4. 382,87981,84471,05184,40791,568107,137Cash and marketable

securities2,5872,1011,5563,1525,9445,9048,55310,0979,2435,7

266,0789,7539,0359,75212,083Current

assets11,55910,1778,79910,81913,33114,01418,45821,98222,07

019,50919,49921,85221,83622,48226,863Total

assets24,34823,02121,96223,86927,48631,60437,93344,95643,1

2845,81950,82352,39757,17061,73768,371Long term

debt2,0592,7102,3532,7132,1112,1572,1371,7521,3361,1374,55

36,5397,0687,0847,103Stockholders'

equity8,5687,3626,0787,5459,83812,26914,86018,49321,52922,

72823,23822,69014,75315,57421,659Senior debt

ratingAABBB+BBB+A-AAA-AA-AAAAAA-AAAACapital

expenditures2,7682,1622,6492,3333,5153,7373,3533,6744,7126,

6957,1635,7235,6976,7148,310Financial ServicesCash and

equivalents5091,2341,3762,1683,1753,1822,5551,739Total

sales8,09610,25313,26715,80616,23515,72516,95321,302Stock

price-

high$3.97$2.89$4.63$7.79$8.56$9.85$15.88$28.16$27.50$28.3

1$24.56$18.88$24.44$33.06$35.06Stock price-

low$2.01$1.75$1.85$3.81$5.50$6.69$8.96$14.22$19.03$20.69$

12.50$11.69$13.88$21.50$25.63Stock price-

close$2.22$1.86$4.32$7.06$7.60$9.67$14.06$18.84$25.25$21.8

1$13.31$14.06$21.44$32.25$27.88Shares outstanding, year

end1,085.21,085.21,085.31,098.01,116.61,116.61,073.61,015.09

81.6945.6946.2966.6979.0998.01,023.0Sources: annual reports,

Compustat, S&P Bond Record, casewriter estimates.1) Ford's

financial statistics presented above are for the automotive

operations only, except for the Financial Services lines as

noted. The stockholholders' equity account is for the entire

consolidated company, and thus may not be comparable to the

stockholders' equity accounts of GM and Chrysler, which were

taken from the equity method statements of their respective

annual reports (see footnote on the equity method in Exhibit 8).

Exhibit 8Exhibit 8 Historical Statements of Earnings for

Chrysler with CFC and Car Rental Operations on an Equity

Basis (in millions, except share price data)

5. (1)19801981198219831984198519861987198819891990199119

9219931994Sales of manufactured

products8,6009,97210,04513,24019,57321,25522,58626,27730,7

9031,03926,96526,70733,40941,24749,534Equity in earnings of

unconsolidated

subsids.(67)(56)(6)91126256270349336353292288131187237In

terest and other

income601020194212163238833026220323Total

Revenues8,5339,97610,04913,35119,71821,55322,97726,63231,

15831,43027,34027,02533,56641,65450,094Cost of goods

sold8,5848,9158,58510,85415,52817,46818,63521,30225,90126,

69123,37823,51927,42432,06637,485Depreciation of property

and

equipment26123319618327226423746458162864466780285391

2Amortization of special

tools306218237273283213307412540620617644641671961Selli

ng and administrative

expenses5565986707769881,1441,3771,6341,7481,8752,0172,1

352,4672,6193,146Pension

expense293288272255267220236470576544531796832749704N

onpension postretirement benefit

expense12681368762828Interest

expense27626215882(51)(125)32170150929107279240361228A

sset sales, investments,

restructurings224(144)(85)(503)(101)(205)(142)(265)Total

Expenses10,27610,51410,11812,64717,28719,18420,68024,4522

9,53730,86527,19327,83532,63237,81644,264Earnings Before

Taxes(1,743)(538)(69)7042,4312,3692,2972,1801,621565147(81

0)9343,8385,830Provision for income

taxes2917040293473590889061224279(272)4291,4232,117Chan

ge in accounting principles (2)(41)(36)(257)218(4,966)Net

Earnings

(Loss)(1,772)(555)(69)3021,4971,6341,3891,2901,05035968(79

5)723(2,551)3,713Selected Market InformationSenior debt

ratingNRNRNRBBBBBBBBBBBBBBBBBBBBBB-BB-

B+BBBBBB+Stock price-

6. high$5.17$3.39$8.28$15.83$15.00$20.89$31.42$48.00$27.88$2

9.63$20.38$15.88$33.88$58.38$63.50Stock price-

low$1.83$1.33$1.56$6.22$9.28$13.28$18.11$19.63$20.50$18.1

3$9.13$9.75$11.50$31.75$43.13Stock price-

close$2.17$1.50$7.89$12.28$14.22$20.72$24.67$22.13$25.75$

19.00$12.63$11.75$32.00$53.25$44.88Shares outstanding, year

end150.69164.55178.82274.08273.31227.80216.69221.22233.10

223.10224.80292.30295.90353.73355.06Sources: annual

reports, S&P Bond Record, and casewriter estimates.1) The

historical financial statements for Chrysler were taken from

statements prepared using the equity method rather than the

consolidated method. In the equity method, the financial

statements show accounts from the core business entity and then

add a summary account for the net effect of affiliates and

subsidiaries. For example, on the balance sheet, the asset

"Investments in unconsolidated subsidiaries and affiliates"

represents the sum of the assets (net of liabilities) of the

subsidiaries. On the income statement, the combined earnings of

subsidiaries and affiliates are added in one line called "Equity

in earnings of unconsolidated subsidiaries." In consolidated

statements, the individual subsidiary accounts are merged into

the parent accounts on a line-by-line basis.2) The large charge

in 1993 reflects new SFAS rule regarding accounting for

postretirement benefits other than pensions, net of a tax benefit

estimate.

Exhibit 9Exhibit 9 Historical Balance Sheets for Chrysler with

CFC and Car Rental Operations on an Equity Basis (in

millions)Assets:198019811982198319841985198619871988198

919901991199219931994Cash and

equivalents104121109112751482851,5421,5059591,4911,5052,

0093,7774,972Marketable

securities1942837889581,6252,6502,3948681,4461,1811,47369

69597072,643Total cash and marketable

securities2984048971,0701,7002,7982,6792,4102,9512,1402,96

42,2012,9684,4847,615Accounts receivable - trade and other

(net)4764302482913322083725781,137993695626936805459In

7. ventories1,9161,6001,1331,3011,6261,8631,6992,5522,9712,53

62,6092,4352,3302,4832,645Prepaid taxes, pension, and other

expenses17216791923224466136316645154175015437131,272P

roperty and

equipment1,7191,6491,6952,1362,6293,2774,3145,8496,2246,1

766,3937,2848,0978,82010,347Special

tools8017987789191,0841,3621,8042,4632,4652,4872,5072,640

2,8963,4553,643Investments in unconsolidated

subsidiaries1,0851,0591,2388621,2412,0702,2442,7212,8142,94

73,2413,7723,6873,6853,642Intangible

assets3872,1372,5434,2644,7424,5504,1363,8821,781Deferred

tax assets7411,4803,6421,951Other

assets1511621831011285822876047371,5739537945712,0514,7

22Total

Assets6,6186,2706,2636,7729,06212,60614,39919,94522,50623,

63124,52125,54427,64434,02038,077Liabilities:Accounts

payable1,1791,0238981,6292,3232,5052,9583,7224,3463,5753,9

844,3575,0136,0747,403Current portion of long-term

debt36128115445150297202285217283279745142499327Accru

ed liabilities and

expenses1,3639609166271,7431,9281,9612,6313,0473,2383,020

3,5923,7934,4225,333Long-term

debt2,4832,0592,1481,1047602,3662,3343,3333,3292,9653,944

3,6723,6432,2812,097Accrued noncurrent employee

benefits3536666369873622982907497132,9713,7534,3844,1871

0,5628,547Other noncurrent

liabilities2222783524324976056611,5262,0932,8612,6922,6853

,3283,3463,676Deferred income

taxes197223169178223927121,1961,179505Total

Liabilities6,1585,4905,2735,4085,7578,3919,11813,44214,9241

6,39817,67219,43520,10627,18427,383Shareholders'

Equity:Preferred stock5641,3191,321221222Common

stock419460500122124153229245245245245312312364364Add

itional paid-in

capital6926936932,2762,3251,9431,8672,3742,3762,3692,2912,

9053,6575,5335,536Retained

8. earnings(1,215)(1,692)(1,524)(1,255)9212,1533,5044,5815,3585

,2294,8133,3853,9241,1705,006Treasury stock - at

cost(65)(34)(319)(697)(397)(610)(500)(493)(357)(233)(214)Tot

al Shareholders'

Equity4607809901,3643,3054,2155,2816,5037,5827,2336,8496,

1097,5386,83610,694Total Liabilities and Shareholders'

Equity6,6186,2706,2636,7729,06212,60614,39919,94522,50623,

63124,52125,54427,64434,02038,077Sources: annual reports

and casewriter estimates.

Exhibit 10Exhibit 10 Historical Statements of Cash Flows for

Chrysler with CFC and Car Rental Operations on an Equity

Basis (in millions)Cash Flows from Operating

Activities:19801981198219831984198519861987198819891990

1991199219931994Net earnings

(loss)(1,772)(555)(69)3021,4971,6341,3891,2901,05035968(795

)723(2,551)3,713Adjustments to get to operating cash

flow:Depreciation and

Amortization5674514324575544765448761,1211,2481,2611,311

1,4431,5241,873Provision for restructuring

charges150929(101)Equity in earnings of unconsolidated

subs.67566(91)(126)(256)(270)(349)(336)(353)(292)(288)(131)(

187)(237)Plant capacity adjustment(391)Deferred income

taxes22546685663473(135)55(288)2298031,065Gain on sales of

auto assets and

investments(16)(126)(539)(205)(142)(265)Cumulative effect of

chng. in acctg. principles257(218)4,966Change in accounts

receivable1344784(165)390(445)12011369(300)131345Change

in

inventories(42)316332(212)(594)102163(493)(271)(26)(87)1741

59(171)(201)Change in prepaid expenses and other

assets(148)138(331)80(73)2574(1,587)(2,095)Change in

accounts payable and other

liabs.504(514)451,0241,029310487310900(874)(372)963953365

2,856Change in noncurrent assets and

liabilities3381(49)(41)339(351)(364)Dividends/earnings

received from

9. subsidiary6280100350Other(48)(6)216829041191572321993011

98199181224215Net Cash Provided by Operating

Activities(525)2558022,1213,2732,9702,4912,6932,3841,2101,1

201,0312,9713,2527,534Cash Flows from Investing

Activities:Purchase (sale) of non-core assets

(1)269(672)(555)Purchases of marketable

securities(2,598)(4,357)(6,779)(6,442)(14,188)(3,149)(3,412)Sa

les and maturities of marketable

securities3116302,0214,6216,4877,21713,9253,4011,463Procee

ds from sale of assets

(2)(39)(29)(185)245(252)(519)(15)(131)59882010021546162Ne

t expenditures for property and

equipment(319)(122)(85)(634)(760)(1,043)(1,287)(1,234)(987)(

932)(1,034)(1,482)(1,374)(1,738)(2,611)Expenditures for

special

tools(395)(214)(227)(415)(447)(492)(749)(655)(557)(651)(663)

(708)(872)(1,234)(1,177)Other(43)(44)1(12)13(2)(35)138(315)(

214)(121)(209)(13)77Net Cash Used in Investing

Activities(796)(409)(227)(816)(1,459)(2,713)(1,742)(1,980)(1,9

83)(1,036)(1,383)(1,436)(2,503)(2,272)(5,598)Cash Flows from

Financing Activities:Change in Short-term

debt5013(24)282(354)29(113)(10)16(9)12249(165)1440Long-

term

borrowings1,157432112201031,8341381,082118251,254183392

32Payments on long-term

borrowings(64)(185)(70)(1,583)(508)(65)(141)(815)(323)(247)(

343)(37)(497)(1,021)(412)Net common and preferred stock

proceeds11163(315)(843)(291)(391)3858361,952Dividends

paid(117)(121)(115)(153)(214)(225)(268)(269)(169)(225)(281)(

399)Other213(1)4(5)(23)(221)3184810128Net Cash Provided by

Financing

Activities1,144261(82)(1,133)(1,182)839(556)(353)(437)(720)7

9541936788(741)Change in cash and cash

equivalents(177)1074931726321,096193360(36)(546)53214504

1,7681,1951) Reflects purchase of Chrysler Defense in 1982,

Gulfstream Aerospace in 1985, and AMC and ESI in 1987.2)

10. Reflects proceeds from sale of Gulfstream Aerospace in

1990.Sources: annual reports and casewriter estimates.

Exhibit 11Exhibit 11 Chrysler Projected Income Statements,

1994-1998E (in millions)19941995E1996E1997E1998ESales of

manufactured products49,53453,23956,03759,49756,894Equity

in earnings of unconsolidated

subsidiaries237164200200200Interest and other

income323191300300300Total

Revenues50,09453,59456,53759,99757,394Cost of goods

sold37,48540,03442,19644,78443,325Depreciation of property

and equipment9129209801,0501,010Amortization of special

tools9611,0801,1501,2001,160Selling and administrative

expense3,1463,2803,4743,6293,647Pension

expense704650630610590Nonpension postretirement benefit

expense828750740730730Interest

expense228228210205190Total

Expenses44,26446,94249,38052,20850,652Earnings Before

Taxes5,8306,6527,1577,7896,742Provision for income

taxes2,1172,5942,7913,0382,630Net

Income3,7134,0584,3664,7514,112

Exhibit 12Exhibit 12 Chrysler Projected Cash Flows, 1994-

1998E (in millions, except per share

data)19941995E1996E1997E1998ENet

Income3,7134,0584,3664,7514,112Depreciation9129209801,050

1,010Amortization of special

tools9611,0801,1501,2001,160Equity in unconsolidated

subsidiaries(237)(164)(200)(200)(200)Deferred taxes

(1)1,0659791,0381,1211,121Change in net working

capital1,1200000Total

Sources7,5346,8737,3347,9227,203Capital

expenditures3,7883,2003,1003,1003,100Debt

payments37019030350350Stock repurchases01,000000Net

equity interest sales1,7200000Total

Uses5,8784,3903,1303,4503,450Net Cash

Flow1,6562,4834,2044,4723,753Net cash flow per

share4.066.2710.8411.539.67Dividends on common and

11. preferred399660726798800Excess Cash

Flow1,2571,8233,4783,6742,953Source: compiled from Morgan

Stanley research reports.1) The deferred tax add-back represents

the amount by which income taxes for financial reporting

exceed the cash outflow computed for tax accounting.

Exhibit 13Exhibit 13 Betas for the Big Three, April,

1995Chrysler1.30General Motors1.15Ford1.15Source: Value

Line

Exhibit 14Exhibit 14 Financial Market Data, April 1995I.

Treasury Yields90 day5.818%Six months6.075One

year6.316Five years6.946Ten years7.112Thirty years7.395II.

Corporate Borrowing RatesLong Term Bond

YieldsAaa8.08%Aa8.19A8.28Baa8.65Sources: Federal Reserve

Bulletin, Bloomberg, Value Line

· My Bookshelf

· TOC/Annotation menu

· Downloads

· Print

· Search

· Profile

· Help

Chapter 18 Partners HealthCare System

Previous section

Next section

18 Partners HealthCare System

Thomas H. Davenport

Partners HealthCare System (Partners) is the single largest prov

ider of healthcare in the Boston area. It consists of 12 hospitals,

with morethan 7,000 affiliated physicians. It has 4 million outp

atient visits and 160,000 inpatient admissions a year. Partners is

a nonprofitorganization with almost $8 billion in revenues, and

it spends more than $1 billion per year on biomedical research.

It is a major teachingaffiliate of Harvard Medical School.

Partners is known as a “system,” but it maintains substantial aut

onomy at each of its member hospitals. While some information

12. systems(the electronic medical record, for example) are standar

dized across Partners, other systems and data, such as patient sc

heduling, arespecific to particular hospitals. Analytical activitie

s also take place both at the centralized Partners level and at ind

ividual hospitals such asMassachusetts General Hospital (MGH)

and Brigham and Women’s Hospital (usually described as “the

Brigham”). In this chapter, bothcentralized and hospital-

specific analytical resources are described. The focus for hospit

al-

specific analytics is the two major teachinghospitals of Partners

—MGH and the Brigham—

although other Partners hospitals also have their own analytical

capabilities and systems.

Centralized Data and Systems at Partners

The basis of any hospital’s clinical information systems is the cl

inical data repository, which contains information on all patient

s, theirconditions, and the treatments they have received. The in

patient clinical data repository for Partners was initially implem

ented at theBrigham during the 1980s. Richard Nesson, the Brig

ham and Women’s CEO, and John Glaser, the hospital’s chief in

formation officer,initiated an outpatient electronic medical reco

rd (EMR) at the Brigham in 1989.1 This EMR contributed outpa

tient data to the clinical datarepository. The hospital was one of

the first to embark on an EMR, though MGH had begun to deve

lop one of the first full-function EMRs asearly as 1976.

A clinical data repository provides the basic data about patients.

Glaser and Nesson came to agree that in addition to a repositor

y and anoutpatient EMR, the Brigham—

and Partners after 1994, when Glaser became its first CIO—

needed facilities for doctors to input onlineorders for drugs, test

s, and other treatments. Online ordering (called CPOE, or Comp

uterized Provider Order Entry) would not only solvethe time-

honored problem of interpreting poor physician handwriting, but

could also, if endowed with a bit of intelligence, check whether

aparticular order made sense or not for a particular patient. Did

a prescribed drug comply with best-

13. known medical practice, and did thepatient have any adverse rea

ctions in the past to it? Had the same test been prescribed six ti

mes before with no apparent benefit? Was thespecialist to whom

a patient was being referred covered by his or her health plan?

With this type of medical and administrative knowledgebuilt int

o the system, dangerous and time-

consuming errors could be prevented. The Brigham embarked on

its CPOE system in 1989.

Nesson and Glaser knew that there were other approaches to red

ucing medical error than CPOE. Some provider institutions, suc

h asIntermountain Healthcare in Utah, were focused on close ad

herence by physicians to well-

established medical protocols. Others, like KaiserPermanente in

California and the Cleveland Clinic, combined insurance and m

edical practices in ways that incented all providers to workjointl

y on behalf of patients. Nesson and Glaser admired those approa

ches, but felt that their impact would be less in an academic me

dicalcenter such as Partners, where physicians were somewhat a

utonomous, and individual departments prided themselves on th

eir separatereputations for research and practice innovations. Co

mmon, intelligent systems seemed like the best way to improve

patient care atPartners.

In 1994, when the Brigham and Mass General combined as Partn

ers HealthCare System, there was still considerable autonomy fo

rindividual hospitals in the combined organization. However, fr

om the onset of the merger, the two hospitals agreed to use a co

mmonoutpatient EMR called the longitudinal medical record (L

MR) and a CPOE system, both of which were developed at the B

righam. This waspowerful testimony in favor of the LMR and C

POE systems, since there was considerable rivalry between the t

wo hospitals, and MassGeneral had its own EMR.

Perhaps the greatest challenge was in getting the extended netw

ork of Partners-

affiliated physicians up on the LMR and CPOE. Thephysician n

etwork of more than 6,000 practicing generalist and specialist p

hysician groups was scattered around the Boston metropolitanar

14. ea, and often operated out of their own private offices. Many lac

ked the IT or telecom infrastructures to implement the systems

on theirown, and implementation of an outpatient EMR cost abo

ut $25,000 per physician. Yet full use of the system across Partn

ers-

affiliatedproviders was critical to a seamless patient experience

across the organization.

Glaser and the Partners information systems (IS) organization w

orked diligently to spread the LMR and CPOE to the growing nu

mber ofPartners hospitals and to Partners-

affiliated physicians and medical practices. To assist in bringin

g physicians outside the hospitals onboard, Partners negotiated

payment schedules with insurance companies that rewarded phy

sicians for supplying the kind of informationavailable from the

LMR and CPOE. By 2007, 90% of Partners-

affiliated physicians were using the systems, and by 2009, 100%

were. By2009, more than 1,000 orders per hour were being ente

red through the CPOE system across Partners.

The combination of the LMR and the CPOE proved to be a powe

rful one in helping to avoid medical error. Adverse drug events,

or the useof the wrong drug for the condition or one that caused

an allergic reaction in the patient, typically were encountered b

y about 14 of every1,000 inpatients. At the Brigham before LM

R and CPOE, the number was about 11. After the widespread im

plementation of these systems atBrigham and Women’s, there w

ere just above five adverse drug events per 1,000 inpatients—

a 55% reduction.

Managing Clinical Informatics and Knowledge at Partners

The Clinical Informatics Research & Development (CIRD) grou

p, headed by Blackford Middleton, is one of the key centralized

resources forhealthcare analytics at Partners. Many of CIRD’s st

aff, like Middleton, have multiple advanced degrees; Middleton

has an MD, a Master ofPublic Health degree, and a Master of Sc

ience in Health Services Research.

The mission of CIRD is

to improve the quality and efficiency of care for patients at Part

15. ners HealthCare System by assuring that the most advancedcurr

ent knowledge about medical informatics (clinical computing) is

incorporated into clinical information systems at PartnersHealt

hCare.2

CIRD is part of the Partners IS organization. It was CIRD’s role

to help create the strategy for how Partners used information sy

stems inpatient care, and to develop both production systems ca

pabilities and pilot projects that employ informatics and analyti

cs. CIRD’s work hadplayed a substantial role in making Partner

s a worldwide leader in the use of data, analysis, and computeri

zed knowledge to improvepatient care. CIRD also has had sever

al projects funded by U.S. government health agencies to adapt

some of the same tools andapproaches it developed for Partners

to the broader healthcare system.

One key function of CIRD was to manage clinical knowledge, a

nd translate healthcare research findings into daily medical prac

tice atPartners. In addition to facilitating adoption of the LMR a

nd CPOE, Partners faced a major challenge in getting control of

the clinicalknowledge that was made available to care provider

s through these and other systems. The “intelligent CPOE” strat

egy demanded thatknowledge be online, accessible, and easily u

pdated so that it could be referenced by and presented to care pr

oviders in real-

timeinteractions with patients. There were, of course, a variety

of other online knowledge tools, such as medical literature searc

hing, available toPartners personnel; in total they were referred

to as the “Partners Handbook.” At one point after use of the CP

OE had become widespreadat Brigham and Women’s, a compari

son was made between online usage of the Handbook and usage

of the knowledge base from orderentry. There were more than 1

3,000 daily accesses through the CPOE system at the Brigham a

lone, and only 3,000 daily accesses of theHandbook by all Partn

ers personnel at all hospitals. Therefore, there was an ongoing e

ffort to ensure that as much high-

quality knowledgeas possible made it into the CPOE.

The problem with knowledge at Partners was not that there wasn

16. ’t enough of it; indeed, the various hospitals, labs, departments,

andindividuals were overflowing with knowledge. The problem

was how to manage it. At one point, Tonya Hongsermeier, a phy

sician with anMBA degree who was charged with managing kno

wledge at Partners, counted the number of places around Partner

s where there wassome form of rule-

based knowledge about clinical practice that was not centrally

managed. She found about 23,000 of them. The knowledgewas c

ontained in a variety of formats: paper documents, computer “sc

reen shots,” process flow diagrams, references, and data or repo

rtson clinical outcomes—

all in a variety of locations, and only rarely shared.

Hongsermeier set out to create a “knowledge engineering and m

anagement” factory that would capture the knowledge at Partner

s, put it ina common format and central repository, and make it

available for CPOE and other online systems. This required not

only a new computersystem for holding the thousands of rules t

hat constituted the knowledge, but an extensive human system f

or gathering, certifying, andmaintaining the knowledge. It consi

sted of the following roles and organizations:

• A set of committees of senior physicians who oversaw clinical

practice in various areas, such as the Partners Drug TherapyCo

mmittee, which reviewed and sanctioned the knowledge as corre

ct or best known practice

• A group of subject matter experts who, using online collaborat

ion systems, debated and refined knowledge such as the best dru

g fortreating high cholesterol under various conditions, or the b

est treatment protocol for diabetes patients

• A cadre of “knowledge editors” who took the approved knowle

dge from these groups and put it into a rule-

based form that wouldbe accepted by the online knowledge repo

sitory

High Performance Medicine at Partners

Glaser and Partners IS had always had the support of senior Part

ners executives, but for the most part their involvement in the a

ctivitiesdesigned to build Partners’ informatics and analytics ca

17. pabilities was limited to some of the hospitals and those physici

an practices thatwanted to be on the leading edge. Then Jim Mo

ngan moved from being president of MGH (a role he had occupi

ed since 1996, shortly afterthe creation of Partners) to being CE

O of Partners overall in January 2003. Not since Dick Nesson ha

d Glaser had such a strong partner inthe executive suite.

Mongan had come to appreciate the value of the LMR and CPO

E, and other clinical systems, while he headed Mass General. B

ut when hecame into the Partners CEO role, with responsibility

over a variety of diverse and autonomous institutions, he began

to view it differently.Mongan said:

So when I was preparing to make the move to Partners, I began t

o think about what makes a health system. One of the keys that

would unite us was the electronic record. I saw it as the connect

ive tissue, the thing we had in common, that could help us get a

handle on utilization, quality, and other issues.

Together Mongan and Glaser agreed that while Partners already

had strong clinical systems and knowledge management compar

ed toother institutions, a number of weaknesses still needed to b

e addressed (most importantly that the systems were not univers

ally usedacross Partners care settings), and steps needed to be ta

ken to get to the next level of capability. Working with other cli

nical leaders atPartners, they began to flesh out the vision for w

hat came to be known as the High Performance Medicine (HPM)

initiative, which took placebetween 2003 and 2009.

Glaser commented on the process the team followed to specify t

he details of the HPM initiative:

Shortly after he took the reins at Partners, however, Jim had a cl

ear idea on where he wanted this to go. To help refine that visio

n,several of us went on a road trip, to learn from other highly in

tegrated health systems such as Kaiser, Intermountain Healthcar

e,and the Veterans Administration about ways we might bring th

e components of our system closer together.

Mongan concluded:

We also were working with a core team of 15-

20 clinical leaders and eventually came up with a list of seven o

18. r eight initiatives,which then needed to be prioritized. We did a

“Survivor”-

style voting process, to determine which initiatives to “kick off

the island.”That narrowed down the list to five Signature Initiati

ves.

The five initiatives consisted of the following specific programs

, each of which was addressed by its own team:

• Creating an IT infrastructure—

Much of the initial work of this program had already been done;

it consisted of the LMR and theCPOE, which was extended to t

he other hospitals and physician practices in the Partners networ

k and maintained. This project alsoaddressed patient data qualit

y reporting, further enhancement of knowledge management pro

cesses, and a patient data portal togive patients access to their o

wn health information.

• Enhancing patient safety—

The team addressing patient safety issues focused on four specif

ic projects: 1) providing decisionsupport about what medication

s to administer in several key areas, including renal and geriatri

c dosing; 2) communicating “clinicallysignificant test results,”

particularly to physicians after their patients have left the hospit

al; 3) ensuring effective flow of informationduring patient care t

ransitions and handoffs in hospitals and after discharge; 4) prov

iding better decision support, patient education,and best practic

es and metrics for anticoagulation management.

• Uniform high quality—

This team addressed quality improvement in the specific domain

s of hospital-

based cardiac care,pneumonia, diabetes care, and smoking cessa

tion; it employed both registries and decision support tools to d

o so.

• Chronic disease management—

The team addressing disease management focused on prevention

of hospital admission byidentifying Partners patients who were

at highest risk for hospitalization, and then developed health co

aching programs to addresspatients with high levels of need, for

19. example, heart failure patients; the team also pulled together a

new database of informationabout patient wishes about end-of-

life decisions.

• Clinical resource management—

At Jim Mongan’s suggestion, this team focused on how to lower

the usage of high-cost drugs andhigh-

cost imaging services; it employed both “low-

tech” methods (e.g., chart reviews) and “high-

tech” approaches (e.g., a datawarehouse making transparent phy

sicians’ imaging behaviors relative to peers) to begin to make u

se of scarce resources moreefficiently.

Overall, Partners spent about $100 million on HPM and related

clinical systems initiatives, most of which were ultimately paid

for by thePartners hospitals and physician practices that used th

em. To track progress, a Partners-

wide report, called the HPM Close, was developedthat shows cu

rrent and trend performance on the achievement of quality, effic

iency, and structural goals. The report was publishedquarterly t

o ensure timely feedback for measuring performance and suppor

ting accountability across Partners.

New Analytical Challenges for Partners

Partners had made substantial progress on many of the basic app

roaches to clinical analytics, but there were many other areas at

theintersection of health and analytics that it could still address.

One was the area of personalized genetic medicine—

the idea that patientswould someday receive specific therapies b

ased on their genomic, proteomic, and metabolic information. P

artners had created the i2b2(Informatics for Integrating Biology

and the Bedside), a National Center for Biomedical Computing

that was funded by the NationalInstitutes of Health. John Glaser

was co-

director of i2b2 and developed the IT infrastructure for the Part

ners Center for PersonalizedGenetic Medicine. One of the many

issues these efforts addressed in personalized genetic medicine

was how relevant genetic informationwould be included in the L

MR.

20. Partners was also attempting to use clinical information for post

market surveillance—

the identification of problems with drugs and medicaldevices in

patients after they have been released to the market. Some Partn

ers researchers had identified dangerous side effects fromcertain

drugs through analysis of LMR data. Specifically, research scie

ntist John Brownstein’s analyses suggested that the level of pati

entswith heart attack admissions to Mass General and the Brigh

am had increased 18% beginning in 2001 and returned to its bas

eline level in2004, which coincided with the timeframe for the b

eginning and end of Vioxx prescriptions. Thus far the identifica

tion of problems hadtaken place only after researchers from oth

er institutions had identified them, but Partners executives belie

ved it had the ability to identifythem at an earlier stage. The ins

titution was collaborating with the Food and Drug Administratio

n and the Department of Defense toaccelerate the surveillance p

rocess. John Glaser noted:

I don’t know that we’ll get as much specificity as might be need

ed to really challenge whether a drug ought to be in a market, b

ut Ialso think it’s fairly clear that you can be much faster and in

volve much fewer funds, frankly, to do what we would call the “

canaryin the mine” approach.3

Partners was also focused on the use of communications technol

ogies to improve patient care. Its Center for Connected Health,

headed byDr. Joe Kvedar, developed one of the first physician-

to-

physician online consultation services in an academic medical s

etting. The Center wasalso exploring combinations of remote m

onitoring technologies, sensors (for example, pill boxes that kno

w whether today’s dosage hasbeen taken), and online communic

ations and intelligence to improve patient adherence to medicati

on regimes, engagement in personalhealth, and clinical outcome

s.

In the clinical knowledge management area, Partners had done a

n impressive job of organizing and maintaining the many rules a

ndknowledge bases that informed its “intelligent” CPOE system.

21. However, it was apparent to Glaser, Blackford Middleton, and

TonyaHongsermeier—

and her successor as head of knowledge management, Roberto R

ocha—

that it made little sense for each medicalinstitution to develop it

s own knowledge base. Therefore, Partners was actively engage

d in helping other institutions with the managementof clinical k

nowledge. Middleton (the principal investigator), Hongsermeier,

Rocha, and at least 13 other Partners employees were involvedi

n a major Clinical Decision Support Consortium project funded

by the U.S. Agency for Healthcare Research and Quality. The c

onsortiuminvolved a variety of other research institutions and h

ealthcare companies, and was primarily focused on finding ways

to make clinicalknowledge widely available to healthcare provi

ders through EMR and CPOE systems furnished by leading vend

ors.

Despite all these advances, not all Partners executives and physi

cians had fully bought into the vision of using smart informatio

n systems toimprove patient care. Some found, for example, the

LMR and CPOE to be invasive in the relationship of doctor and

patient. A seniorcardiologist at Brigham and Women’s, for exa

mple, argued in an interview [with the author] that:

I have a problem with the algorithmic approach to medicine. Pe

ople end up making rote decisions that don’t fit the patient, and

itcan also be medically quite wasteful. I don’t have any choice h

ere if I want to write prescriptions—

virtually all of them are doneonline. But I must say that I am ge

tting alert fatigue. Every time I write a prescription for nitrogly

cerine, I am given an alert thatasks me to ensure that my patient

isn’t on Viagra. Don’t you think I know that at this point? As f

or online treatment guidelines, Ibelieve in them up to a point. B

ut once something is in computerized guidelines it’s sacrosanct,

whether or not the data arelegitimate. Recommendations should

be given with notification of how certain we are about them....

Maybe these things are moreuseful to some doctors than others.

If you’re in a subspecialty like cardiology you know it very well

22. . But if you are an internist, youmay have shallow knowledge, b

ecause you have to cover a wide variety of medical issues.

Many of the people involved in developing computer systems fo

r patient care at Partners regarded these as valid concerns. “Aler

t fatigue,”for example, had been recognized as a problem within

Blackford Middleton’s group for several years. They had tried t

o eliminate the moreobvious alerts, and to make changes in the

system to allow physicians to modify the types of alerts they rec

eived. There was a difficult lineto draw, however, between savi

ng physician attention and saving lives.

Centralized Business Analytics at Partners

While much of the centralized analytical activity at Partners has

been on the clinical side, the organization is also making progr

ess onbusiness analytics. The primary focus of these efforts is o

n financial reporting and analysis.

For several years, for example, Partners has employed an extern

al “software as a service” tool to provide reporting on the organ

ization’srevenue cycle. It has also developed several customized

analytics applications in the areas of cash management, underp

ayments, bad debtreserves, and charge capture. These activities

primarily took place in the Partners Revenue Finance function.

The Partners Information Systems organization is also increasin

g its focus on administrative and financial analytics. It is puttin

g in placeCompass, a common billing and administrative system

, at all Partners hospitals. At the same time, Partners has created

a set of standardprocesses for collecting, defining, and modifyi

ng financial and administrative data. Further, as one article put i

t:

At Partners, John Stone, corporate director for financial and ad

ministrative systems, is developing a corporate center of busine

ssanalytics and business intelligence. Some 12 to 14 financial e

xecutives will oversee the center, define Partners’ strategy for d

atamanagement, and determine data-

related budget priorities. “Our analysts spend the majority of th

eir time gathering, cleaning, andscrubbing administrative data a

nd less time providing value-

23. added analytics and insight into what the data is saying,” says S

tone.“We want to flip that equation so our analysts are spending

more time producing a story that goes along with the data.”4

Hospital-Specific Analytical Activities—

Massachusetts General Hospital

MGH, because it was a highly research-

driven institution, had long focused primarily on clinical resear

ch and the resulting clinicalinformatics and analytics. In additio

n to the LMR and CPOE systems used by Partners overall, MGH

researchers and staff have developed anumber of IT tools to an

alyze and search clinical data, one of which was a tool that sear

ched across multiple enterprise clinical systems,including the L

MR.

While historically, the research, clinical, information systems, a

nd the analytically focused business arms of MGH tended to ope

rate in stovepipes, the challenges of an evolving healthcare land

scape have forced a change in that paradigm. For instance, a str

ong current focus withinMGH is on how to achieve federal “mea

ningful use” reimbursement for the organization’s expenditures

on EMR. Because achievingmeaningful use objectives is predica

ted on a high level of coordination among information systems,

the physicians, and businessintelligence, people like David Y. T

ing, the associate medical director for Information Systems for

MGH and Massachusetts GeneralPhysicians Organization, and C

hris Hutchins, the director of Finance Systems and deputy CIO,

are beginning to collaborate extensively.

The HITECH/ARRA criteria for Stage 1 EMR meaningful use pr

escribe 25 specific objectives to incentivize providers to adopt a

nd useelectronic health records.5

To raise the level of EMR use by all its providers, as well as to

provide resources for the work needed to achieve that level, MG

H has arrivedat a novel funds distribution model. They determin

ed that the physicians organization will reserve a portion of the

pool of $44,000 perphysician toward IT and analytics infrastruct

ure, then distribute the remaining incentive payment across all p

roviders, proportional to theamount of data a particular physicia

24. n is charged with entering. An internal quality incentive progra

m would serve as the distributionmechanism. So, for example, if

you recorded demographics, vital signs, and smoking status for

the requisite number of patients, you wouldreceive 30% of the p

er-

physician payment from the pool. If you fulfilled all ten quality

measures, you would receive 100% of the paymentfrom the pool

. This encourages all physicians to contribute to the meaningful

use program, but it also means that no physicians will receiveth

e full amount of $44,000. The incentive from the federal govern

ment is up to $44,000 for each eligible provider who fulfills the

meaningful use criteria. MGH has examined the objectives and

broken them down into ten major pieces of patient data that phy

sicians needto record in the EMR. However, many are not releva

nt for all of its physicians. For example, a primary care physicia

n would logically entersuch data as demographics, vital signs, a

nd smoking status, but these would be less relevant for certain s

pecialists to enter.

Clearly, such a complex quality incentive model requires an unp

recedented level of analytics. Currently, Ting, Hutchins, and oth

ers at MGHare working to map the myriad clinical and finance d

ata sources that are scattered among individual departments, exi

st at a hospital sitelevel, or exist at the Partners enterprise level.

Simultaneously, they must negotiate data governance agreemen

ts even among other Partnersentities, to ensure that the requisite

data feeds from sources within Partners and pertaining to MGH

, but stored outside MGH’s physical datawarehouses, are availa

ble for MGH analytics purposes.

MGH has some experience with reimbursement metrics based on

physician behaviors, having used them in Partners Community

HealthCare, Inc. (PCHI), its physician network in the Boston ar

ea. Physician incentives have been provided through PCHI on th

e basis ofadmission rates, cost-

effective use of pharmacy and imaging services, and screening f

or particular diseases and conditions, such as diabetes. This was

also the mechanism used to encourage the adoption of the LMR

25. and CPOE systems by physicians. But MGH, like otherprovider

s, struggles with developing clear and transparent metrics across

the institution that can help to drive awareness and newbehavio

rs. If MGH could create broadly accessible metrics on individua

l physicians’ frequency of prescribing generic drugs, for exampl

e, itwould undoubtedly drive MGH’s competitive physicians to

excel in the rankings.

On the business side, MGH is trying to develop a broad set of c

apabilities in business intelligence and analytics. A BusinessInt

elligence/Performance Management group has recently been cre

ated under the direction of Chris Hutchins, deputy CIO and dire

ctor offinance systems for the Mass General Physicians Organiz

ation (MGPO). The group is generating reports on such financia

l and administrativetopics as

• Billing efficiency, claims adjudication, rejection rates, and tim

es to resolve billing accounts, both at MGH overall and across p

ractices

• Improving patient access, average wait times to see a physicia

n, and cancellation and no show rates

• Employer attrition as an MGH customer

MGH is also working with CMS on the Physician Quality Repor

ting Initiative. To combine all these measures in a meaningful f

ashion, MGPO isalso working on a balanced scorecard.6

While the current analytical activity is largely around reporting,

Hutchins plans to develop more capabilities around alerts, exce

ptionreporting, and predictive models. The MGH Physicians Or

ganization is implementing capabilities for statistical and predic

tive analytics thatwould be applied to several topics. For examp

le, one key area in which better prediction would be useful invo

lves patient volume. They arealso pursuing more general models

that would predict shifts in business over time. At the moment,

however, Hutchins feels that thescorecard is still early in its dev

elopment and current efforts are focused on identifying leading

indicators.

Hospital-Specific Analytical Activities—

Brigham and Women’s Hospital

26. Like MGH, the Brigham’s analytical activities in the past have

been largely focused on clinical research. Today it is also addre

ssing much ofthe same business, operational, and meaningful us

e issues that MGH is. Many of the analytical activities at the Br

igham are pursued by theCenter for Clinical Excellence (CCE),

which was founded by Dr. Michael Gustafson in 2001. The cent

er has five functionally interrelatedsections, including

• Quality programs

• Patient safety

• Performance improvement

• Decision support systems (including all internal and external d

ata management and reporting activities)

• Analysis and planning (which oversees business plan develop

ment, ROI assessments for major investments, cost benchmarkin

g,asset utilization reporting, and support for strategic planning)

The CCE has close working relationships with the Brigham’s C

FO and finance organizations, the Brigham’s information syste

msorganization, the Partners Business Development and Plannin

g function, and other centers and medical departments at the Bri

gham.

One major difference between the Brigham and MGH (and most

other hospitals, for that matter) is that the Brigham established

a balancedscorecard beginning in 2000. It was based on a well-

established cultural orientation to operational and quality metric

s throughout thehospital. Richard Nesson, the Brigham CEO wh

o had partnered with CIO John Glaser to introduce the LMR and

CPOE systems, was also astrong advocate of information-

driven decision making on both the clinical and business sides o

f the hospital. The original systems thatNesson and Glaser had e

stablished also incorporated a reporting tool called EX, and a da

ta warehouse called CHASE (ComputerizedHospital Analysis Sy

stem for Efficiency). The analyses and data from these systems

formed the core of the Brigham’s balanced scorecard.

Before an effective scorecard could be developed, the Brigham

had to undertake considerable work on data definitions and man

agement.One analysis discovered, for example, that there were f

27. ive different definitions of the length of a patient stay circulatin

g in 11 differentreports. The chief medical officer at the time, D

r. Andy Whittemore, and the CCE’s Dr. Gustafson, a surgeon w

ho had just taken on qualitymeasurement issues at the Brigham,

addressed these data issues with a senior executive steering com

mittee and decided to present thedata in an easy-to-

digest scorecard.

Under the ongoing management of the CCE, the scorecard conta

ins a variety of financial, operational, and clinical metrics from

across thehospital. The choice of metrics is driven by a “strateg

y map”7 specifying the relationships among key variables that d

rive the performance ofthe hospital (see Figure 18.1). Unlike m

ost corporate strategy maps, financial performance variables are

at the bottom of the map ratherthan the top. In the scorecard its

elf, there are more than 50 specific measures in the hospital-

wide scorecard, and more detailed scorecardsfor particular depa

rtments, such as Nursing and Surgery. The scorecard has also be

en extended to Faulkner Hospital, a Partners institutionthat is m

anaged jointly with the Brigham.

Figure 18.1 Strategy map for Brigham & Women’s balanced sco

recard

Dr. Gary Gottlieb, the Brigham president from 1992 to 2009, wa

s the most aggressive user of the scorecard. He noted:

I review the balanced scorecard on a regular basis, because ther

e is specific data that is of interest to me. There are key metrics

Iexamine for trends and if they develop, then I analyze the data

to better understand what is going right or wrong. It is one view

,but an important one of our hospital. I can look at the balanced

scorecard and get information in another way, from a differentp

erspective than I can when I’m making rounds on a hospital unit

, or sitting in the meeting with chiefs.8

Gottlieb left the Brigham CEO role to become the CEO of Partn

ers overall in 2010. One of the primary initiatives in his new Pa

rtners role isto expand the degree of common systems throughou

t Partners, so that there can be common data and analytics throu

28. ghout theorganization. Perhaps one day all of Partners HealthCa

re System will be managed through one scorecard.

Notes

1. This and other details of the Partners LMR/CPOE systems are

derived from Richard Kesner, “Partners Healthcare System:Tra

nsforming Healthcare Services Delivery Through Information M

anagement,” Ivey School of Business Case Study (2009).

2. “CIRD, Clinical Informatics Research & Development,” http:

//www.partners.org/cird/.

3. PricewaterhouseCoopers, “Partners HealthCare: Using EHR

Data for Post-

market Surveillance of Drugs” (2009). http://pwchealth.com/cgi

-local/hregister.cgi/reg/partners_healthcare_case_study.pdf.

4. Healthcare Financial Management Association, “Developing

a Meaningful EHR,” http://www.hfma.org/Publications/Leaders

hip-Publication/Archives/Special-Reports/Spring-

2010/Developing-a-Meaningful-

EHR/, Part 3 of “Leadership Spring-

Summer 2010Report: Collaborating for Results.”

5. The 25 meaningful use criteria are described in “Eligible Pro

vider: ‘Meaningful Use’ Criteria,” by Jack Beaudoin, Healthcar

e IT News,December 30, 2009, http://www.healthcareitnews.co

m/news/eligible-provider-meaningful-use-criteria.

6. Robert S. Kaplan and David P. Norton, “The Balanced Scorec

ard: Measures that Drive Performance,” Harvard Business Revie

w (January– February 1992).

7. Robert S. Kaplan and David P. Norton, “Having Trouble With

Your Strategy? Then Map It,” Harvard Business Review (Septe

mber –October, 2000).

8. Ibid.

· Notebook

Davenport, T., & McNeill, D. (2014). Analytics in healthcare

and the life sciences: Strategies,implementation, methods, and

best practices. Retrieved from https://content.ashford.edu

29. LSE - FM474

Questions:

Below you will find a number of questions that I want you to

address in your analysis

(approximate % weighting of each question is provided in

parentheses).

1. Evaluate Chrysler’s past performance. Is there evidence of

mismanagement? (25%)

a. Evaluate Chrysler’s financial and operating performance

between 1980-1992.

What financial and investment policies did they pursue and

why? How

successful were they?

b. What should Chrysler’s capital structure look like? What

payout policies

should they pursue? How does that compare with the policies

pursued by

current management?

2. What is the intrinsic value of a share of Chrysler stock? How

does that value compare to

the market’s valuation? (45%)

• When it comes to the capital structure assumptions, one can

imagine a number of

different alternatives, for example

30. 1. Assume that the firms debt will be kept at some constant

amount D.

2. Assume that Chrysler will follow some specific borrowing

and repayment

schedule for a number of years, after which the leverage policy

will be kept

constant.

3. Evaluate the structure of Kerkorian’s proposed deal in detail.

Does it make sense? What

risks are involved? Use the downturn of 1988-1991 to model

another downturn scenario.

(30%)

Assumptions:

• Market risk premium: 6%

• Tax rate: 39%

• Deferred taxes should be added back, since it is a non-cash

expense. (This is tax that

we owe, but do not presently have to pay to the IRS)

• Equity in unconsolidated subsidiaries is strictly speaking not a

cash income, which

implies that it is not part of the free cash flow. The equity stake

is valuable, however,

and should therefore be added to the value of the firm somehow.

32. closing on the 12th, Chrysler shares had risen to $48.75.

Kerkorian was Chrysler’s largest shareholder,

owning 10%. Lee Iacocca, Chrysler’s former CEO who was

forced into retirement in 1992 by the board,

was backing the Kerkorian bid. The proposed $19.5 billion deal

was sketched out to include $2 billion in

Chrysler equity already held by Kerkorian and Iacocca, $3.5

billion from outside equity investors, $8.8

billion in bank debt, and $5.2 billion from Chrysler's own $7.6

billion in cash. The group planned to

suspend annual dividends, totaling $650 million a year, to help

finance the deal.

Chrysler had built up its cash balance from $3 billion to $7.6

billion from 1992 to 1994 with solid

performances in a number of divisions. CEO Robert Eaton

argued that a cash reserve of at least $7.5

billion, or $21.13 per share, should be kept as a cushion for the

next downturn in the industry. But

Kerkorian and Iacocca thought otherwise. In a news conference

shortly after the announcement, Iacocca

stated:

You just watch, it [the cash] will self-fulfill the prophecy. If

you keep saying, we

need $7.5 billion and it's just a cushion, then the union -- and I

know them like I know

my kids -- will say, 'We have a place to put that money.' They

will want part of [it]

baked into the UAW contract for three years.1

Kerkorian and Iacocca argued that Chrysler needed $2.5 billion

in cash and $2.5 billion in bank

lines of credit to survive the next recession. Alex Yemenidjian,

an executive at the Tracinda Corporation,

which was Kerkorian’s wholly owned investment vehicle,

33. summed up the position succinctly: "We

understand they want a cushion, we just believe the cushion is

too large."2

After an emergency board meeting, Chrysler issued an

announcement, saying it was "not for

sale." Eaton remarked, "We don't want to put Chrysler at risk.

We've worked hard to build this

company's financial strength, to increase shareholder value, and

to build the confidence of customers,

employees, dealers and suppliers. We have no desire to reverse

this process."3 Other observers were

less subtle about the proposal. "It's immoral," said a ranking

U.S. official with an Italian bank. "I believe

in enhancing shareholder value, but as a long-term concept

rather than a short-term grab for profits. This

could only happen in this country."4

1. As quoted in The Wall Street Journal, April 13, 1995.

2. Ibid.

3. Ibid.

4.

As quoted in The Detroit News, April 19, 1995.

This document is authorized for use only in Dr Angie

Andrikogiannopoulou's FM474M CEMS EXCHANGE at London

School of Economics and Political Science (LSE) from Dec

2019 to Jun

2020.

296-078 The Chrysler Takeover Attempt

34. 2

Company Background

Chrysler was incorporated in 1925 by Walter Percy Chrysler, a

former vice president of General

Motors (GM). Resigning from GM over policy differences,

Chrysler rescued the Maxwell Motor

Corporation from insolvency and designed its new Chrysler

automobile. First exhibited in 1924, the car

was an immediate success and before year's end, the company

had sold 32,000 cars and had earned more

than $4 million. By 1940, Chrysler had acquired Dodge and

Plymouth, controlled 25% of the domestic

market, and surpassed Ford to become the second largest

automaker in the industry behind GM.

Although it lost ground to Ford and GM in the ensuing decades,

Chrysler was still third among U.S. and

worldwide automakers by the end of the 1960s. But the 1970s

were not good to Chrysler, as the oil

shocks, inflation in the economy, and increased Japanese

competition all took their toll on the company.5

The Iacocca Years In 1974 losses totaled a massive $52 million,

and the next year's deficit was

five times that amount. After a brief respite in 1976 and 1977,

Chrysler incurred net losses of $205 million

in 1978 and $1.1 billion in 1979. In just one year, Chrysler’s

worldwide sales of motor vehicles fell by 1.6

million units.6 It took a complex set of negotiations with

creditors and unions as well as a $1.5 billion

government bailout to save Chrysler from bankruptcy in 1978.

Lee Iacocca, the charismatic CEO who

was hired shortly after being fired from the presidency of Ford,

presided over Chrysler's comeback with

35. a flair for communications and salesmanship. By 1981,

Chrysler was on its way back. Its fleet had

achieved the best corporate average fuel economy in the

industry at 25.5 miles per gallon, and its Aries

and Reliant models had both received the prestigious “Motor

Trend Car the Year” award. By 1983,

Chrysler had achieved the largest percentage increase in U.S.

retail sales of any major domestic car maker

(19% for cars and 11% for trucks). Earnings were positive

again in 1983 and the company repaid the

government loan seven years early.7

After its recovery in the early 1980's, Chrysler diversified. It

acquired Gulfstream Aerospace,

Finance America, and E.F. Hutton Credit Corporation, among

others. It also merged with American

Motors Corporation, acquired the Italian automaker

Lamborghini, and established several joint-ventures

with Mitsubishi and Samsung. But at the end of 1989, Chrysler

announced that it was scrapping its

holding-company structure (which was created just four years

earlier) to cut costs. Soon thereafter, it

announced it would try to sell Gulfstream and Electrospace

Systems, marking a humiliating end to the

company's diversification strategy.8

In 1991 Chrysler lost $759 million, its debt was junk rated, and

its pension plans were

underfunded by more than $4 billion. Domestically, Chrysler

was selling only one in twelve cars, as

opposed to one in every nine cars five years earlier. Critics

argued that Chrysler’s financial problems

were a direct result of failing to invest in new product

development in the mid 1980s.9 But by 1992, new

models were ready, and hopes were high for another recovery.

Fortunately, sales of the higher-margin

36. minivans (a product Chrysler virtually invented in 1984) were

strong, and its other new models were

earning good reviews. They were the low priced Dodge Shadow

and Plymouth Sundance; the high

performance Dodge Stealth; the Dodge Spirit and Plymouth

Acclaim sedans; and the Jeep Grand

Cherokee and Dodge Dakota V-8 trucks. Despite all this, the

board thought it was time for new

leadership. In 1992 they chose Robert Eaton, head of European

operations at GM, to replace Iacocca.

Eaton Takes Over Eaton's focus from the start was on

transforming Chrysler into a company

that could withstand downturns. Shortly after becoming

chairman, he told company managers, "My

5. International Directory of Company Histories, Volume 1.

6. Chrysler Annual Report, 1980.

7. For further information, see “Chrysler: Iacocca's Legacy,”

Harvard Business School Case No. 493-017.

8. Ingrassia, Paul, and White, Joseph B., Comeback, The Fall

and Rise of the American Automobile Industry. New York:

Simon & Schuster, 1994, p. 195.

9. Frank Washington, "LH, as in 'Last Hope'," Newsweek, June

29, 1992 as quoted in HBS case No. 493-017.

This document is authorized for use only in Dr Angie

Andrikogiannopoulou's FM474M CEMS EXCHANGE at London

School of Economics and Political Science (LSE) from Dec

2019 to Jun

2020.

37. The Chrysler Takeover Attempt 296-078

3

personal ambition is to be the first chairman to never lead a

Chrysler comeback."10 The early results were

good as the stock price soared in 1992 and 1993 on the heels of

the economic recovery. New product

development was accelerated even more, and good reviews came

out for the LH sedans, the Dodge

Neon, and the midsize Cirrus and Stratus models. Chrysler also

continued to dominate the minivan

segment. In one of Eaton’s first major product moves, the

company invested $2.6 billion on a complete

redesign of the minivan line -- more than any new-vehicle

development program in company history.

But as interest rates began to climb and the stock price

remained flat, Chrysler was forced to take

steps to mollify Kerkorian, who was the largest shareholder at

9%. Management boosted its dividend by

60%, announced a $1 billion share buyback, and diluted its

poison pill so that individual investors could

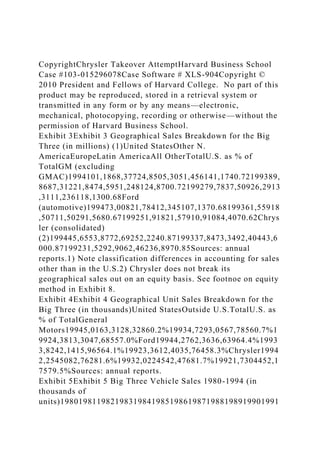

raise their stakes to 15%. Nevertheless, the share price

continued to fall. Between mid-December and the

April 12 Kerkorian bid, Chrysler’s stock price fell 16% -- a

drop of one-third from its peak of $53 in

January, 1994 (see Exhibit 2).11

The Tracinda Group

The 77-year-old Kerkorian was the son of poor Armenian

farmers from Fresno, California. He

made his first millions running commercial and military flights

during the 1950s and 1960s, many of

them between Los Angeles and Las Vegas. He bought and sold

38. properties in Las Vegas and eventually

pioneered the notion of building huge hotels and attracting

people who had never gambled before.

Enticing people to "play where they stay" was a new idea which

proved extremely successful.12 Another

large part of his estimated $2.5 billion net worth came from

timely acquisitions and disposals of

Hollywood studios, among them Columbia Pictures and

MGM/UA.

Kerkorian owned all of the Tracinda Corporation, which was

the holding company for his

Chrysler stock. He began purchasing Chrysler in 1990 in the

middle of the recession for $12.37 per share.

By 1995, he had spent about $676 million accumulating his

stake. At the closing market price of $48.75

the day of the announcement, Kerkorian’s 36 million shares

were worth nearly $1.8 billion.

Many analysts wondered whether Kerkorian was serious about

his intent to buy control of

Chrysler. Ownership of a heavy manufacturing entity was not

characteristic of his long investment

history.13 For his part, Iacocca, 70, stated that he would serve

only as an advisor to Chrysler if the deal

went through, saying, "after 47 years in Detroit, I don't want to

go back."14 But others were more

suspicious of his motives. One reporter commented: "It's

impossible to believe Mr. Iacocca's current

protestations that he doesn't want to run Chrysler again. He

never wanted to stop running it, and at the

very least a Kerkorian victory would leave him in charge of all

the major strategic decisions at the

company."15

The Auto Industry Cycle

39. Supply In the volatile auto industry, car companies can quickly

shift from making a lot of money

to posting big losses when sales drop. One reason for this is

that traditionally, auto companies built

enough production capacity to supply everyone who wanted a

car in a boom year. This maximized

profits in boom years but led to excess inventory problems in

bad years. Also, in good times they

received payments for cars as soon as they were assembled, and

did not have to pay parts suppliers for

10. As quoted in The Wall Street Journal, April 14, 1995.

11. The Economist Newspaper, April 15, 1995.

12. The Washington Post, April 14, 1995.

13. Los Angeles Times, April 14, 1995.

14. As quoted in The Wall Street Journal, April 13, 1995.

15. Paul Ingrassia, "What's Driving the Chrysler Deal," The

Wall Street Journal, April 19, 1995.

This document is authorized for use only in Dr Angie

Andrikogiannopoulou's FM474M CEMS EXCHANGE at London

School of Economics and Political Science (LSE) from Dec

2019 to Jun

2020.

296-078 The Chrysler Takeover Attempt

4

up to 45 days. When sales sagged, however, auto makers ended

up paying for parts before the cars were

sold, straining cash reserves.16

40. To cover their high fixed costs when sales were flat, auto

makers cut their prices to move existing

inventory. These cuts, typically in the form of rebates and

dealer incentives, often escalated into

industry "incentive wars." Thus earnings would be more

variable than actual vehicle sales. For example,

from 1989 to 1990, Chrysler’s vehicle sales fell 16.8% from

2.38 to 1.98 million units. In that same period,

pretax income fell 74%, from $565 million to $147 million.

Likewise, when vehicle sales increased 11.5%

from 1993 to 1994, pretax income rose 51.9% in the same

period.

Demand Interest rates had a large impact on demand. As with

most companies, higher rates

increased the cost of capital and squeezed margins. But with

auto manufacturers, rising rates also had a

dramatic impact on consumer demand because buyers who

financed their auto purchases would have

higher monthly payments. Federal Reserve interest rate policy

was thus a key variable affecting the auto

cycle. Other key demand indicators were employment, real

income growth, the underlying age

composition of the motor vehicle fleet, and the strength of the

dollar relative to the currencies of Japan

and Europe.

The consensus among analysts in early 1995 was that new

vehicle sales would be sluggish

because of the recent Federal Reserve rate hikes and an overall

slowing of the economy. Some believed

that the auto cycle had already peaked, predicting that 1994

volumes would be very difficult to match. A

downturn was inevitable, they argued, and it was more likely to

come sooner rather than later. But

41. others believed that slower demand growth (rather than an

actual decline in demand) would lead to a

longer, flatter cycle for the auto companies. In this scenario,

Chrysler’s sales volumes would be

maintained by the pent-up demand still lingering from the last

recession.

Chrysler's Cash

When the 1989-1991 recession ended, management established

the goal of building up $5 billion

in cash to weather the next downturn. But when revenues

increased, Chrysler raised the target to $7.5

billion. As one official put it, "$7.5 billion would be prudent.

If you run the company with less cash, you

run a greater risk of having to cut product spending and pension

funding in the next downturn."17 But

in 1995 Chrysler’s pension was fully funded for the first time in

almost 40 years, and its credit rating had

just been upgraded to single-A by the major credit agencies.

Company plans called for an aggressive capital expenditure

program, projected to cost $3.2

billion in 1995 and $3.1 billion annually thereafter. Other

projected cash outlays included the $1 billion

stock buyback in 1995 (subject to “market conditions”), and

increasing the dividend payment from $1.00

to $1.60 per common share, adding about $200 million to the

annual cash outlay for dividends. In

addition, Chrysler’s stated goal was to lower its debt-to-capital

ratio from 18% to 10%. This would cost

approximately $1 billion, although the timing of the debt pay-

down was unknown.

On the product side, Chrysler was aggressively rolling out its

new models and predicting that

42. profit margins would improve as the product mix changed. But

some external factors were creating

uncertainty. Inventories for the Neon and the LH full-size

sedans were running above normal in the first

quarter. For the minivans, Chrysler was projecting the loss of

approximately 65,000 units during the

model changeover. Also, Ford was building its inventories to

uncomfortable levels, and all

manufacturers were adding capacity to the sport utility line

which included Chrysler’s high-margin

Grand Cherokee. The concern was that this could lead to price

cutting, followed by reduced margins.

16. The Wall Street Journal, April 17, 1995.

17. As quoted in The Wall Street Journal, April 17, 1995.

This document is authorized for use only in Dr Angie

Andrikogiannopoulou's FM474M CEMS EXCHANGE at London

School of Economics and Political Science (LSE) from Dec

2019 to Jun

2020.

The Chrysler Takeover Attempt 296-078

5

Finally, the crisis in Mexico was depressing sales there and

creating some uncertainty about the market

for the T300 pickup and the Cirrus/Stratus lines which were

manufactured in Mexico.

Deal Structure and Financing

43. For Tracinda, the structure of the deal would have an impact on

two key issues related to

Chrysler's cash position. First, the amount of cash they were

going to use from the company's balance

sheet would directly affect its ability to weather a future

downturn. Second, the deal structure itself

could have cash flow implications depending on the amount and

type of leverage used for the buyout.

Using $5.2 billion of Chrysler cash to finance the deal would

leave approximately $2.4 billion on

the balance sheet. Depending on projections of additional cash

build-up in the short term, Chrysler

would have anywhere from $2.5 billion to $4 billion to weather

the next downturn. As for the cash flow

implications of adding $8.8 billion of leverage, it appeared that

the after-tax cost of the additional interest

would be almost offset by the elimination of dividends.

Chrysler's finance subsidiary might also be available to support

some of the leverage in the deal.

Chrysler Financial (CFC) was a well-managed company with

earning assets to equity of roughly 4.5

times. This was much lower than GMAC (GM's finance unit)

which was at 9.0 times, and Ford Financial

Services which was at 9.6 times. Increasing leverage at

Chrysler Financial might provide an additional $2

billion in capital for the deal.

At the time of the announcement, Kerkorian had not yet

obtained financing for the deal. A

Tracinda spokesperson cited the need for secrecy as the reason

no banks had been contacted. But there

was some uncertainty about whether it could be raised at all.

One reason was that more than 150 banks -

- ranging from small local lenders to some of the world's

44. biggest banks -- were already tied up in

Chrysler credit agreements.

Reactions

As both sides in the deal stepped up the rhetoric on the

proposed takeover, Chrysler's analysts

remained mixed in their opinions. Summarizing the pro-

management stance, one analyst observed: "It's

really uncertainty in the economy that drove the stock down and

put Chrysler in play. And that is

completely out of Chrysler's control."18 These analysts were

convinced Chrysler represented a great

buying opportunity, with an inherent value in the range of $70

to $90 per share. David Cole, Director of

the Office for the Study of Automotive Transportation, was

even more bullish: “Wall Street has

undervalued the [auto] industry,” he said, placing the value of

Chrysler at $100 per share.19 But others

suggested that the large cash hoard and weak stock price were

signs that Chrysler wasn't handling its

finances properly. "The market is the ultimate arbiter on how

Chrysler is being run, and the market is

saying it's sorely mismanaged."20

Public reaction to the Tracinda group was mostly negative, as

many were calling the deal a

flashback to the excesses of the 1980s. The Tracinda team was

unmoved. Yemenidjian summarized the

group’s attitude: "We are the owners of the company. We are

not some outside intruders who came in to

spoil the company. The lack of respect is abominable."21

18. John Casesa of Wertheim Schroder, as quoted in The Wall

45. Street Journal, April 14, 1995.

19. As quoted in William J. Cook and Linda Grant, U.S. News

& World Report, April 24, 1995.

20. Analyst Nicholas Lobacarro of S.G. Warburg & Co., as

quoted in The Wall Street Journal, April 17, 1995.

21. As quoted in USA Today, April 27, 1995.

This document is authorized for use only in Dr Angie

Andrikogiannopoulou's FM474M CEMS EXCHANGE at London

School of Economics and Political Science (LSE) from Dec

2019 to Jun

2020.

296-078 The Chrysler Takeover Attempt

6

Exhibit 1 Chryslerís Board of Directors

Name Age Occupation Director Since

Lilyan H. Affinitok 63 Former Vice Chairman, Maxxam Group

1982

Robert E. Allen 60 Chairman and CEO, AT&T 1994

Joseph E. Antoninik 53 Former President and CEO, Kmart Corp.

1989

Joseph A. Califano, JR. k 63 Secretary of Health, Education,

and Welfare (1977-79) 1981

Thomas G. Denomme 55 Chrysler Vice Chairman 1993

Robert J. Eaton 55 Chrysler Chairman and CEO 1992

Earl G. Graves 60 Chairman and CEO, Earl G. Graves Ltd. 1990

Kent Kresa 57 Chairman and CEO, Northrop Grumman 1989

Robert J. Lanigan* 66 Chairman Emeritus, Owens-Illinois 1984

Robert A. Lutz 63 Chrysler President and Chief Operating

Officer 1986

46. Peter A. Magowan* 52 Chairman, Safeway 1986

Malcolm T. Stamper 69 Former Vice Chairman, Boeing 1984

Lynton R. Wilson 54 President and CEO, BCE Inc. 1984

kAlso a director of Kmart Corp.

*Both Lanigan and Magowan headed companies that were

acquired in leveraged buyouts by KKR.

Source: annual report.

Exhibit 2 Big Three Closing Stock Prices and the S&P 500

Index, 1/3/95 to 4/12/95 (1/3/95 = 100)

77.00

79.00

81.00

83.00

85.00

87.00

89.00

91.00

93.00

95.00

97.00

99.00

101.00

103.00

105.00

107.00

109.00

111.00

1/

3/

51. The Chrysler Takeover Attempt 296-078

7

Exhibit 3 Geographical Sales Breakdown for the Big Three (in

millions) (1)

United Other Latin U.S. as %

States N. America Europe America All Other Total of Total

GM (excluding GMAC)

1994 101,186 8,377 24,850 5,305 1,456 141,174 0.72

1993 89,868 7,312 21,847 4,595 1,248 124,870 0.72

1992 79,783 7,509 26,291 3,311 1,236 118,130 0.68

Ford (automotive)

1994 73,008 21,784 12,345 107,137 0.68

1993 61,559 18,507 11,502 91,568 0.67

1992 51,918 21,579 10,910 84,407 0.62

Chrysler (consolidated) (2)

1994 45,655 3,877 2,692 52,224 0.87

1993 37,847 3,349 2,404 43,600 0.87

1992 31,529 2,906 2,462 36,897 0.85