Download to read offline

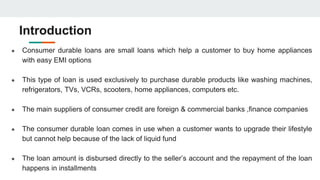

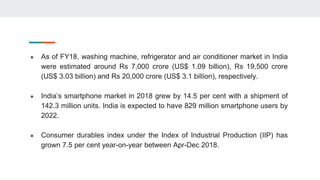

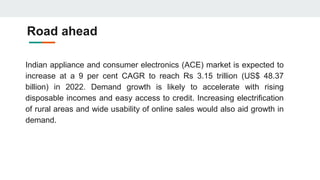

The document discusses consumer durable loans, which facilitate the purchase of home appliances through manageable EMI options, typically requiring a down payment of 20-25% and a repayment period of 12-60 months. It highlights key aspects like credit screening procedures, revenue models involving various fees and charges, and the growth prospects of India's consumer electronics market, driven by rising disposable incomes and a favorable demographic trend. The market for appliances is projected to grow significantly, with increased access to credit and widening online sales contributing to this expansion.