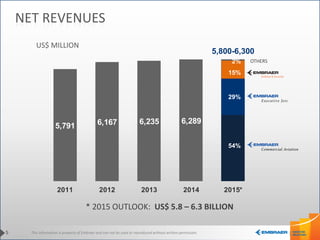

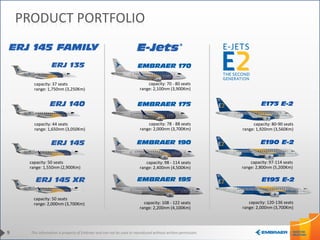

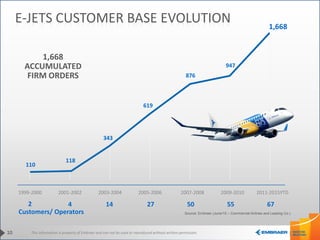

This document provides an overview of Embraer's corporate and business strategy, including: - Organic growth, margin enhancement, business diversification, and organic growth through acquisitions. - Establishing Embraer as the defense house of Brazil and focusing on product strategy, customer base expansion and excellence in customer experience. - Details on Embraer's commercial jet portfolio, order backlog, revenues, and outlook for 2015 aircraft deliveries. - Information on the E-Jets family and new E2 models in development.