Downloaded 11 times

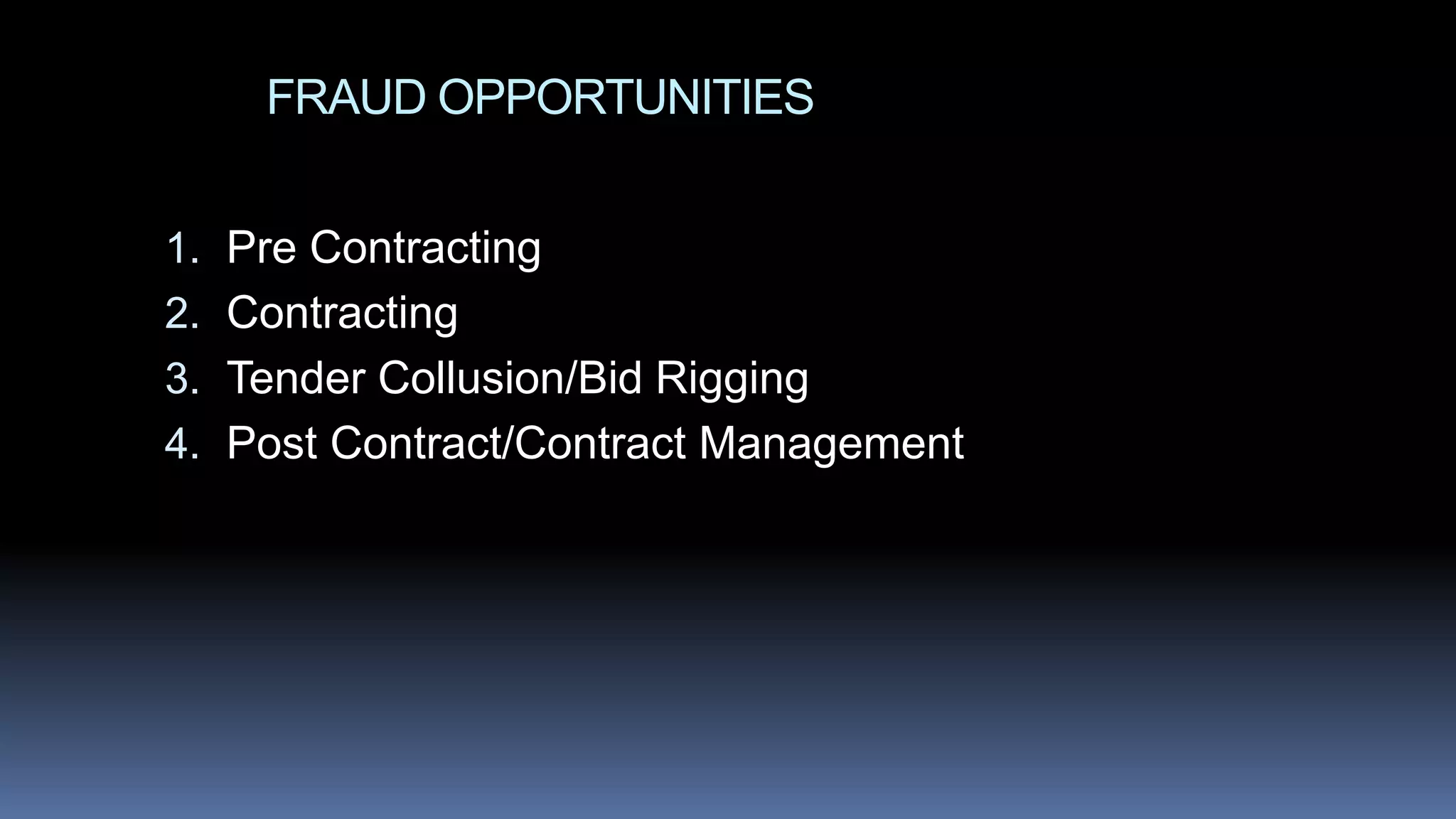

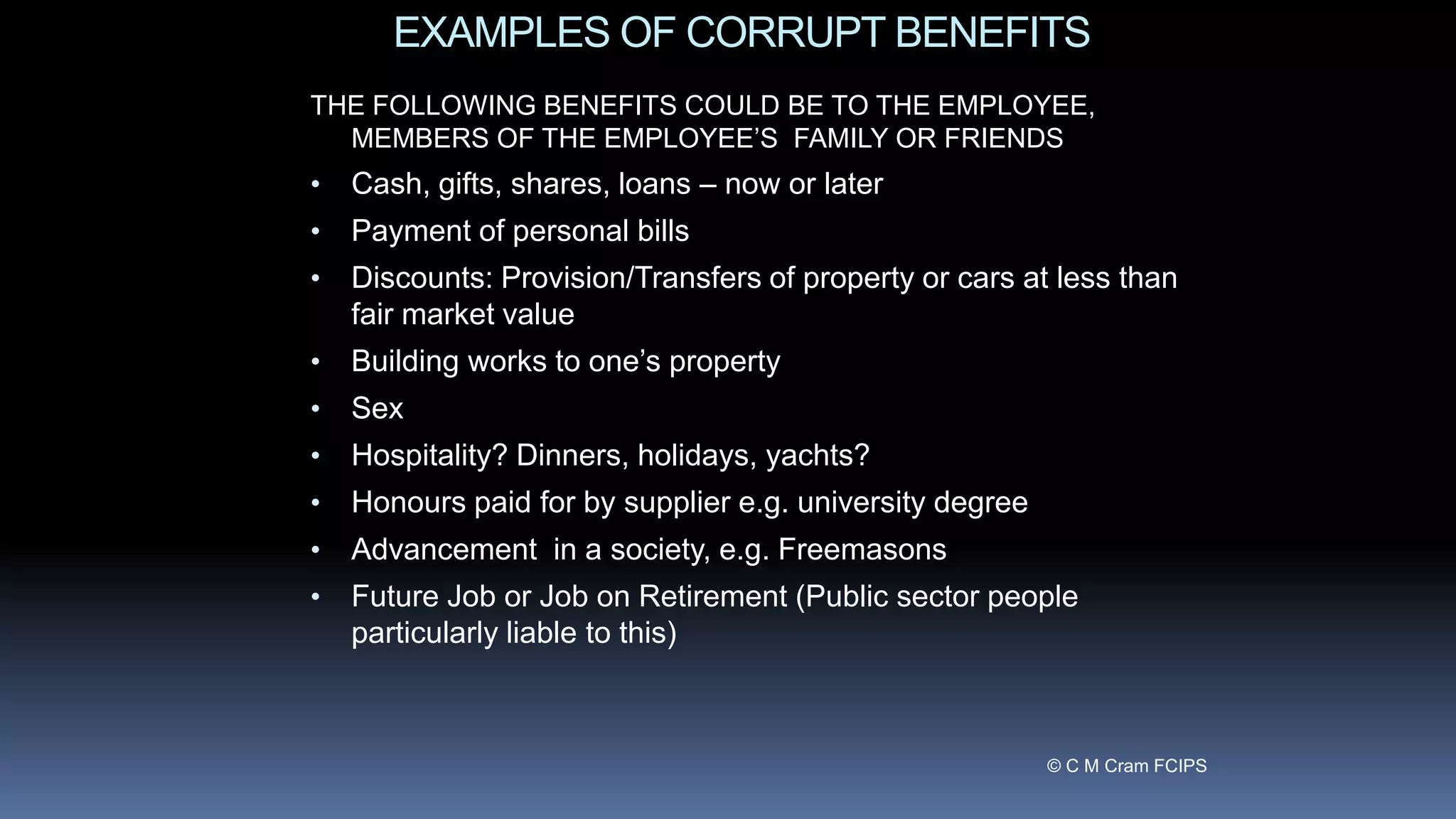

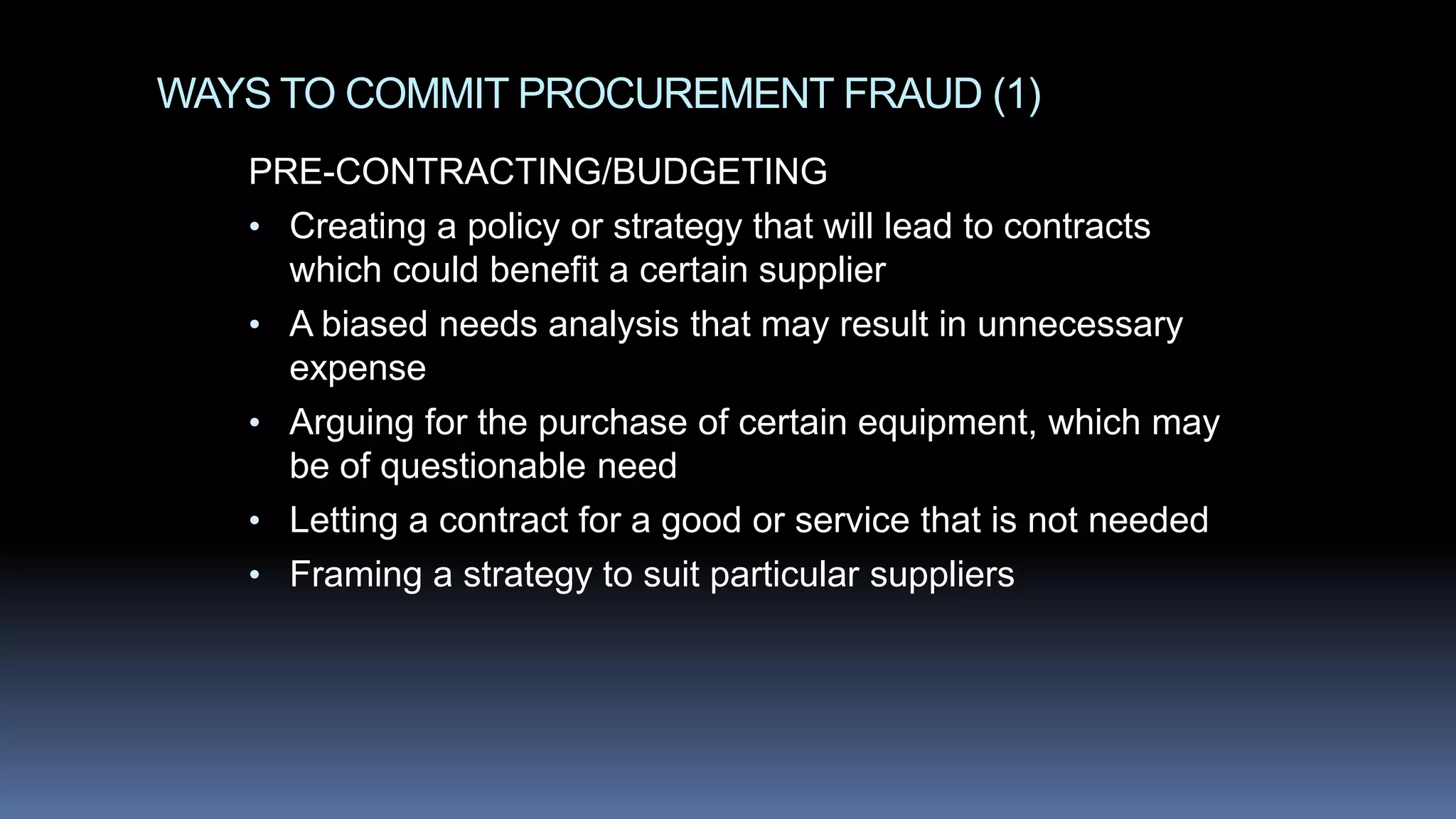

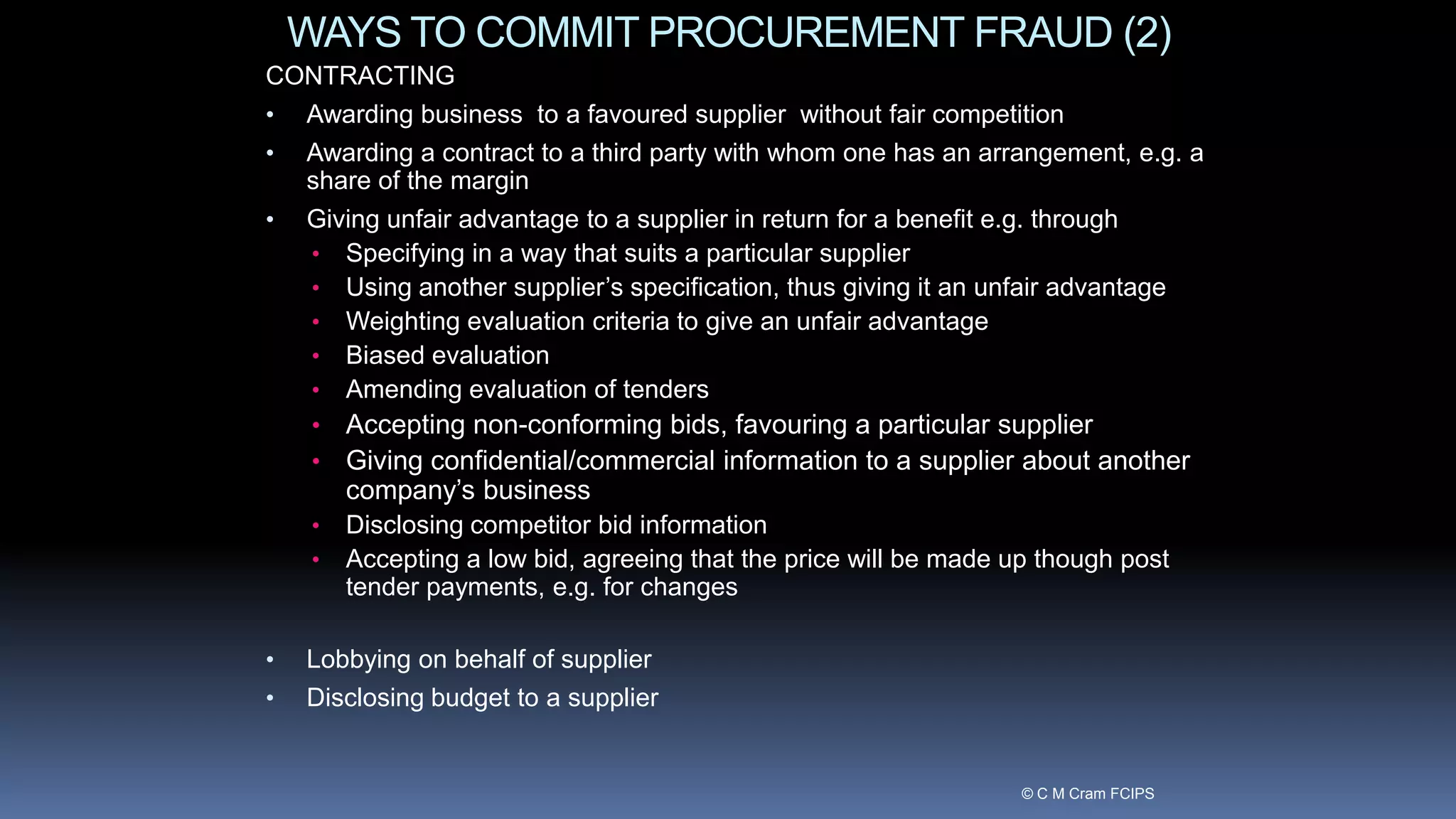

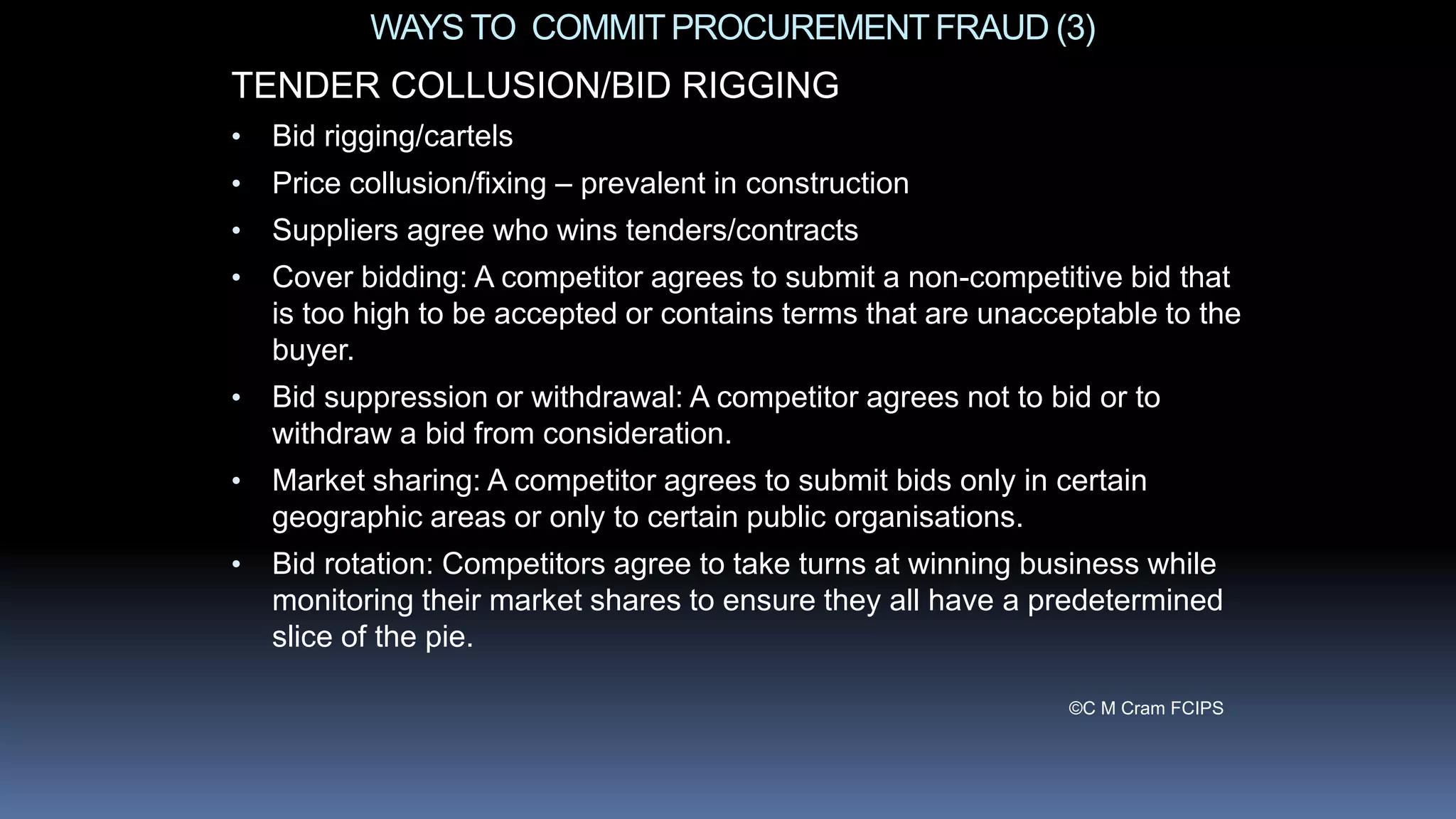

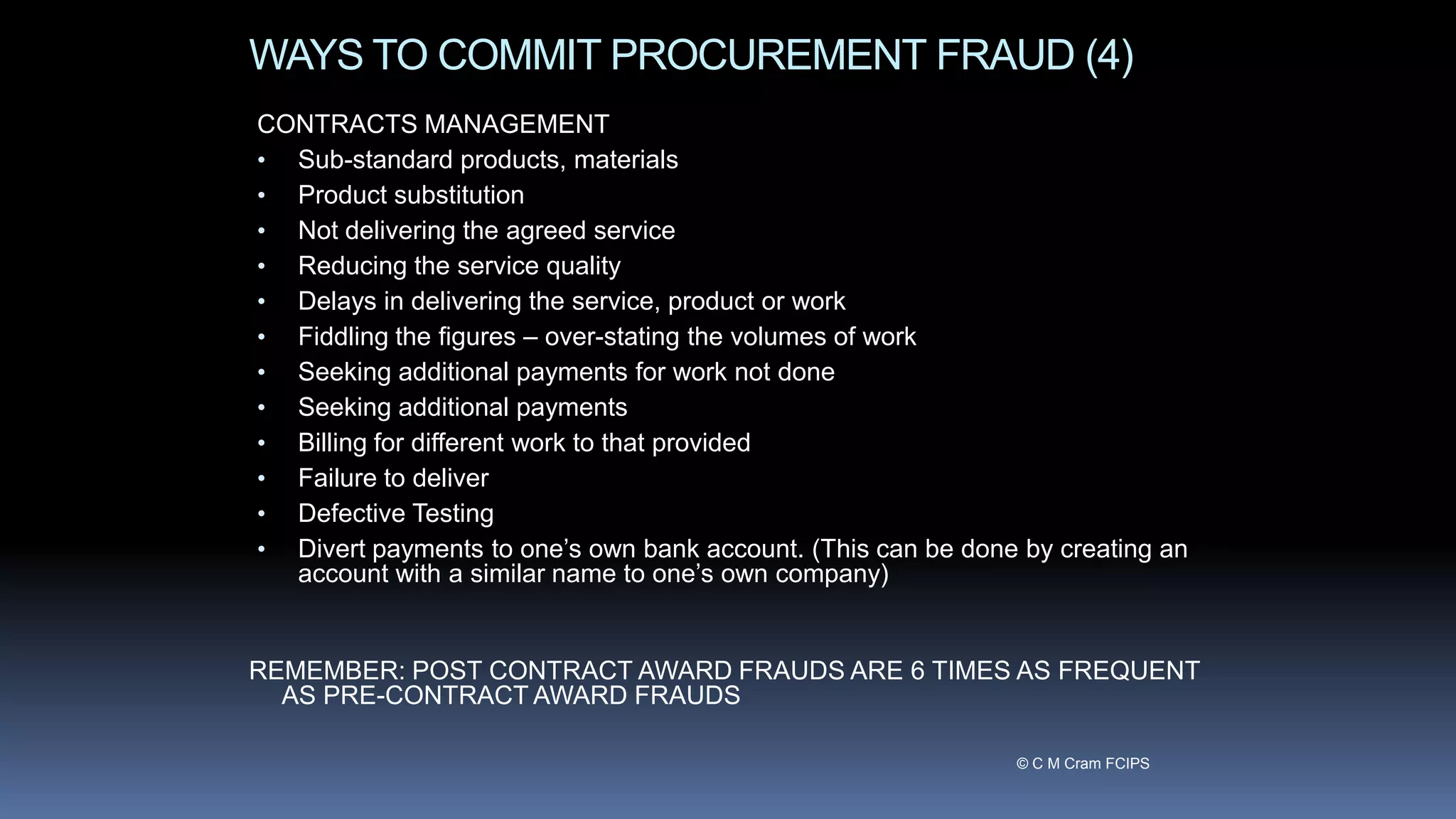

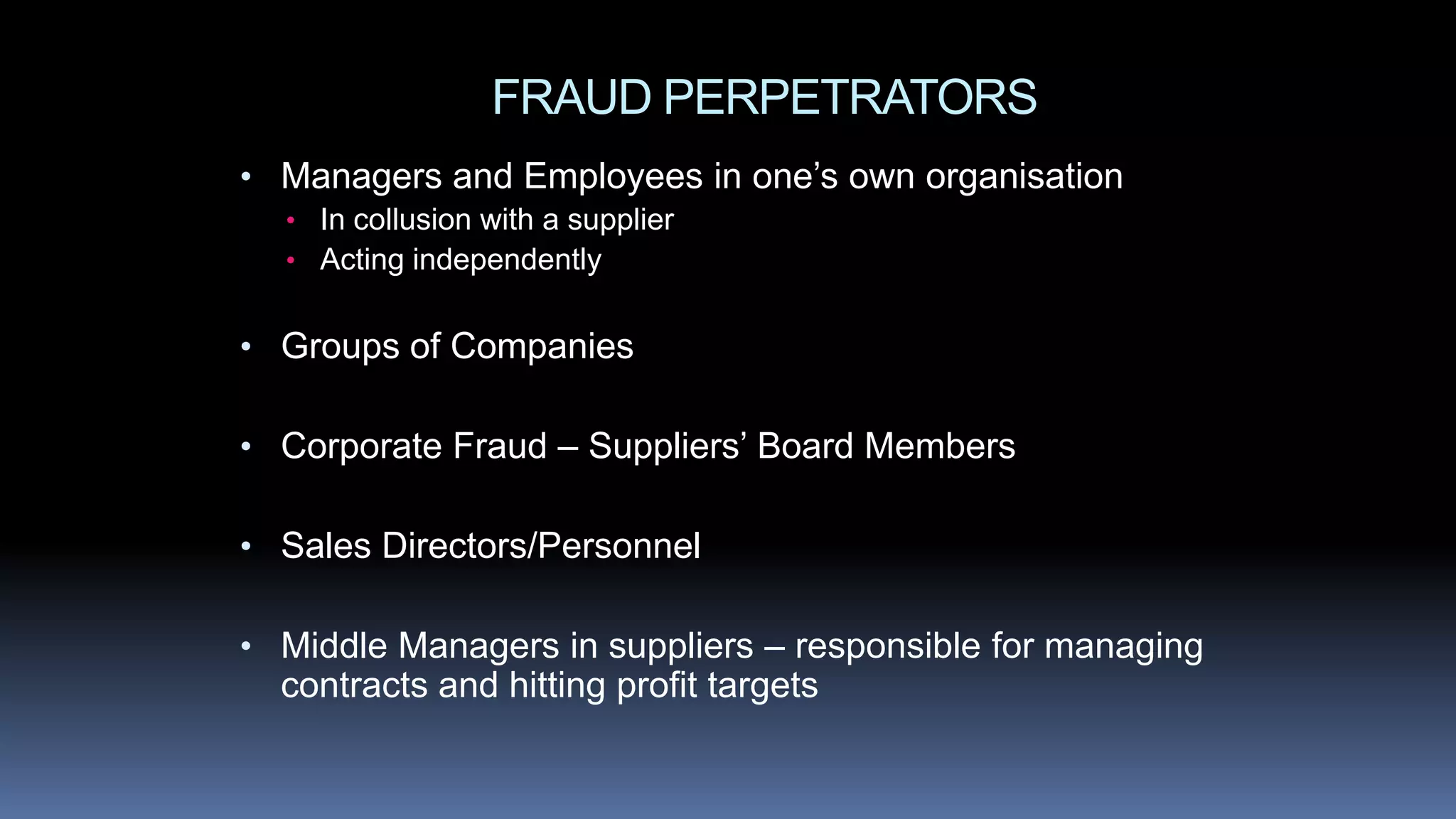

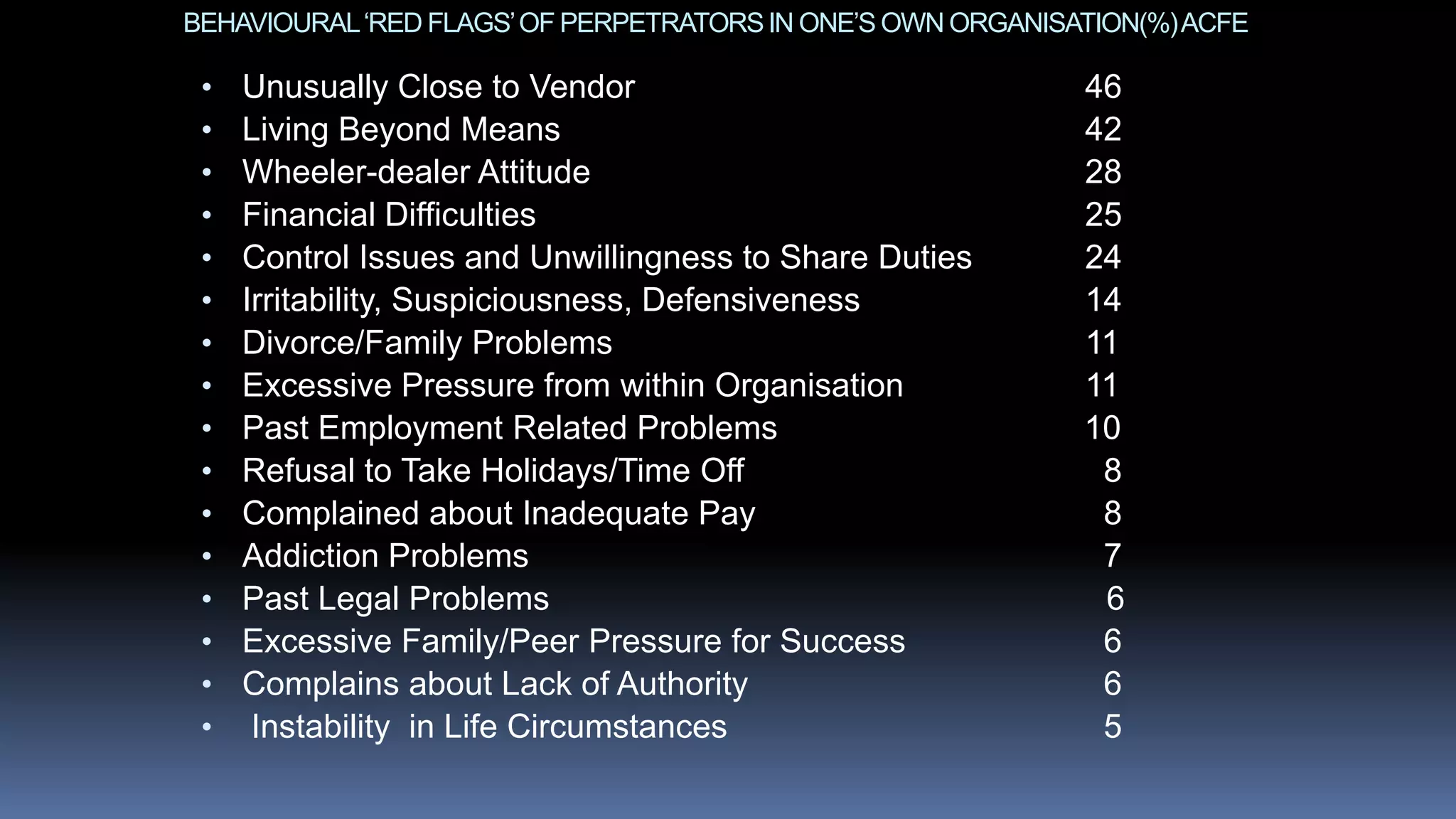

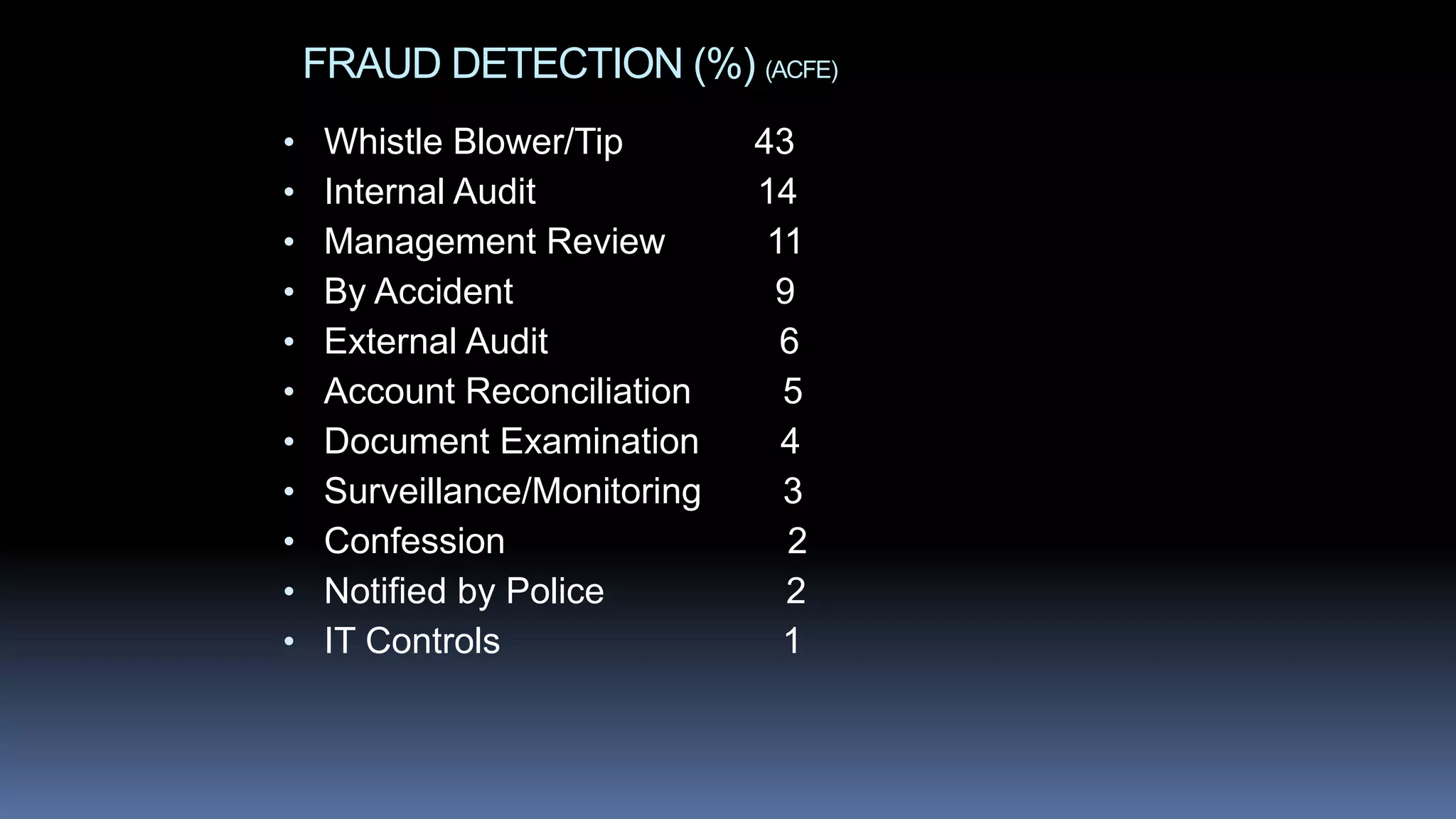

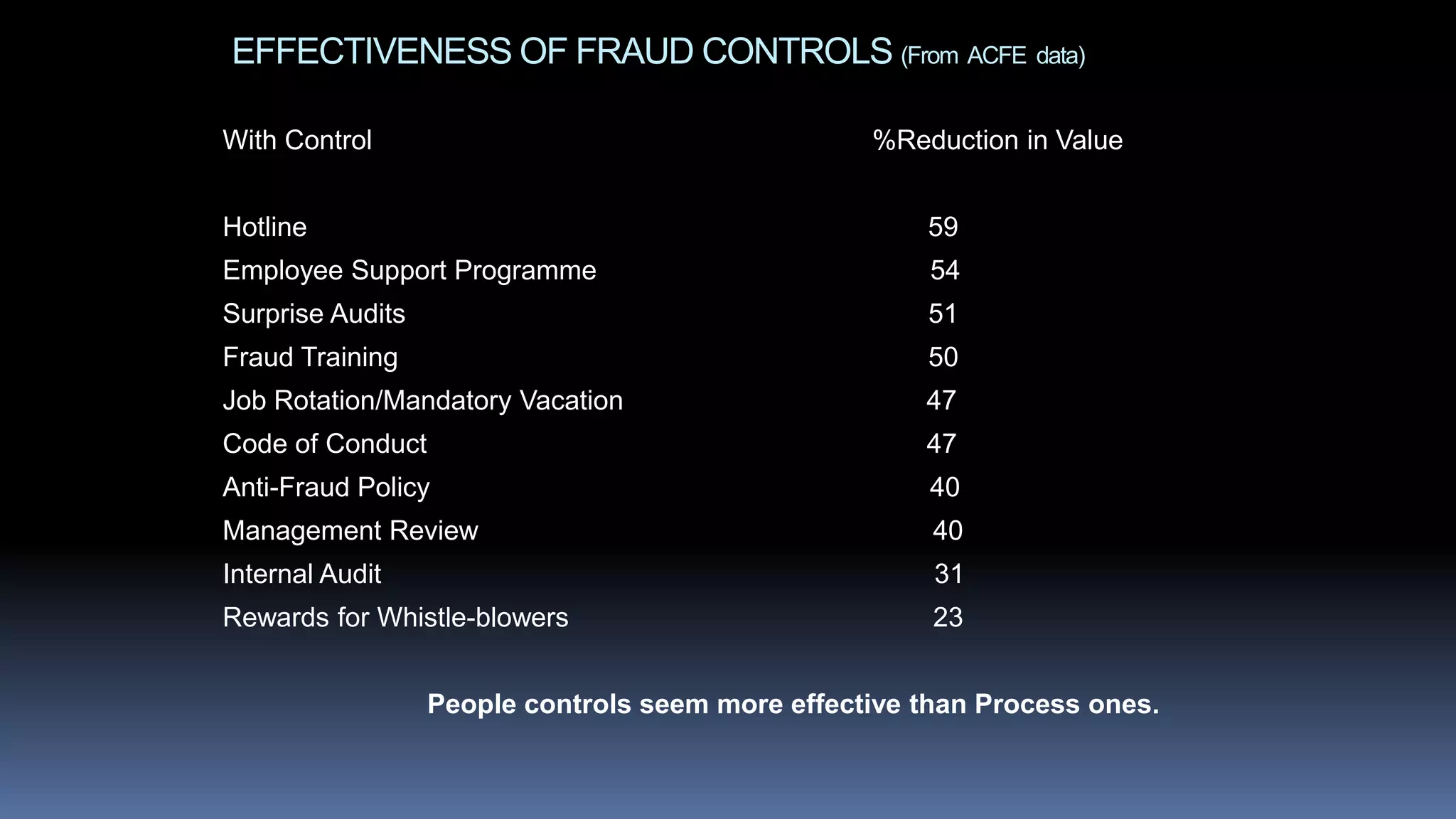

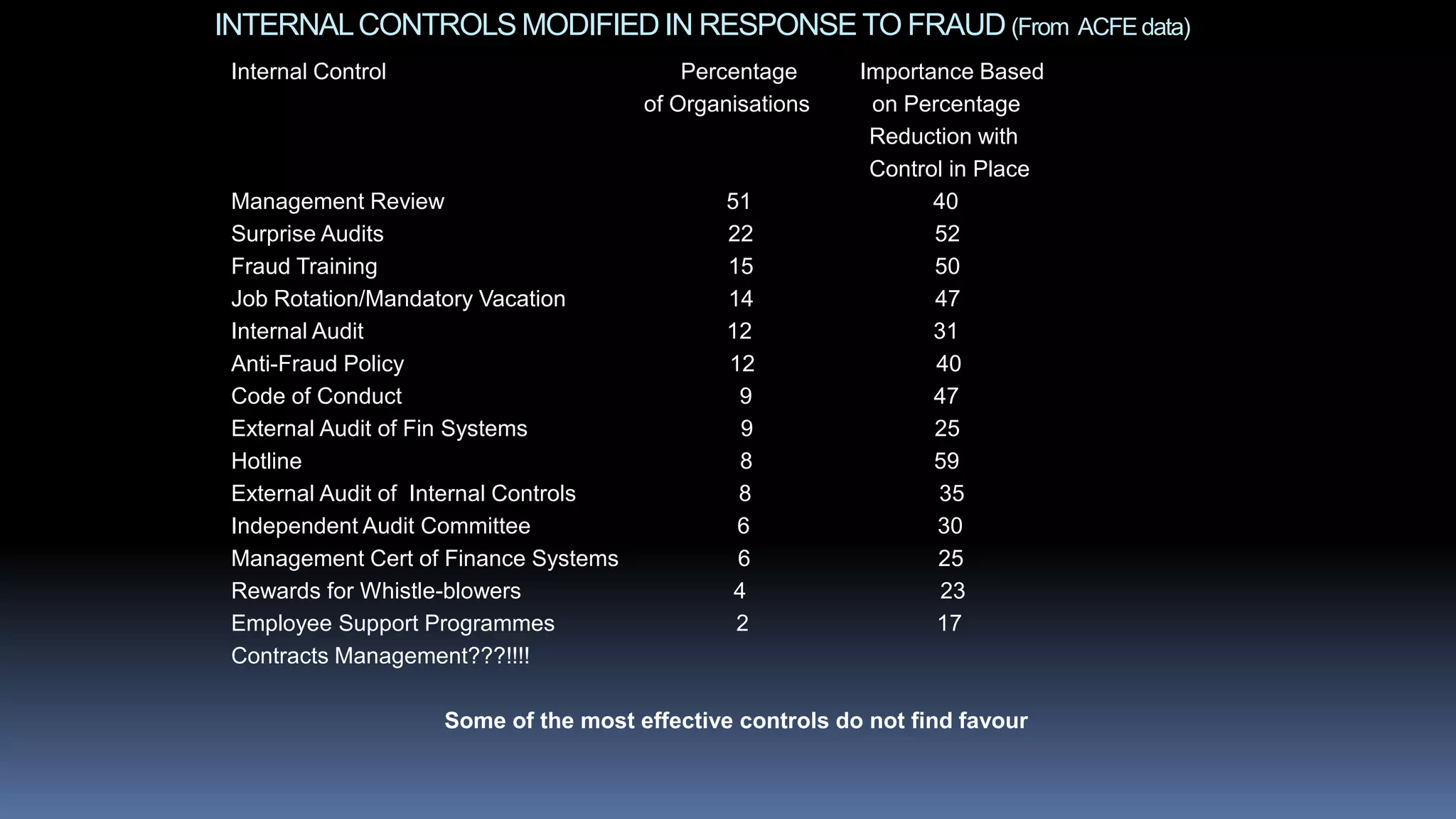

The document discusses ways to combat procurement fraud in the public sector. It begins by showing where the UK ranks globally in reducing corruption. It then outlines the main opportunities for fraud during the pre-contracting, contracting, tendering, and post-contract phases. Examples of corrupt benefits and behaviors of fraud perpetrators are provided. The document also discusses effective internal controls and fraud detection methods based on data from organizations that have experienced fraud. It concludes by recommending investing in effective contract management and other fraud prevention measures.