Downloaded 14 times

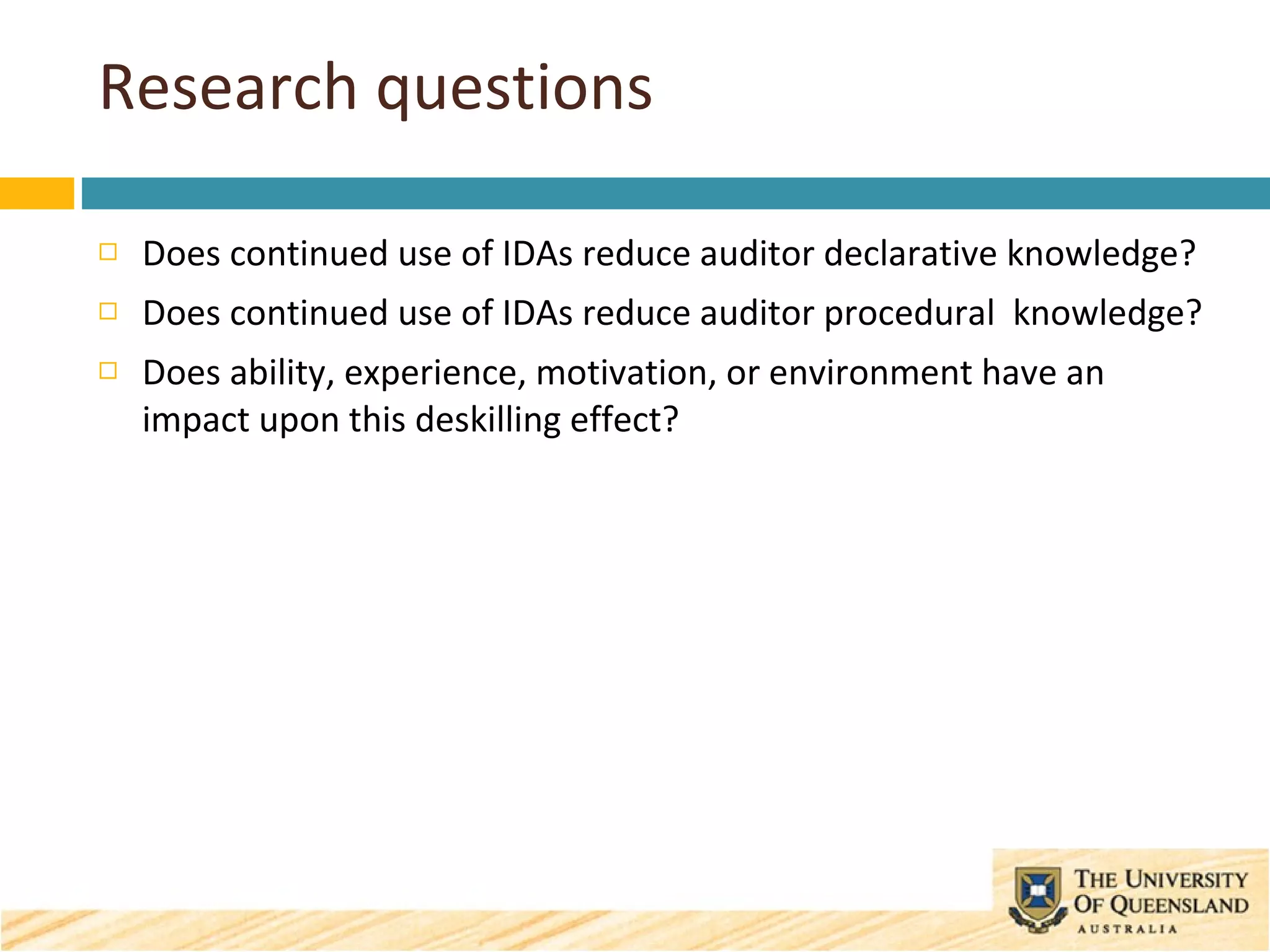

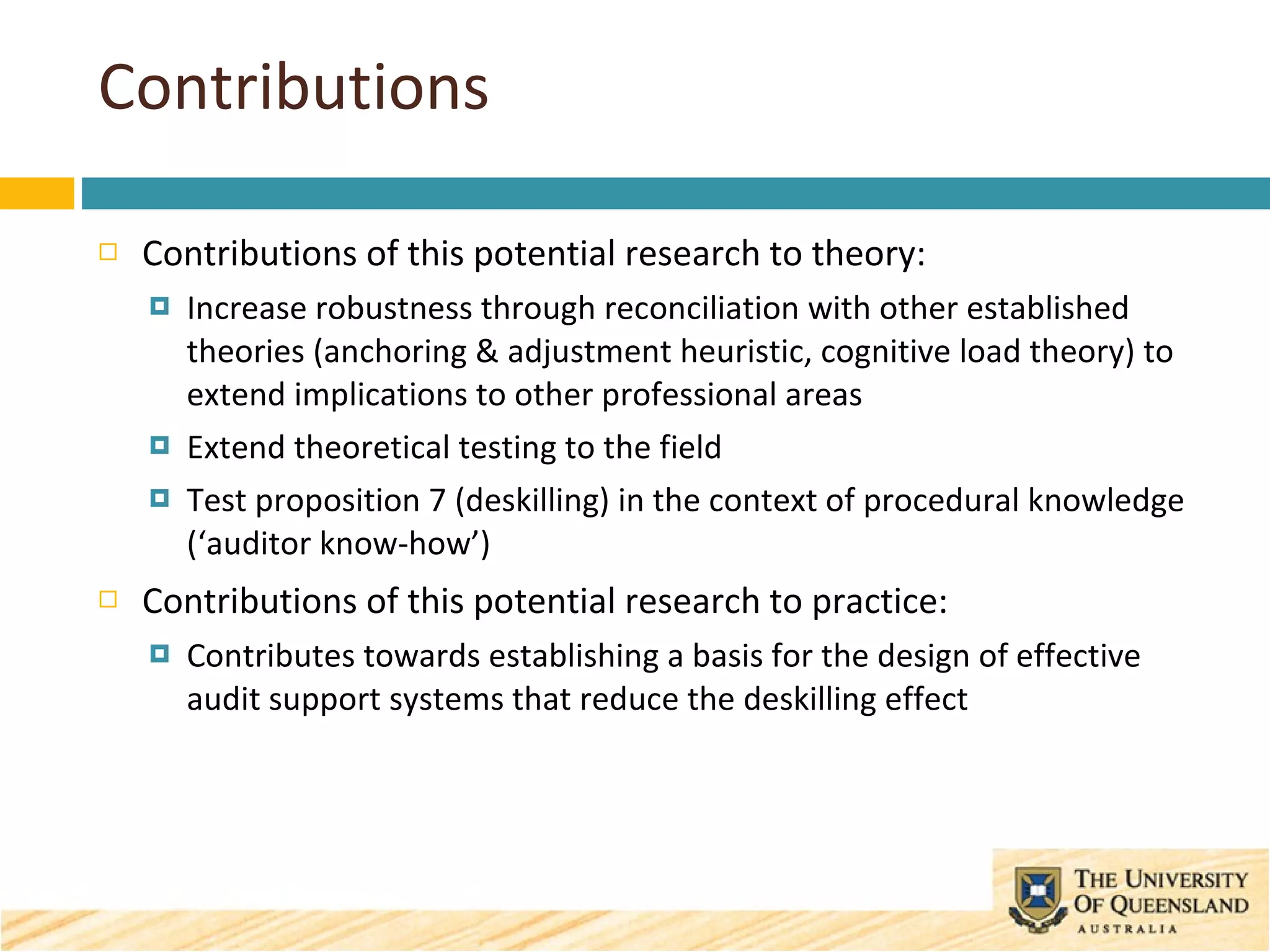

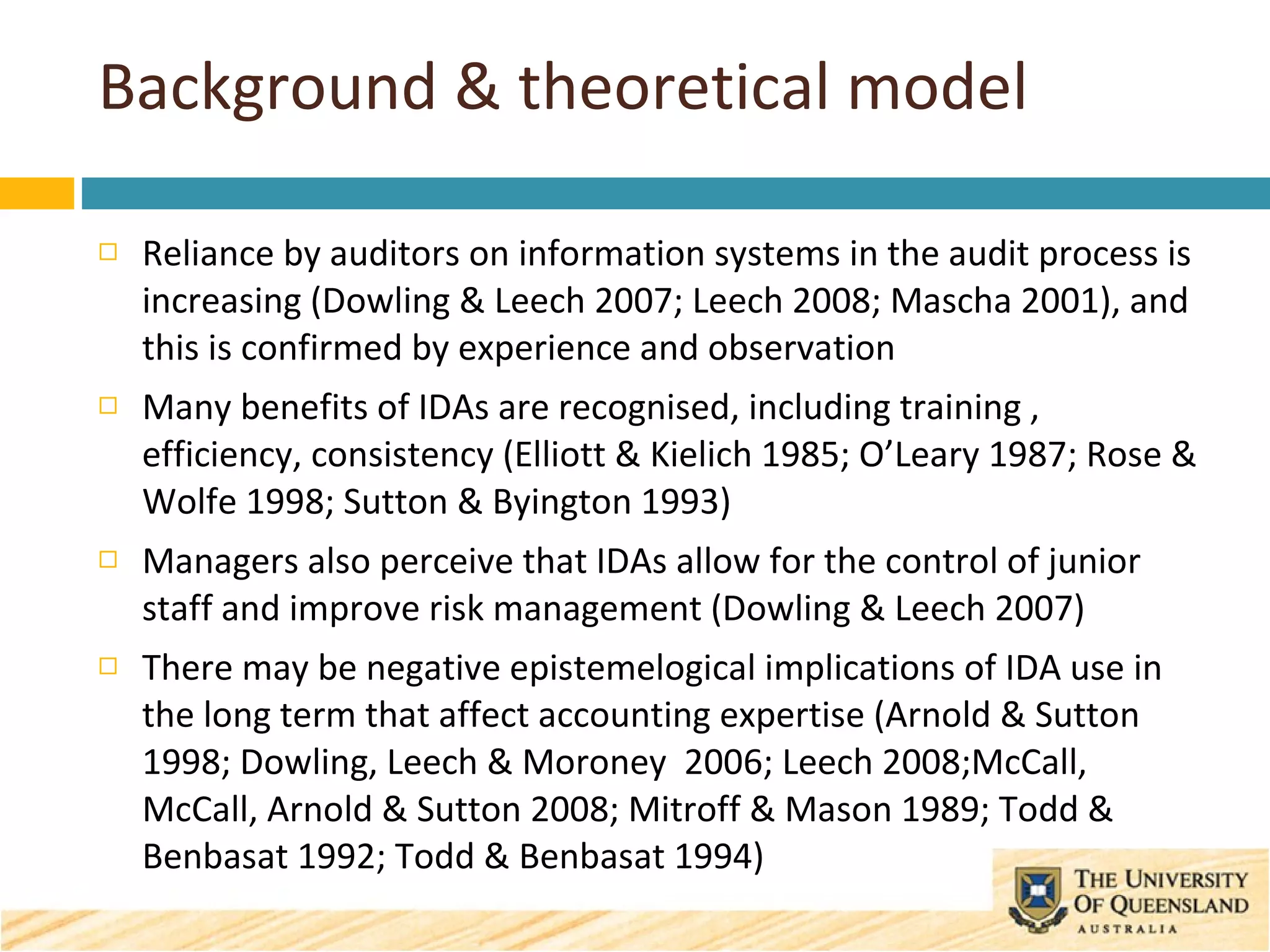

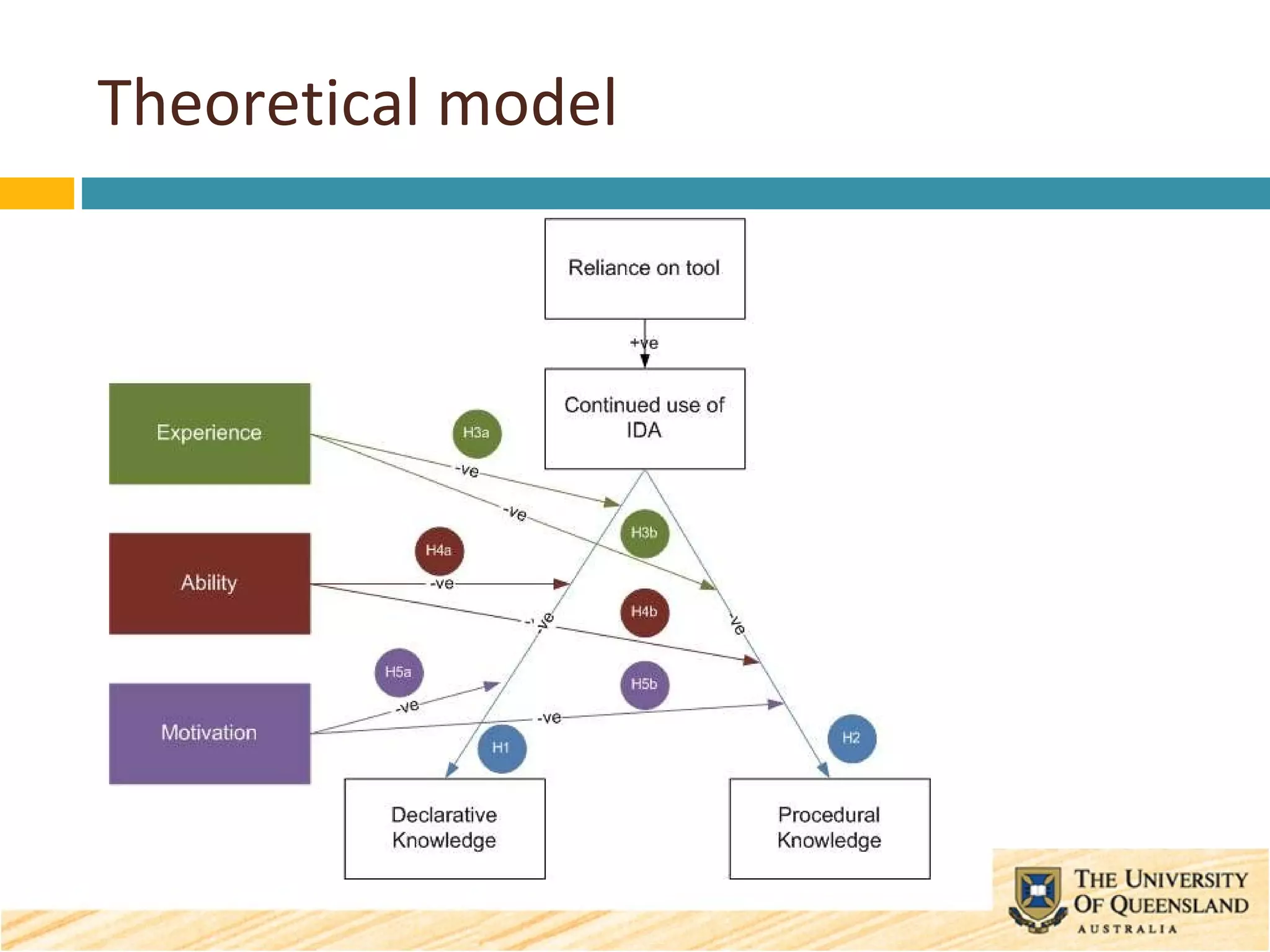

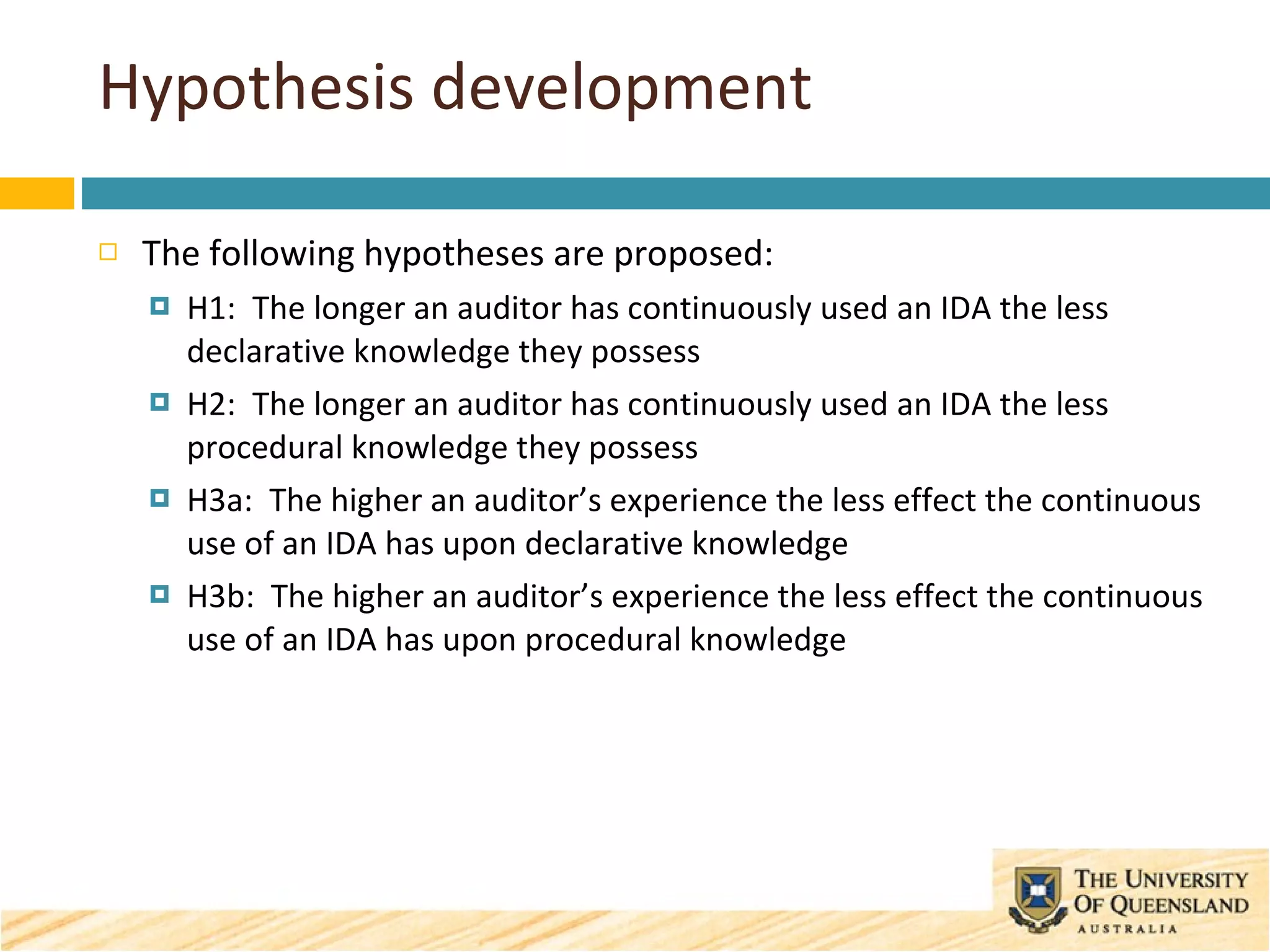

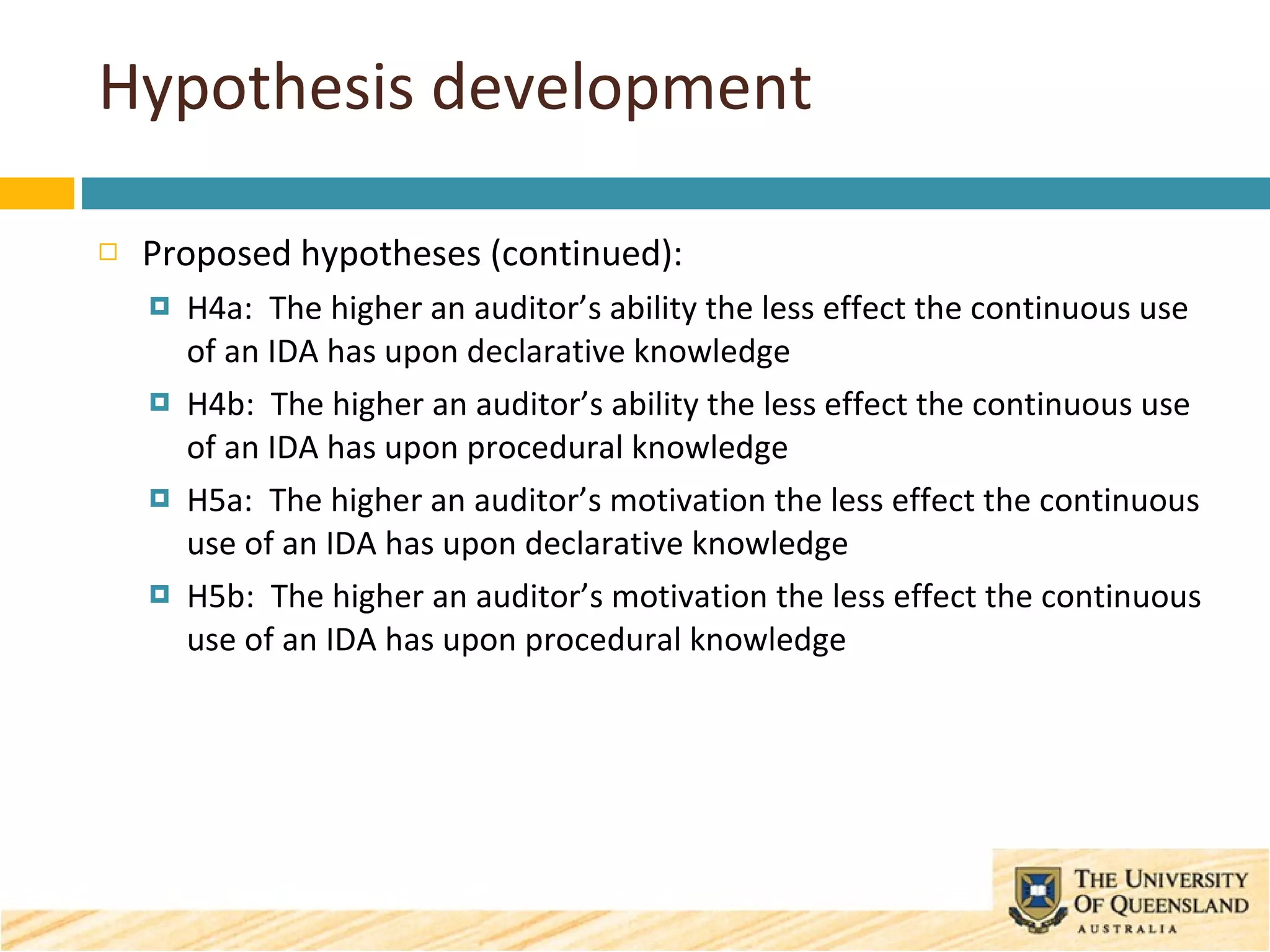

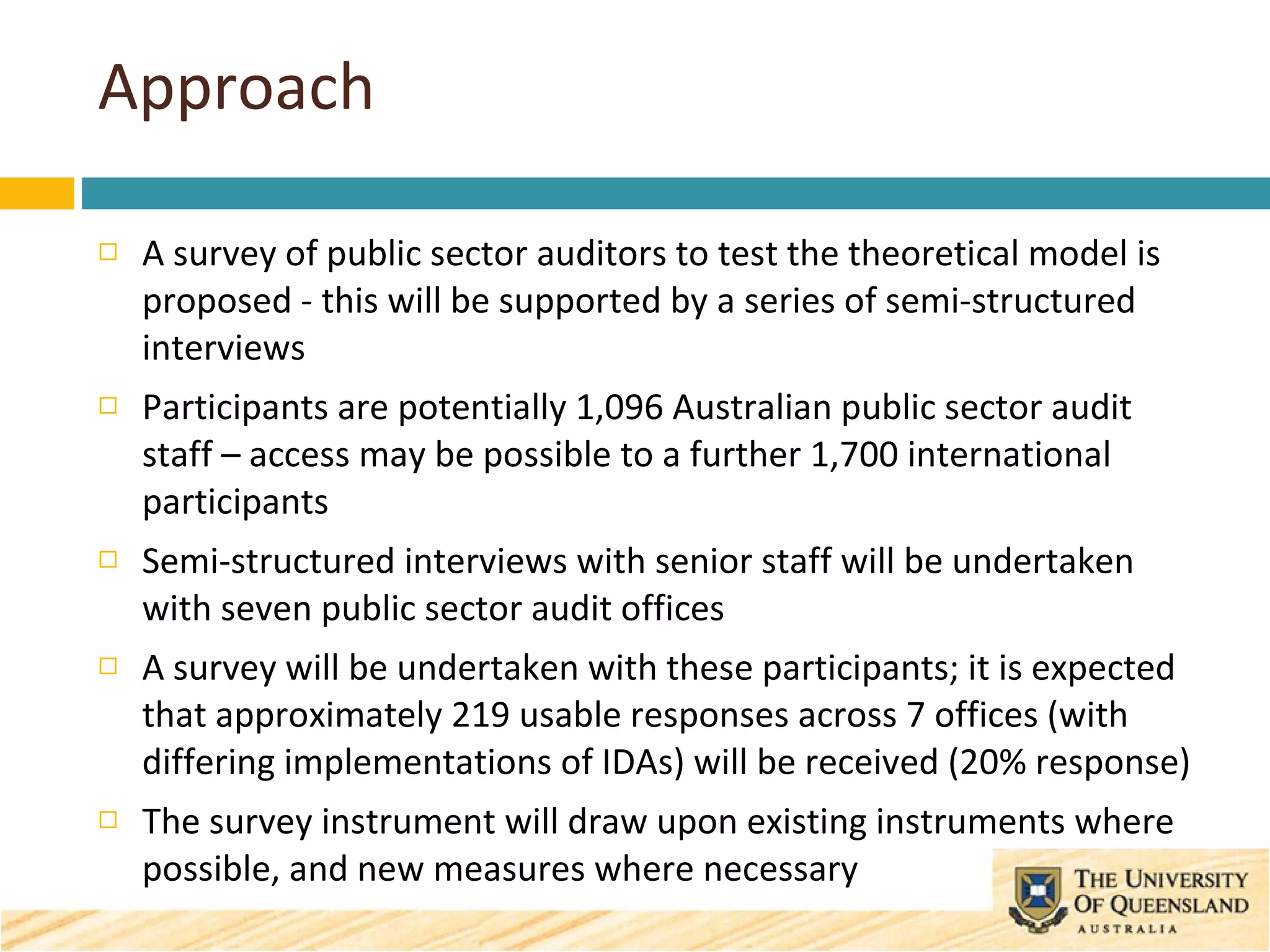

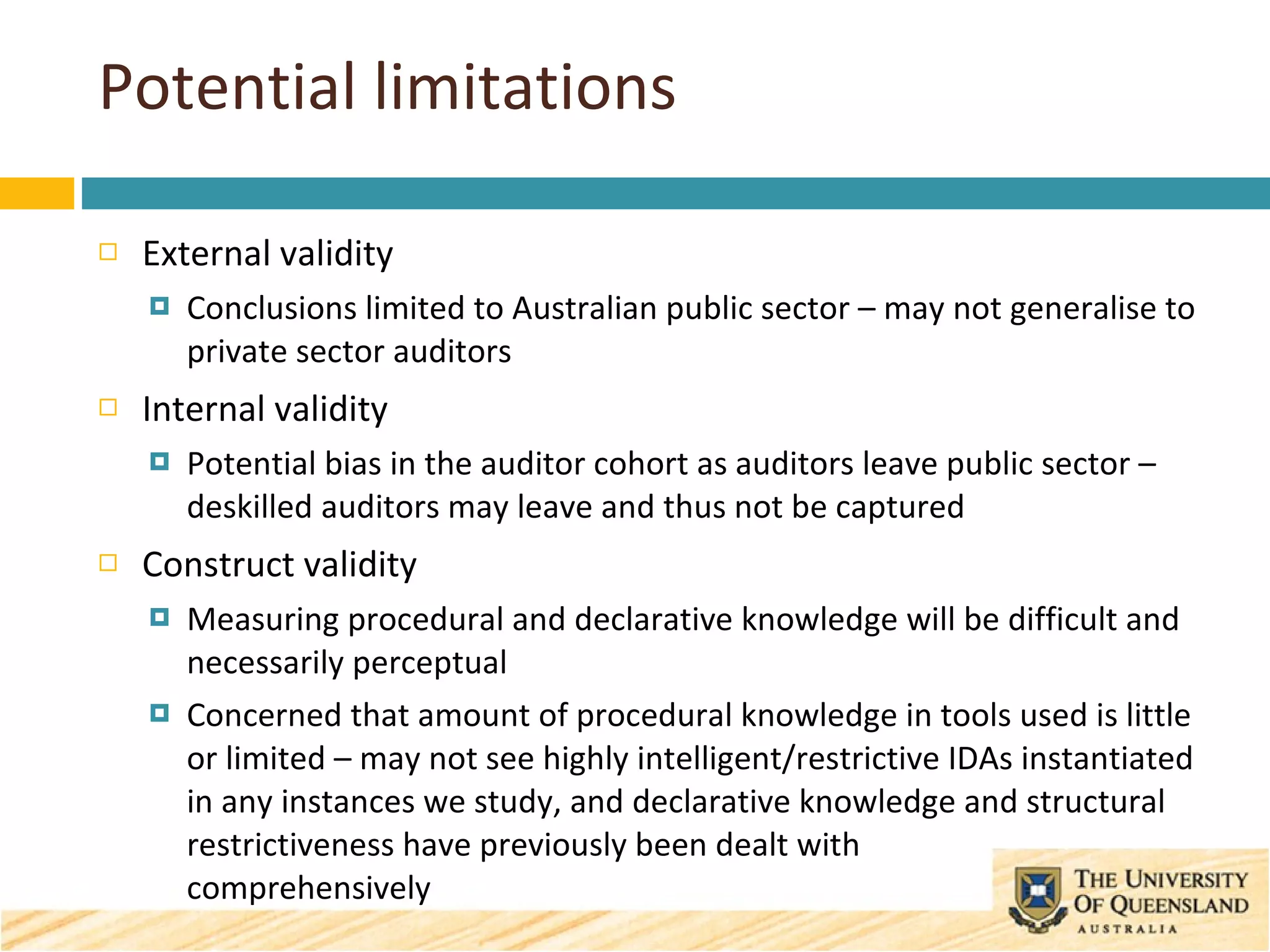

This document discusses the impact of using intelligent decision aids (IDAs) on auditors' procedural and declarative knowledge, addressing potential deskilling effects due to reliance on technology in auditing practices. It proposes research questions and hypotheses related to the relationship between IDA usage and auditors' knowledge retention, while also outlining a proposed methodology for testing these hypotheses through surveys and interviews. The findings aim to contribute to both theoretical understanding of technology dominance in decision-making and practical applications for designing effective audit support systems.