Downloaded 47 times

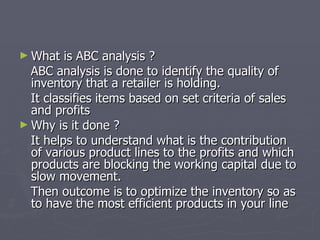

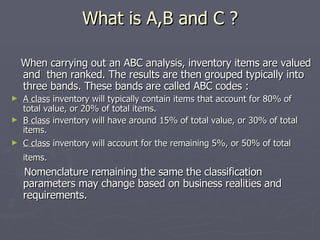

ABC analysis classifies inventory items into A, B and C categories based on their value and sales contribution. A items account for 80% of total value but only 20% of items. B items are 15% of value and 30% of items. C items are 5% of value but 50% of items. This analysis helps optimize inventory by increasing buying of A items and reducing or eliminating slow moving C items. This improves working capital, inventory efficiency and customer satisfaction.