DME Methanol Outlook for gas conversion Amoco 2000

•

1 like•635 views

The document discusses Amoco's strategy to capitalize on the emerging gas-to-liquids (GTL) industry through focusing on oxygenate products like methanol and dimethylether (DME). It describes GTL as a strategic inflection point that will transform the energy industry similarly to the past shift from coal to oil. Amoco aims to establish a commercial position in methanol and DME production through various projects and partnerships. This will allow them to control fundamental building blocks in chemical and fuel markets and monetize stranded natural gas resources. The key is to act quickly as a first mover to build capability and options before competitors, in order to influence the strategic changes coming to the energy industry through GTL.

Recommended

Recommended

More Related Content

What's hot

What's hot (20)

Viewers also liked

Viewers also liked (10)

Similar to DME Methanol Outlook for gas conversion Amoco 2000

Similar to DME Methanol Outlook for gas conversion Amoco 2000 (20)

More from Steve Wittrig

More from Steve Wittrig (20)

Recently uploaded

Recently uploaded (20)

DME Methanol Outlook for gas conversion Amoco 2000

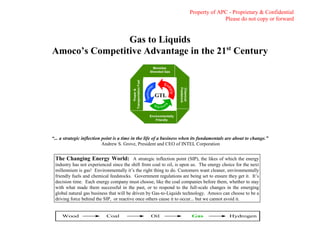

- 1. Property of APC - Proprietary & Confidential Please do not copy or forward Gas to Liquids Amoco’s Competitive Advantage in the 21st Century M Monetize Stranded Gas Environmentally Friendly Power& TransportationFuel Chemical Feedstock GTL “... a strategic inflection point is a time in the life of a business when its fundamentals are about to change.” Andrew S. Grove, President and CEO of INTEL Corporation The Changing Energy World: A strategic inflection point (SIP), the likes of which the energy industry has not experienced since the shift from coal to oil, is upon us. The energy choice for the next millennium is gas! Environmentally it’s the right thing to do. Customers want cleaner, environmentally friendly fuels and chemical feedstocks. Government regulations are being set to ensure they get it. It’s decision time. Each energy company must choose, like the coal companies before them, whether to stay with what made them successful in the past, or to respond to the full-scale changes in the emerging global natural gas business that will be driven by Gas-to-Liquids technology. Amoco can choose to be a driving force behind the SIP, or reactive once others cause it to occur... but we cannot avoid it. Wood Coal Oil Gas Hydrogen

- 2. Property of APC - Proprietary & Confidential Please do not copy or forward 2 Gas-to-Liquids: The Industry’s Next Mega-Trend Natural gas is increasing in popularity as an alternative fuel where market links exist via pipeline or LNG. Gas-to-liquids (GTL) represents the next phase in transforming gas into a truly global commodity. The commerciality of GTL has become the hottest topic in the energy industry. It is now economically feasible to manufacture clean liquid fuels, fuel additives, and chemical feedstocks from natural gas, capable of displacing petroleum based products in traditional markets. No single technology has affected as many segments of the energy industry as GTL will in the future. The implications to the E&P sector alone are huge. Worldwide natural gas resources are estimated to exceed 14,000 TCF proved and possible. Over 50% of the current proved resources, 900 TCF, are considered stranded due to inaccessibility to market. Successfully linking these resources to markets is like discovering several hundred billion barrels of new clean oil. The implications for the chemical and refining and marketing sectors could be even greater. Oil refining produces products from crude oil by breaking (cracking) very large hydrocarbon molecules, whereas GTL starts with the basic methane molecule and custom builds the desired product. This fundamental shift in technology will lead to totally new ways of doing business. New studies, partnerships, and projects are announced monthly. Construction of the first commercial world-scale GTL plant will set off a major scramble for position. Being first counts! Once established, GTL will become a serious game of haves and have nots. Those with access to competitive GTL technology and natural gas resources are in and will be preferred partners to those trying to catch up. Companies possessing GTL capabilities will be competitively advantaged to: 1. Capture and monetize new E&P opportunities (gas and oil) previously deemed off limits via non-conventional approaches. 2. Market value-added products in existing and new transportation fuel markets, e.g., clean diesel, diesel and gasoline additives and fuel cells. 3. Control fundamental building blocks in the chemical value chain, e.g., methanol and DME. 4. Introduce options to address environmental, regulatory and production problems facing customers and governments. M Monetize Stranded Gas Environmentally Friendly Power& TransportationFuel Chemical Feedstock GTL 0 50 100 150 200 250 300 350 400 1980 1982 1984 1986 1988 1990 1992 1994 1996 Liquids Gas MBOE/D Amoco’s International Oil and Gas Production “Stranded” Natural Gas Reserves Amoco Reserves BP Reserves Competitor’s Reserves

- 3. Property of APC - Proprietary & Confidential Please do not copy or forward 3 The GTL Game: Technologies, Approaches and Challenges Major oil and technology companies have invested hundreds of millions of dollars since 1980 on the development of GTL technologies. Ongoing industry investments have led to several process improvements that substantially reduced the cost of these technologies over the last several years. Recent breakthroughs have resulted in smashing through the historical cost barrier of $30,000/bbl of daily capacity. The long term goal is to push GTL capital costs down to $12,000/bbl of daily capacity, which is on par with a world-scale crude oil refinery. As cost continues to decline below $30,000/bbl of daily capacity, new markets in transportation and power fuels, and expanded chemical feedstock applications will develop and grow, and gas will compete as a true global commodity. Today, there are two fundamentally different GTL approaches, Fischer-Tropsch (F-T) and oxygenates. Common to both is the production of syngas, the process by which natural gas is chemically converted to a reactive intermediate which is in turn converted to the final liquid product. The syngas step accounts for over 60% of the total capital cost of manufacturing GTL. Amoco established a technical consortium (Oxygen Transport Membrane - OTM) with BP, Phillips, Statoil, Praxair and Sasol that is focused on reducing the cost of syngas production by 20-30%. F-T is often used interchangeably with GTL, and is by far the most popular GTL process in terms of dollars invested. The F-T process generates long, straight-chain hydrocarbons of varying lengths. This syncrude is sold into global oil markets at a price premium (+30-45% over crude oil) due to it’s added value as a diesel blending agent and specialty wax. Shell, Exxon, and Sasol are the industry leaders in this technology. All three have proprietary technologies, however Shell and Exxon regard them as competitive advantage and are unwilling to offer their GTL technologies for license. The majority of the other big players (Chevron, Texaco, Arco) have pursued this technology via partnerships with either Sasol or Syntroleum (a relatively new technology provider). Amoco is positioned to pursue F-T, if it chooses to do so, via a cooperative agreement with Sasol. Amoco made the strategic decision to pursue GTL by focusing on oxygenate products (e.g., methanol, DME, DMM). This decision was based on a combination of commercial and technical advantages for oxygenate manufacturing including: 1. Lower capital cost and smaller gas resource requirements 2. Higher conversion efficiency at lower energy consumption 3. The potential breadth of new and existing market applications 4. Opportunity to control technology via patents and exclusivity contracts versus trying to play catch up with Shell and Exxon’s F-T research M Monetize Stranded Gas Environmentally Friendly Power& TransportationFuel Chemical Feedstock GTL PLANTCAPITALCOST, $M/DAILYBBLCRUDEOILEQUIV. Mobil, MTG, NZ, 1985 Shell, FT, Malaysia, 1993 0 20 40 60 80 100 1985 1990 1995 2000 2005 II Exxon, FT, Qatar, 1996 Phillips-Sasol, FT Qatar, 1997 Amoco, DME, 1997 III “Economic” GTL ($30000) Crude Refinery Target ($12000) + Catalyst + Natural Gas Oxygen Syn Gas Carbon MonoxideHydrogen Catalyst Methane Syn Crude Dimethoxymethane (DMM)Methanol Dimethylether (DME) Oxygenates Fischer-Tropsch

- 4. Property of APC - Proprietary & Confidential Please do not copy or forward 4 Methanol is currently the largest (by volume) oxygenate produced and is used primarily in manufacturing MTBE, formaldehyde and acetic acid. In addition, there is a wide range of untapped oxygenate markets which include chemical feedstocks, transportation fuels, and power generation. While certainly smaller than the global oil market available to F-T, these oxygenate markets offer tremendous growth potential and higher margins. For example, “low cost” methanol currently sells for $100/ton ($5.25/mmbtu) compared to $21/bbl syncrude ($3.60/mmbtu) in a $15/bbl ($2.60/mmbtu) crude oil market. Amoco’s Vision 2010 (Addendum 1), is to focus in the near term to establish a commercial position in methanol and DME. The primary hurdle to developing an oxygenate-based GTL business will be to establish new market applications and grow existing markets. Amoco is well positioned in many of these markets and value chains to cause future SIPs with the introduction of next generation oxygenates and/or new market applications. For example, using methanol or DME as the basic building blocks in the manufacture of olefins and/or aromatics. In transportation fuels, DMM (or derivatives) could be the key to clean diesel, a diesel additive, an improved substitute for MTBE in gasoline, and along with methanol, the fuel of choice for fuel cells. Unlike Shell and Exxon, our strategy to access GTL technology was a balance of in-house proprietary work and partnering with key technology developers. Taken as a whole, Amoco’s competitive advantage is now greater than the sum of the specific partnerships and agreements listed below, and provides us the option to respond quickly to customer needs. Exclusivity in the near term with key DME technology provider - Haldor Topsoe Partnership with methanol marketer and engineering company - Saturn and Lurgi Proprietary DMM technology Cooperative relationship with key turbine manufacturers - GE and Westinghouse GM clean diesel partnership Two economic projects, Titan and Atlas - establishes a Caribbean platform for low cost methanol Cooperative agreement in India - GAIL, IOCL, IIP Joint DME study in Japan and Far East - EPDC F-T technology sharing agreement - Sasol OTM consortium Partnership with AVL, the worlds largest engine testing lab, in the development of DME as diesel alternative The result is that Amoco is poised to jump ahead of the competition in the GTL game. However, there is a limited window of opportunity in which to act. While the balanced approach has allowed us to leverage our research dollars to gain tremendous capability in a short time frame, continued exclusivity with these key technology partners requires performance - use it or lose it. Methanol DME Formaldehyde MTBE DMC Olefins DMM Acetic Acid Aromatics Gasoline Power Fuel Natural Gas Refinery Polypropylene Diesel Additive Polycarbonate PTA Gasoline Additive Cellulose Acetate Vinylacetate Fuel Cells Natural Gas Oxygen Polyethylene

- 5. Property of APC - Proprietary & Confidential Please do not copy or forward 5 Building Capability ===> Future Optionality Uncertainty gives the GTL business tremendous upside potential. To continue to make intelligent choices, we must develop flexibility to respond to new information. Our strategy builds optionality in a stepwise manner through individual project investments (Addendum 2) designed to secure potential upsides while insuring against the downside and providing multiple exit points. Ultimately, the value of the options we generate is recognized through the value of learning (Addendum 3). The Titan methanol plant provided key learnings and partnerships which contributed greatly to the development of the Atlas mega-methanol plant. In turn, Atlas will provide valuable learnings that enable the commercialization of DME for the Qatar/India project with less risk. Another key aspect to optionality is geographic presence - a foothold in the region. By 2004, we will have established growth platforms in the Caribbean and Middle East, with a third platform currently envisioned in the Far East. In addition, there exists a multitude of stranded gas supply and market development options that could provide the next steps for continued growth of the GTL business. To win in the long-term requires Amoco to utilize the potential of GTL technology to capture large low cost natural gas resources, NOW. With low cost manufacturing and secured low cost resources, we will be competitively advantaged to offer unique energy solutions to customers with environmentally superior, high value-added chemical feedstocks, fuels and fuel additives. This is not based solely on internal perception. Potential customers have demonstrated a strong interest (Addendum 4) and have confirmed, “There are vast market opportunities for clean cost competitive fuels.” 1999 2001 2003-4 Titan Atlas Qatar/India DME Market: 1. Introduction to MeOH business 2. Establish partner network Market: 1. Initiate new MTO market 2. Initial exposure to DME value chain 3. Positioned as low cost producer of MeOH Technology: 1. Prove scale-up mega-methanol technology 2. DME logistics Market: 1. DME end users 2. EstablishDME marketing partners 3. Establish low cost DME position Technology: 1. Full scale DME logistics 2. Optimize “on-purpose” DME facility Supply: 1. Capture supply via tech & markets Strategic: 1. DME value-chain doability 2. Establishes AN as a leader in GTL business MeOH / DME to Olefins Chemical Feedstocks Transportation Fuels Fuel Cells DME for LPG M Monetize Stranded Gas Environmentally Friendly Power& TransportationFuel Chemical Feedstock GTL Methanol Supply Hub DME/Methanol Supply Hub Potential Future Flows of GTL Products

- 6. Property of APC - Proprietary & Confidential Please do not copy or forward 6 Keys to Success The bottom line... Amoco has a distinct competitive advantage to be a first mover - to move quickly and decisively to build capability, secure low cost gas resources, create options and establish growth platforms before the competition has time to respond. The key to success is to understand and respond quickly to external and internal forces. Our external business challenges are to: 1. Be a first mover to establish credibility, capability and capture higher returns. 2. Utilize our knowledge of the potential of GTL to secure long-term low cost gas supplies before market forces drive up the competition and gas owner expectations. 3. Manage partnerships with technology providers (i.e., Lurgi and Haldor Topsoe) to optimize speed and flexibility of execution that results in wins for all parties. 4. Continue improving cost of technology - internally and with partners. 5. Develop next generation oxygenate and/or introduce new market applications to cause future SIPs. Leverage GM partnership for clean fuels and increased engine efficiency Partner with UOP to access MTO technology 6. Expand participation in the value chain to capture shifting margins. Our internal challenges are to: 1. Establish a common mindset that the GTL business is ours to win. 2. Establish single point accountability. 3. Endorse a first mover mentality. 4. Manage as a cross-stream business. 5. Establish processes to enable effective communication and learning. Amoco is at a very early stage in the overall development of GTL as a core business. A centralized, coordinated effort is needed to ensure that individual projects realize the learning, capability and optionality objectives which go beyond the specific project scope and economics. Historically, the industry has not been very successful in realizing the full potential of cross-stream businesses. Amoco is no exception. As we move forward, this is our biggest challenge. With an effective organization and management structure, and well defined accountability, we can establish a new core business with PV10 (1/1/98) > $.5 billion by 2010 (Addendum 5). It’s time to choose to be a have or a have not! We are positioned to influence the inevitable Strategic Inflection Point. As first movers, we can have the competition chasing us. M Monetize Stranded Gas Environmentally Friendly Power& TransportationFuel Chemical Feedstock GTL

- 7. Property of APC - Proprietary & Confidential Please do not copy or forward 7 Addendum 1: Vision 2010 Our Purpose: Create and build a new core business for the Corporation in gas-to-liquids. Initially, we will focus on the commercialization of distinctive technologies and the development of new markets, to manufacture and sell DME and methanol. Our approach to GTL will change the rules governing the methanol business and develop the rules for the DME and oxygenate businesses. Mission - “What our business is” The identification and capture of markets for products manufactured from the chemical conversion of natural gas to fuels and chemicals to optimize short term profitability and promote long term growth. Vision 2010 - “ What we want to be” The preferred partner for providing oxygenate fuels and low cost chemical feedstocks from natural gas. Philosophy - “Underlying concepts, attitudes and general beliefs” Build the GTL business by taking focused and deliberate project steps to steadily increase capability and establish an advantaged position for future opportunities. Each project should stand on its own economically Analyze individual project scope decisions within the frame of the greater business to enhance the range and quality of future investment options for growing the business first to identify and capture new markets first to realize the potential and capture new technology Align with partners to grow the business - technology, supply and markets gain capability and competitive advantage (i.e., exclusivity) mitigate risk Realize current technical competitive advantage to create and grow optionality to sustain competitive advantage in the future M Monetize Stranded Gas Environmentally Friendly Power& TransportationFuel Chemical Feedstock GTL

- 8. Property of APC - Proprietary & Confidential Please do not copy or forward 8 Addendum 1: Vision 2010 Continued Goals - “2010” Financial (Capture 4 platform projects): NPV10 (1/1/98) > $300 mm Net Income > $100 mm ROACE > 15% Environment, Health and Safety: Maintain a healthy and accident free business based on a fully implemented EHS Management System. Demonstrate improved environmental quality of produced products. Stationary sources utilizing our fuel products will achieve a 95% SOx reduction and a 20% reduction in greenhouse gases (CO2 equivalents, lb/MW-hr) as compared to distillates. Oxygenates used as diesel additives (10% blend) will achieve 30% reduction in particulate emissions (soot) over #2 diesel. Technology: Reduce the GTL capital cost of daily plant capacity by 25% from 1998 levels. Markets: 50% of all sales (by volume) will be to new markets created after 1998. Supply: Monetize 700 MMCFD gross, 300 MMCFD net of natural gas. Capture 15 TCF gross of low cost natural gas resources Organizational Effectiveness / Capability: Ensure necessary systems and capabilities are in place to qualify as a world class organization by 2010 (i.e., attain a score of +700 based on Amoco’s ABA) Strategies - “How we will accomplish our goals” Marketing: MARKETS IN A CHANGING WORLD We will capture growth in existing methanol markets as low cost provider and create new markets that are awaiting a lower cost oxygenate material. Supply: GETTING THE BEST SEAT IN THE HOUSE We will identify, prioritize and capture targeted gas resources in regions that allow us to best service near-term markets and sustain long-term growth. External Focus: LIVING IN THE REAL WORLD We will utilize knowledge from across Amoco and the external world to identify the most promising market opportunities, to lead their development, and to capture value from that growth. Best Cost: UP THE LEARNING CURVE We will establish and maintain a low cost position via economy of scale, continuous technology improvements with our partners, and rapid implementation of learnings across our business. Environmental: GREEN POWER We will define the applications of our products that can reduce emissions, publicly advocate these advantages to our customers, and achieve other quality of life goals of the communities in which we operate. Organizational Capability: HONING OUR SKILLS We will sustain competitive advantage by developing capabilities within Amoco and with our partners. We will continually identify our most critical capability gaps and implement plans to fill them. M Monetize Stranded Gas Environmentally Friendly Power& TransportationFuel Chemical Feedstock GTL

- 9. Property of APC - Proprietary & Confidential Please do not copy or forward 9 Addendum 2: The Projects - Titan, Atlas, and Qatar/India Amoco entered the GTL business with the Trinidad Titan methanol plant, currently under construction. The primary business driver was the monetization of equity gas resources - supply push - with an eye toward understanding the methanol business through partnership with Saturn. This JV created a powerful alliance by combining Amoco’s natural resources with Saturn’s methanol marketing and technological expertise. Amoco has a 15% working interest and will supply 100% of the gas (80 mmcfd gas sales) to the 2500 TPD Lurgi designed plant. When operational, Titan will represent one of the lowest capital cost per ton of capacity plants, in the world. Approximately 80% of production capacity is already sold under take-or-pay contracts to markets in the United States and western Europe. The capabilities developed with Titan facilitated the next project step to the 5000 TPD mega-methanol Atlas plant. Amoco will again supply 100% of the gas (160mmcfd) and have a 35% working interest in the plant. The Lurgi designed mega plant represents a manufacturing cost breakthrough (20% overall reduction) and positions Atlas as the low cost provider in the methanol business. Lurgi has offered Saturn an exclusive license in Trinidad for its technology, providing the Saturn-Amoco JV a first mover advantage. Saturn is currently negotiating with Exxon to supply them 500M tons per year of methanol to feed their Baytown, Texas, methanol-to-olefins (MTO) facility scheduled for start-up in 2002. The results of this pilot could open a new methanol market and provide further option value as described in Addendum 3. In addition, the Lurgi technology allows for DME production through a dehydration step at the end of the process at minimum incremental capital cost and maximum flexibility (0 - 100% DME). The capability to produce DME is critical to initializing several emerging markets in the Caribbean and United States, e.g., chemical, olefin, power and transportation, where producers and markets have been at loggerhead with each unwilling to be the first to make the commitment to enable the other to proceed. DME production at Atlas will also develop capabilities, i.e., logistics and marketing, that will significantly mitigate some of the risks associated with the Qatar/India and Japan/Far East (EPDC) DME projects, both currently under evaluation. The potential India markets are huge. With a population approaching one billion, the projected deficit in power generation is 12,000 MW by 2001-02. The application of LNG is limited and the alternative fuel is naphtha. Diesel consumption exceeds gasoline 7:1 in the transportation market and is growing at 9%/year. Pollution is a major concern and cleaner fuels are needed. The Qatar /India project scope assumes a 17.5% WI plant located in Qatar. This will be Amoco’s first on-purpose DME plant employing Haldor-Topsoe technology to manufacture 7000 TPD (MeOH equivalent) DME. Amoco’s partners would be the Qatar General Petroleum Company (QGPC), Gas Authority of India (GAIL), Indian Oil Corporation Limited (IOCL), and Indian Institute of Petroleum (IIP). M Monetize Stranded Gas Environmentally Friendly Power& TransportationFuel Chemical Feedstock GTL Qatar/India DME 1999 2001 2003-4 Titan Atlas Equity Gas WI=100% Lurgi Technology WI=15% 2500 MTPD Methanol Saturn Markets Methanol T-O-P Price Floor Equity Gas WI=100% Lurgi Technology WI=35% 5000 MTPD MeOH Dme Option Process & EPC Cost guarantee Saturn Markets Methanol T-O-P Price Floor Niche DME market Captured Supply WI=17.5% Partners: QGPC, India combine H-T Technology WI=17.5% 7000 MTPD (MeOH eqv) 5300 MTPD DME Indian DME Markets Power

- 10. Property of APC - Proprietary & Confidential Please do not copy or forward 10 Addendum 3: Optionality What is optionality? Optionality is additional value derived from an investment over and above the financial returns directly attributable to that investment. The option value generally impacts future opportunities in the form of reduced risk, preserving existing or creating new opportunities, reduced chase cost, and increased probability of capture. The value of optionality is real and measurable in post appraisal. However, it is very difficult to quantify point forward because it’s based on the holders perception of the future. By example, on Wall Street, an option to buy a share of stock at a predetermined price and future date, is sold at a premium above the strike price. The cost of the option is determined by the market. The buyers final value won’t be determined until he exercises the option or time runs out and it expires. Optionality has real value in the GTL business as well. Our strategy builds optionality in a stepwise manner through individual project investments. Because much of the strategy is based on future projects it is difficult to represent the value optionality creates. However, to illustrate the potential, consider the optionality created by the Trinidad Atlas project. As a stand-alone project, Atlas has a PV(10)=$80mm. Once the Atlas plant is built, three options are created for the disposition of methanol: 1) sell methanol as methanol, 2) sell methanol as a transportation fuel additive via DMM, or 3) sell methanol as olefins (MTO). The latter two options result in an expanded gas value chain. Under current project assumptions, Atlas will buy inlet gas for $.90/mmbtu and sell methanol for $90/MT (w/ escalation) or $4.75/mmbtu. If ongoing work proves commercial, it will be possible to convert methanol to DMM and Poly-DMM for blending with gasoline and/or diesel, thereby raising the value of the BTUs sold from $4.75/mmbtu (as methanol) to $8.90-11.00/mmbtu as fuel additives. Granted, the value associated with this expanded value chain is highly uncertain. However, the potential to triple the revenue received for each BTU sold suggests that this option has significant value. Another alternative that may develop is to install an MTO plant in Trinidad to supply olefins to a future polyethylene plant. The Government and Energy Ministry of Trinidad and Tobago are promoting private investment in an ethane cracker and polyethylene plant to maximize value from their gas. If ongoing work on MTO technology proves commercial and the Trinidad Government’s plans proceed, this option becomes real. Again, the additional revenue realized for each BTU (or lb) sold is substantial. Admittedly, there is significant uncertainty associated with each of the alternatives described above. The point to remember is that the Atlas project and other related GTL activities (DMM & MTO research) have a value, greater than that directly related to the specific project, by positioning us to capture future growth opportunities once the economics are better understood. M Monetize Stranded Gas Environmentally Friendly Power& TransportationFuel Chemical Feedstock GTL Atlas MeOHNatural Gas DMM plant Texas City Refinery Blended Gasoline (MTBE substitute = $.80 / gal) Blended Diesel (DMM additives = $.65 / gal) 2000 TPD 10M BPD IRR=13% $90 / Ton $4.75 / mmbtu $.50 / gal $6.85 / mmbtu $.65 - .80 / gal $ 8.90-11.00 / mmbtu$.90 / mmbtu methanol market FOB price $90 / ton 5000 TPD 2000 TPD MTO plant IRR=13% 150 MMCFD Trinidad Polyethylene Plant $90 / Ton $0.045 / lb $0.18-23 / lb $0.35-50 / lb

- 11. Property of APC - Proprietary & Confidential Please do not copy or forward 11 Addendum 4: Customer Response Customer response to DME and DMM has been extremely positive. Their message is... “There are vast market opportunities for clean cost competitive fuels.” General Electric: In 1996, GE did a test burn in their “E” class turbine using DME provided by Amoco. A comment by the lead technician sums it up best, “... it took us years to fine tune this machine to burn natural gas. With DME, you guy hit it on the first try.” Based on this test, GE engineers refined their burner design to virtually eliminate flashback. A second test with an “F” class machine is scheduled to be completed by year end as part of the Amoco - EPDC (Japan Power Company) joint study agreement. EPDC has agreed to finance the test. EPDC: EPDC is one of the largest power producers in Japan. Amoco and EPDC have a joint study agreement to assess the economic feasibility of DME as a power fuel in Japan and the Far East and a commitment to partner in future power projects. EPDC recognizes the environmental benefits of DME over conventional fuels and the space benefits (requires smaller footprint) over LNG, and are considering DME as the power fuel for an expansion project in 2004-6. India: The Gas Authority of India (GAIL), Indian Oil Corporation Limited (IOCL), and Indian Institute of Petroleum (IIP) have all expressed keen interest in DME as a potential solution to their growing power and transportation fuel needs. They have signed an MOU with Amoco to complete a Technical Economic Feasibility Report by early 1999. Their primary message to Amoco has been, “... can we do it any faster?” DME could prove to be an alternative fuel for naphtha in power as well as address the severe environmental situation caused by diesel in transportation vehicles in major cities. AVL Powertrain: AVL is very enthusiastic about DME as a diesel substitute. So much so that it has designed and tested a conversion package to convert diesel vehicles to DME. They have worked the cost down to roughly $800/conversion and even less on new builds. Partnership for New Generation Vehicles: In recent testing by the PNGV group (GM, Ford, Chrysler, Mobil, Arco, Amoco, Exxon, and DOE) DMM was the clear winner of seven fuels tested. Blended 15% with diesel, DMM reduced particulate emissions 45%, significantly better than F-T liquids, low-sulfur diesel, and biodiesel. M Monetize Stranded Gas Environmentally Friendly Power& TransportationFuel Chemical Feedstock GTL

- 12. Property of APC - Proprietary & Confidential Please do not copy or forward 12 Addendum 5: The Size of the Prize In realizing our Vision 2010 (Addendum 1), Amoco will have about $1 billion of assets with multiple GTL plants in operation and a portfolio rich in growth opportunities. We will have established growth platforms in the Caribbean, Middle East, and Pacific Rim providing methanol, and DME to chemical, olefin, power, and transportation fuel markets in the United States, India, and Far East. The value of the GTL business starts with a platform of individual projects upon which the value of future optionality is added. These projects are generally limited to upstream development and the GTL plant. However, optionality is created for future chemical feedstock, olefin, power, and transportation fuel projects. With the successful capture of the platform projects, the GTL business will contribute about $200 MM in annual net income and $240 MM in annual net cash flow by 2010. At that time, 80% of the capital expenditures will have been spent, with the largest single year expenditure of $270 MM spent in 2004. ROACE will reach and remain over 15% by 2007. By 2005, the business will have positive net cash flow and a payout by 2010. The full cycle PV10 (1/1/98) contribution from these projects is about $500 MM, with an overall IRR of 18%. The additional value from optionality comes as we expand the oxygenate value chain to include projects such as DMM, MTO, and chemical feedstocks. For example, 2,000 MTPD of methanol from the Atlas plant could be converted to 10,000 BPD of DMM. The DMM could then be shipped to our Texas City refinery and blended with gasoline to replace MTBE for environmental reasons. The PV10 (1/1/98) created by the DMM plant alone can range from $60-$100 MM. Expanding the value chain also mitigates the price risk for methanol. The reduced returns at Atlas are shifted and captured in the downstream segments. Since each of the projects in the platform creates optionality, the total value created by the GTL business could be well in excess of that described for the platform projects alone. M Monetize Stranded Gas Environmentally Friendly Power& TransportationFuel Chemical Feedstock GTL GTL PlantNatural Gas Project Platform 1999 2001 2003-4 2005-6 2006-7 2009-10 Titan Atlas Qatar/India DME Pacific Rim Oxygenate Equity Gas WI=100% Lurgi Technology WI=15% 2500 MTPD Methanol Saturn Markets Methanol T-O-P Price Floor Equity Gas WI=100% Lurgi Technology WI=35% 5000 MTPD MeOH Dme Option Process & EPC Cost guarantee Saturn Markets Methanol T-O-P Price Floor Niche DME market Captured Supply WI=17.5% Partners: QGPC, India combine H-T Technology WI=17.5% 7000 MTPD (MeOH eqv) 5300 MTPD DME Indian DME Markets Power Pacific Basin NW Shelf Indonesia Alaska DME/MeOH WI=35% 5000 MTPD Japan power Far East chemical feedstock DMM feedstock Expansion of India 1 except: Indian Markets Power Diesel Blending stock H-T Technology WI=20% 11,000 MTPD (MeOH eqv) DME & MeOH Expansion of India 2 Caribbean MeOH North Coast Trinidad Venezuela MeOH WI=50% 5000 MTPD USGC Olefins 2005-6 Qatar/India DME II Qatar/India DME III GTL GTL Plant DMM Plant Refinery Blended Diesel and Gasoline 0.00 2.00 4.00 6.00 8.00 10.00 12.00 Stranded Gas DME/ MeOH Upstream Diesel Additive DMM Gasoline Additive $/MMBTU

- 13. Property of APC - Proprietary & Confidential Please do not copy or forward 13 Certainty Financials for the 7 Projects in the Platform: Net Income $0 $100 $200 $300 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 $MM Capital Expenditures $0 $100 $200 $300 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 $MM Net Cash Flow ($200) ($100) $0 $100 $200 $300 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 $MM ROCE and Avg. Capital Employed 0% 5% 10% 15% 20% 25% 30% 35% 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 ROCE,% $0 $200 $400 $600 $800 $1,000 $1,200 ACE,$MM Goal 2010 Goal 2010 GTL M T S Monetize Stranded Gas Environmentally Friendly Chemical Feedstock Power&Transport Fuel