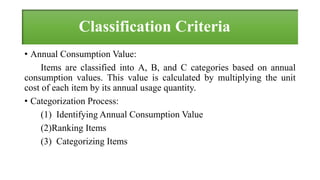

ABC analysis is a strategic inventory management technique that categorizes items into three groups (A, B, C) based on their importance or value, typically following the 80/20 rule where 80% of sales come from 20% of inventory. The classification is based on annual consumption value determined by unit cost and annual usage. This method benefits businesses by optimizing resource allocation, improving inventory control, and achieving cost savings.