Downloaded 703 times

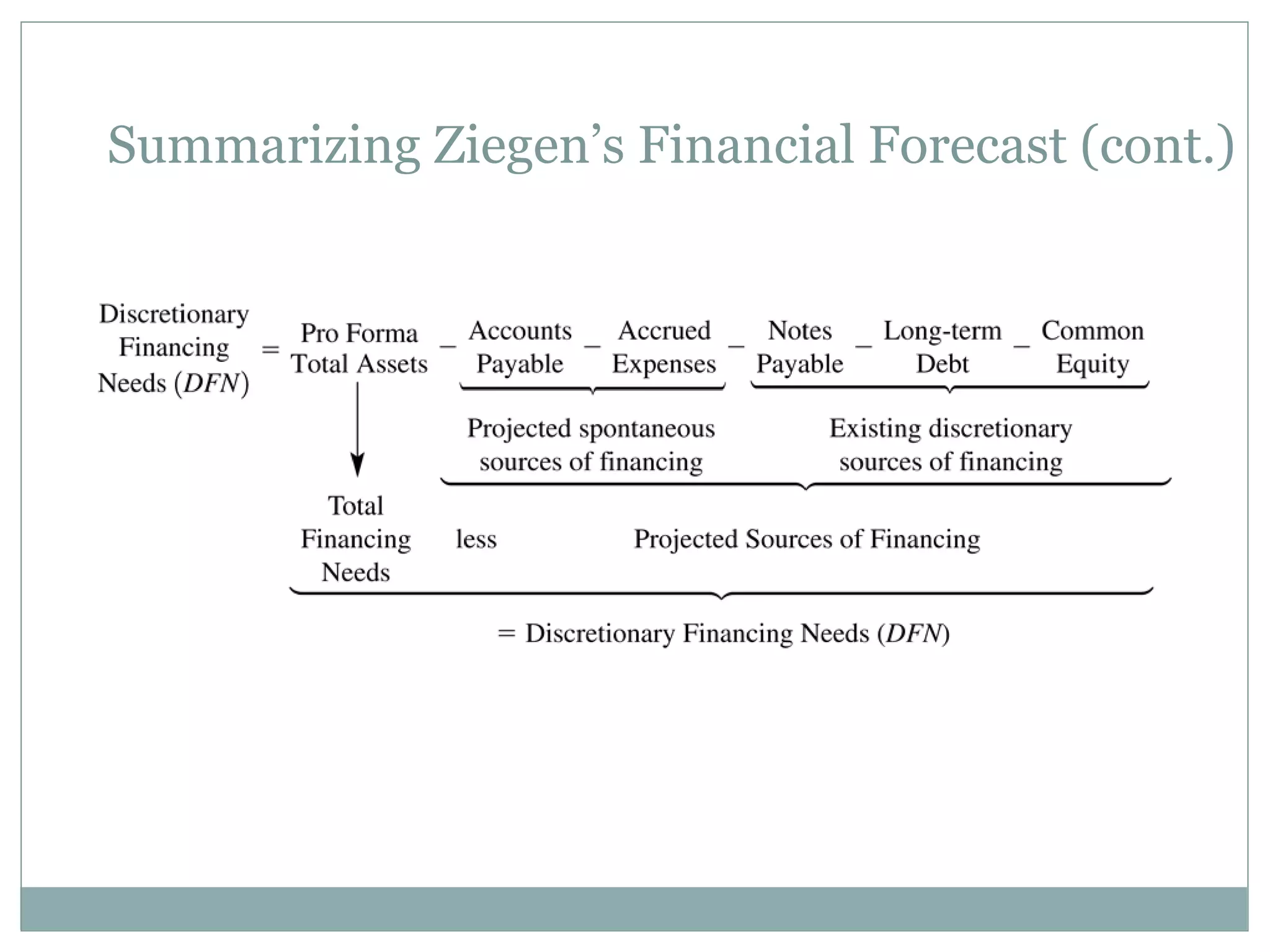

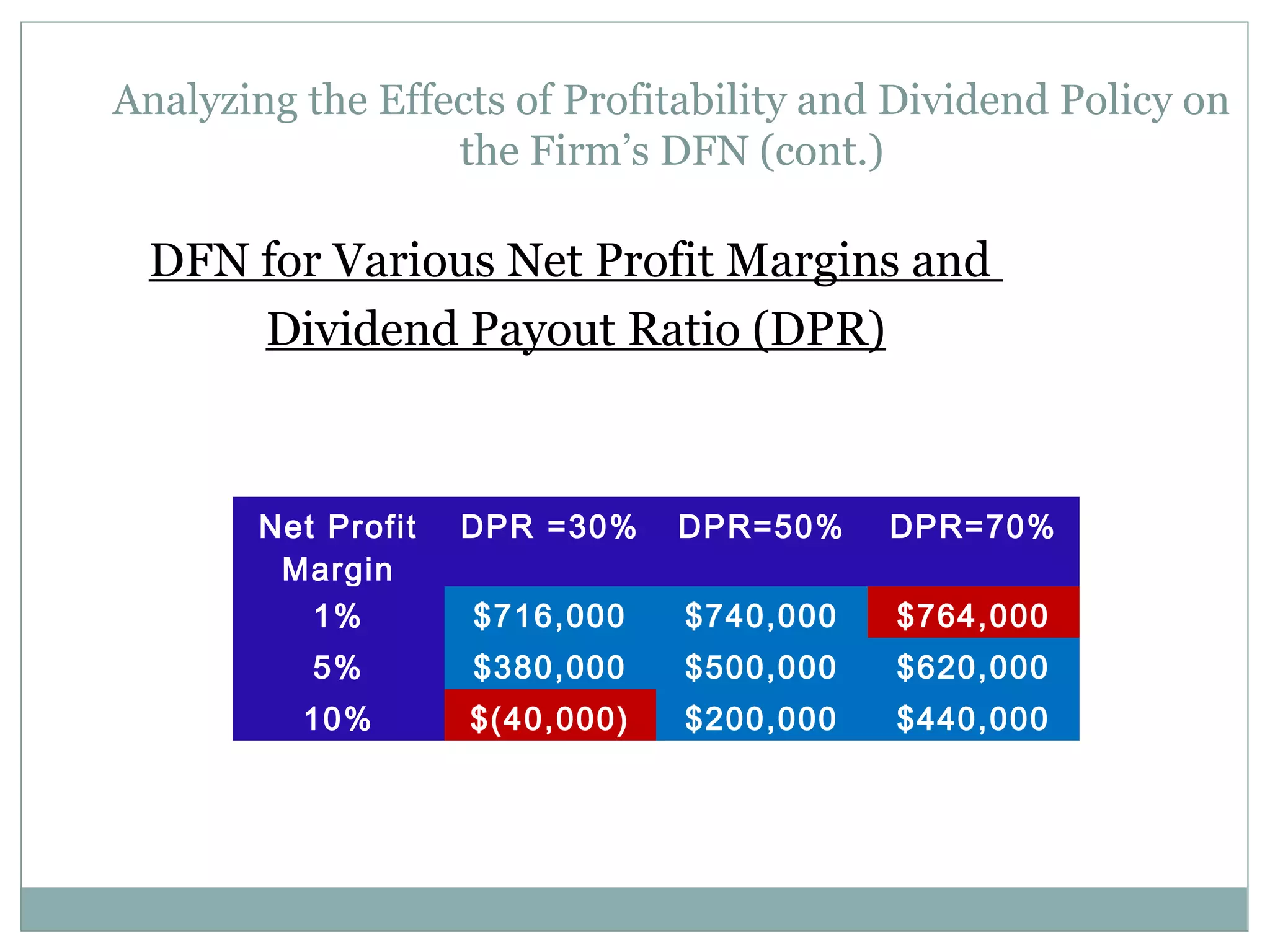

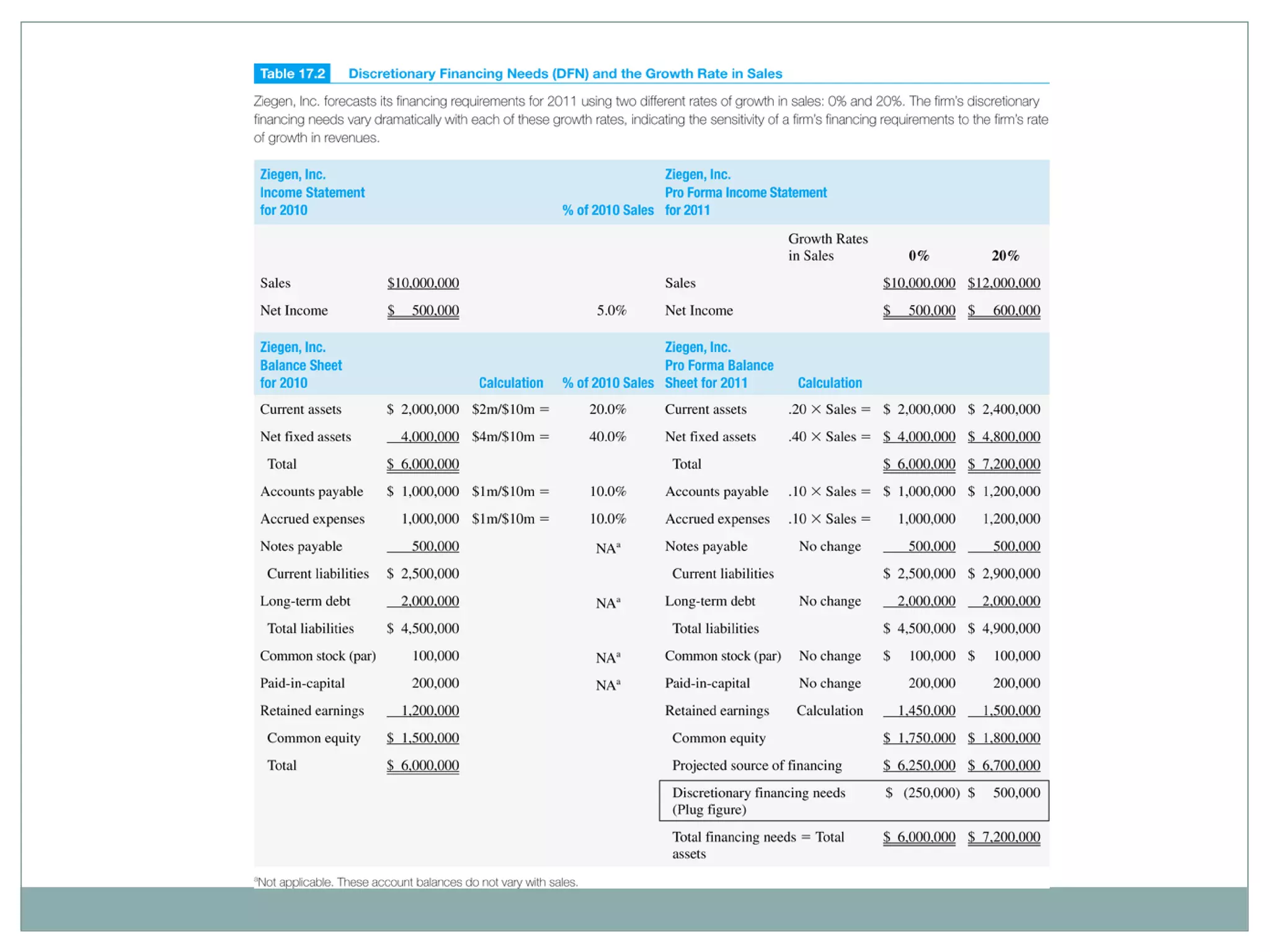

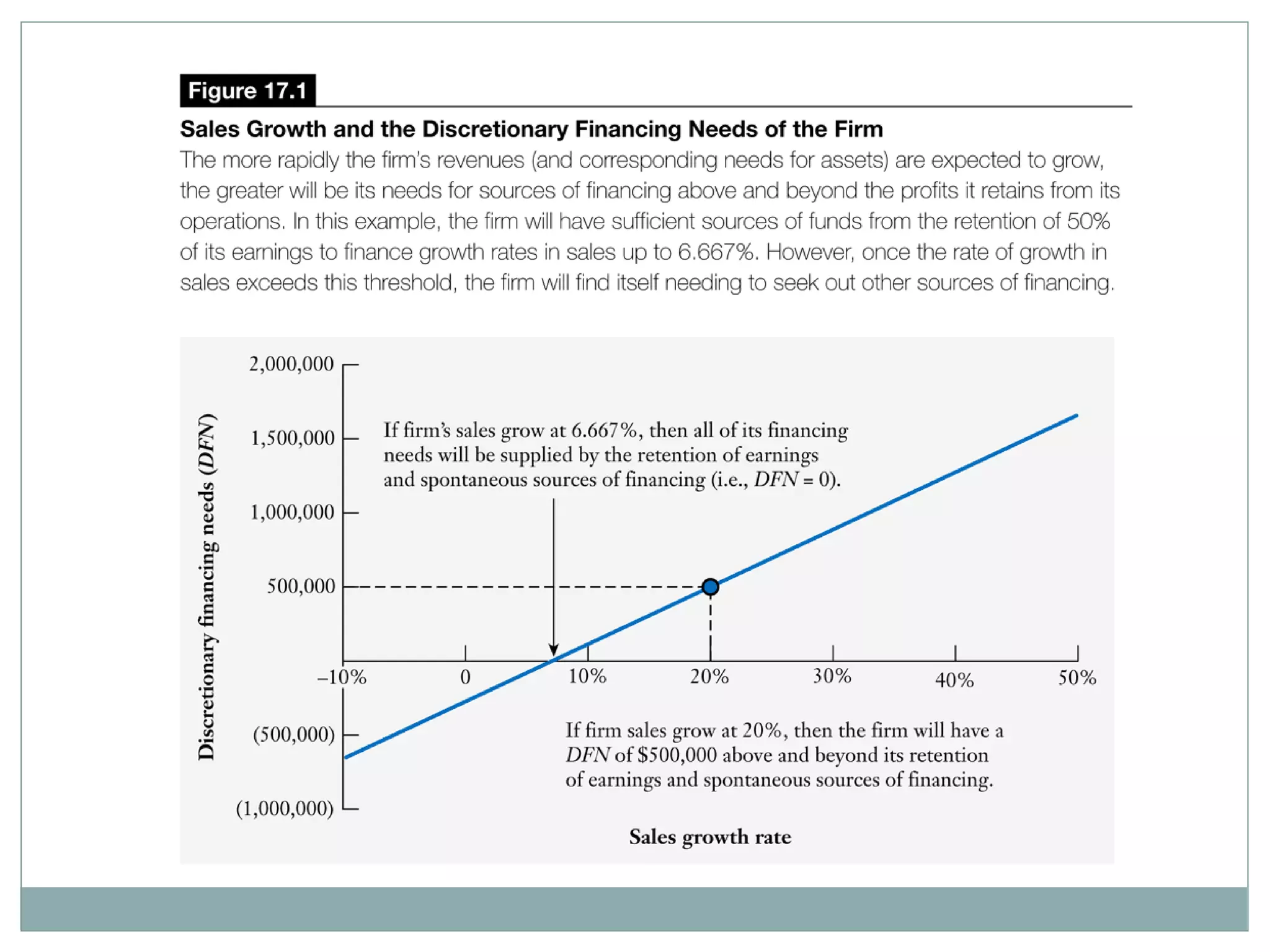

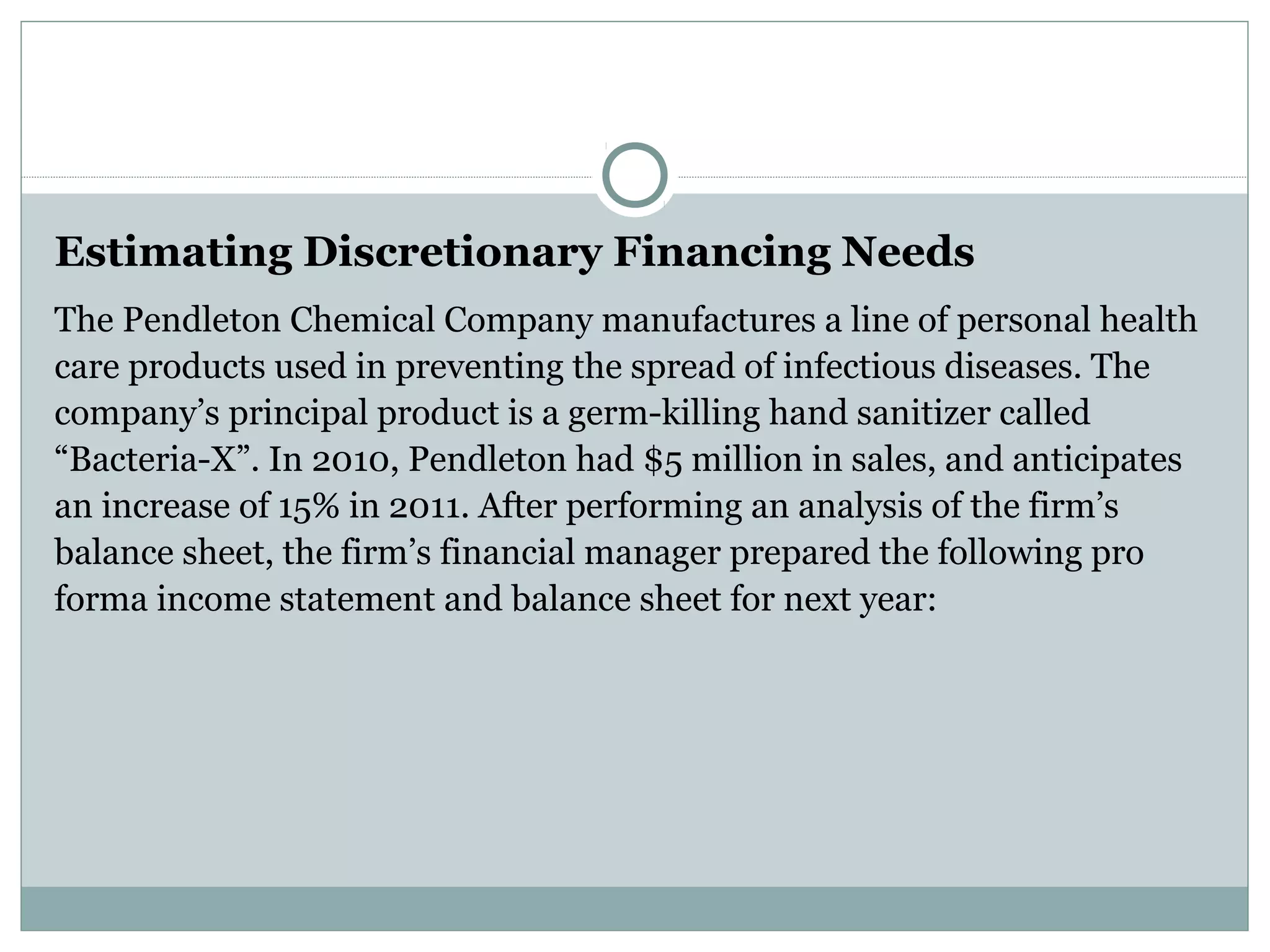

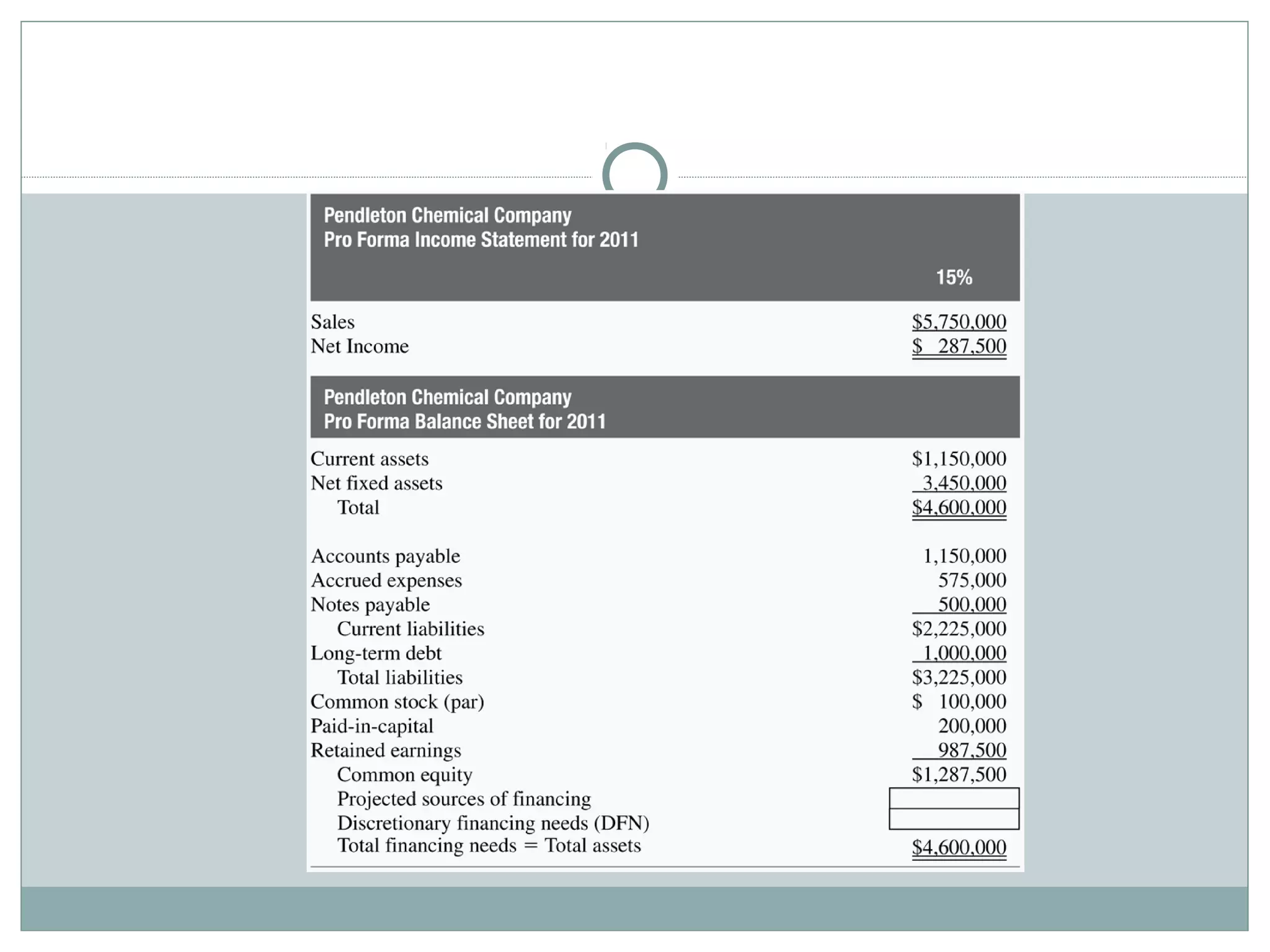

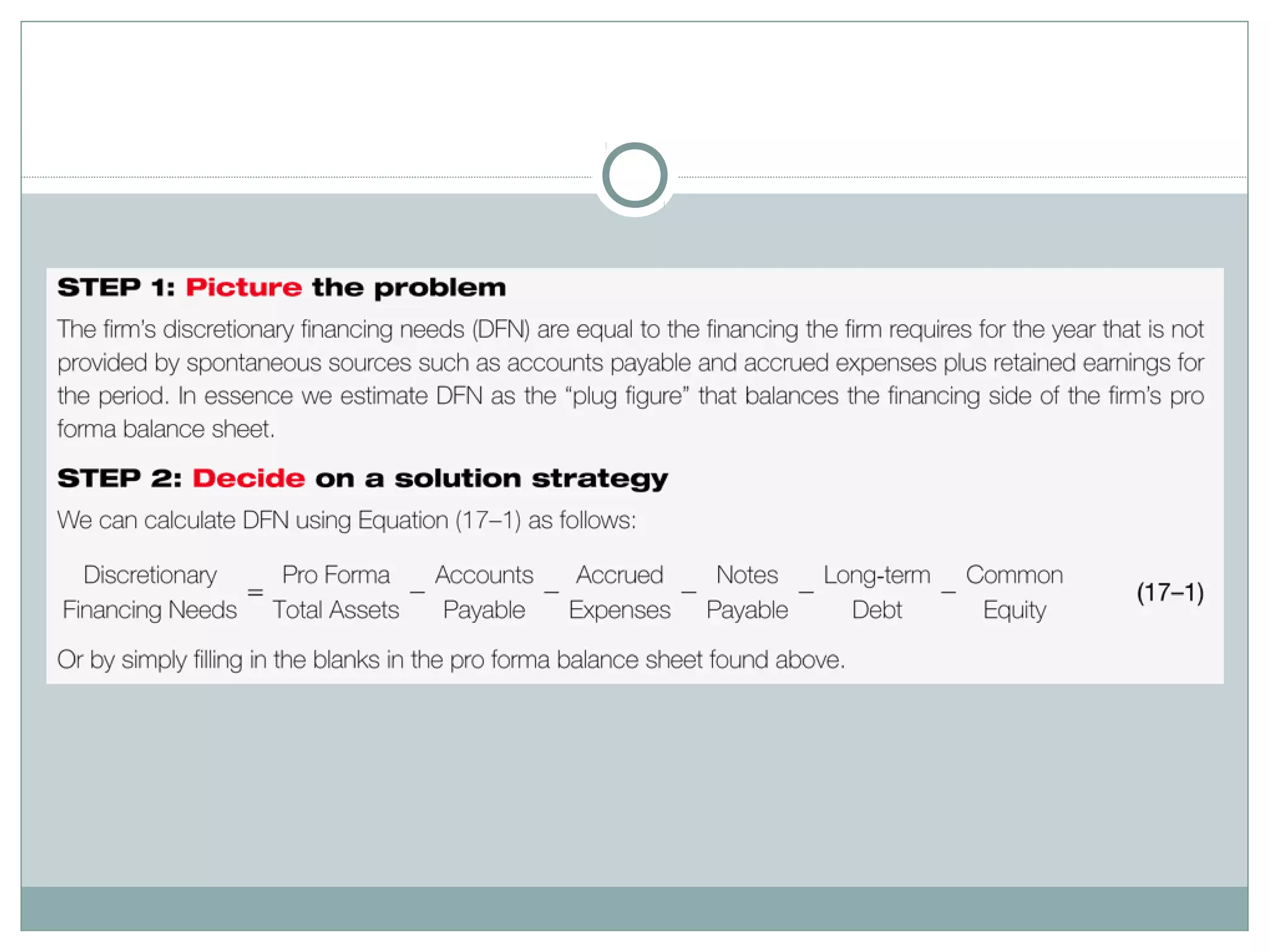

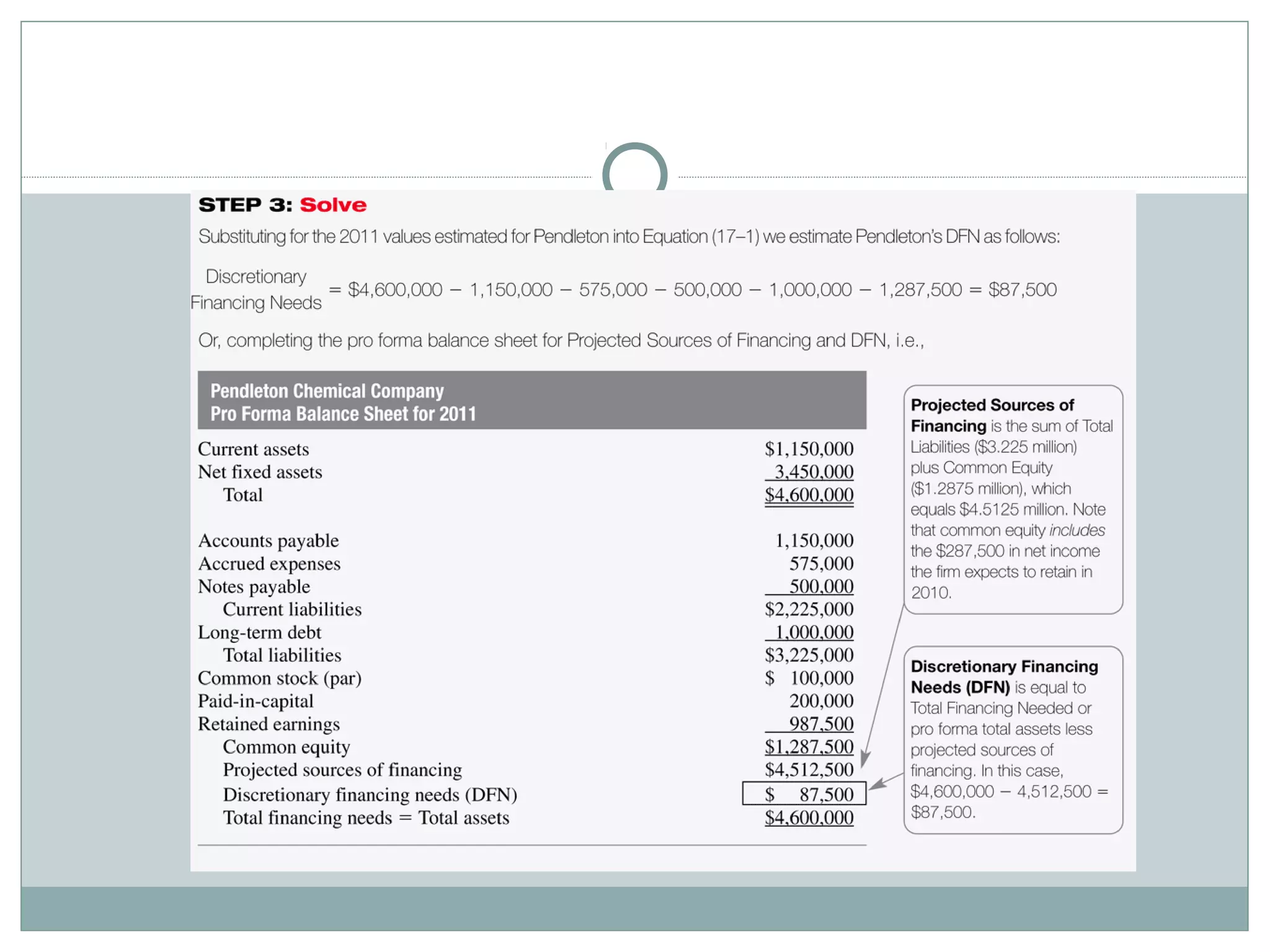

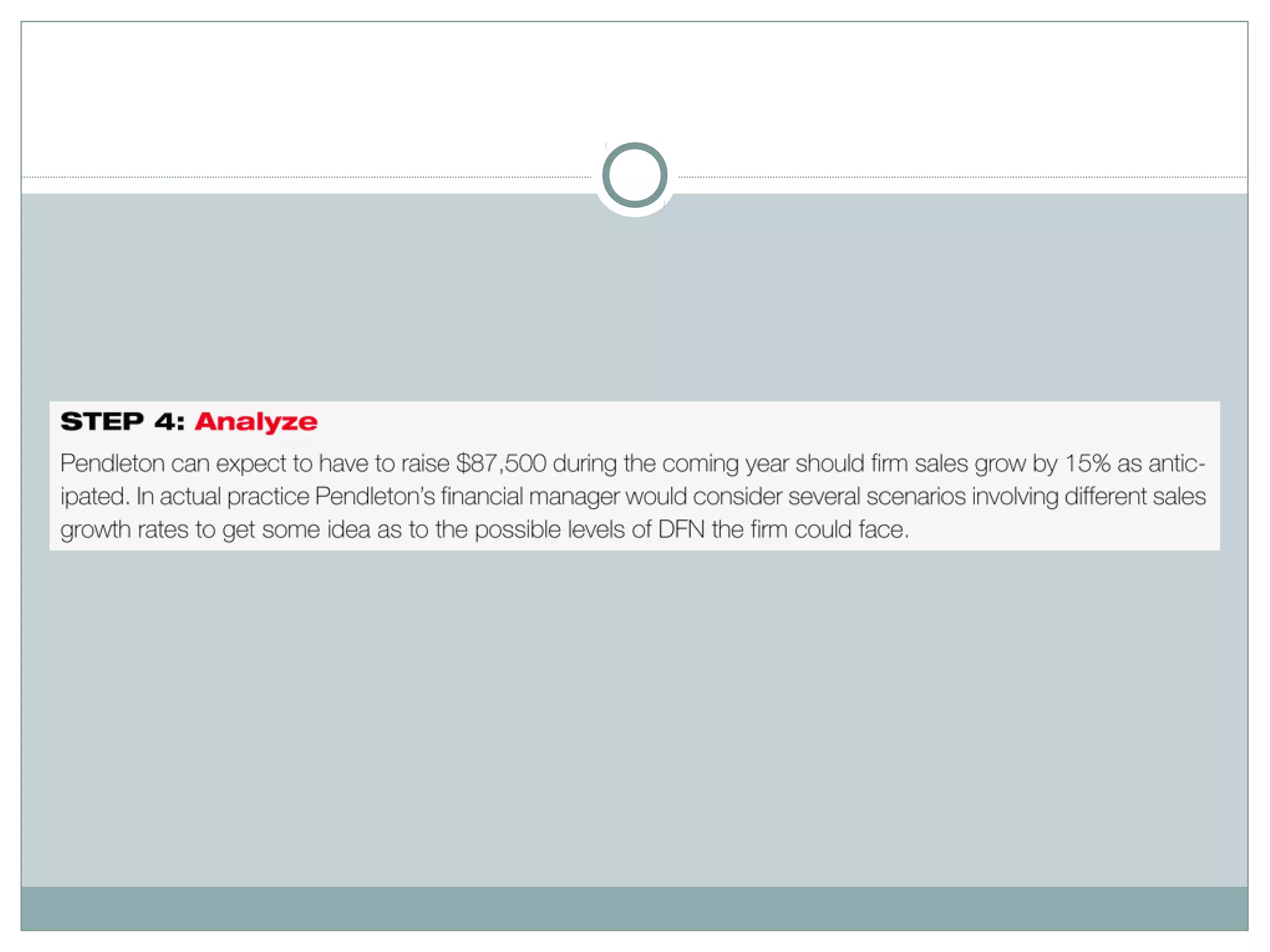

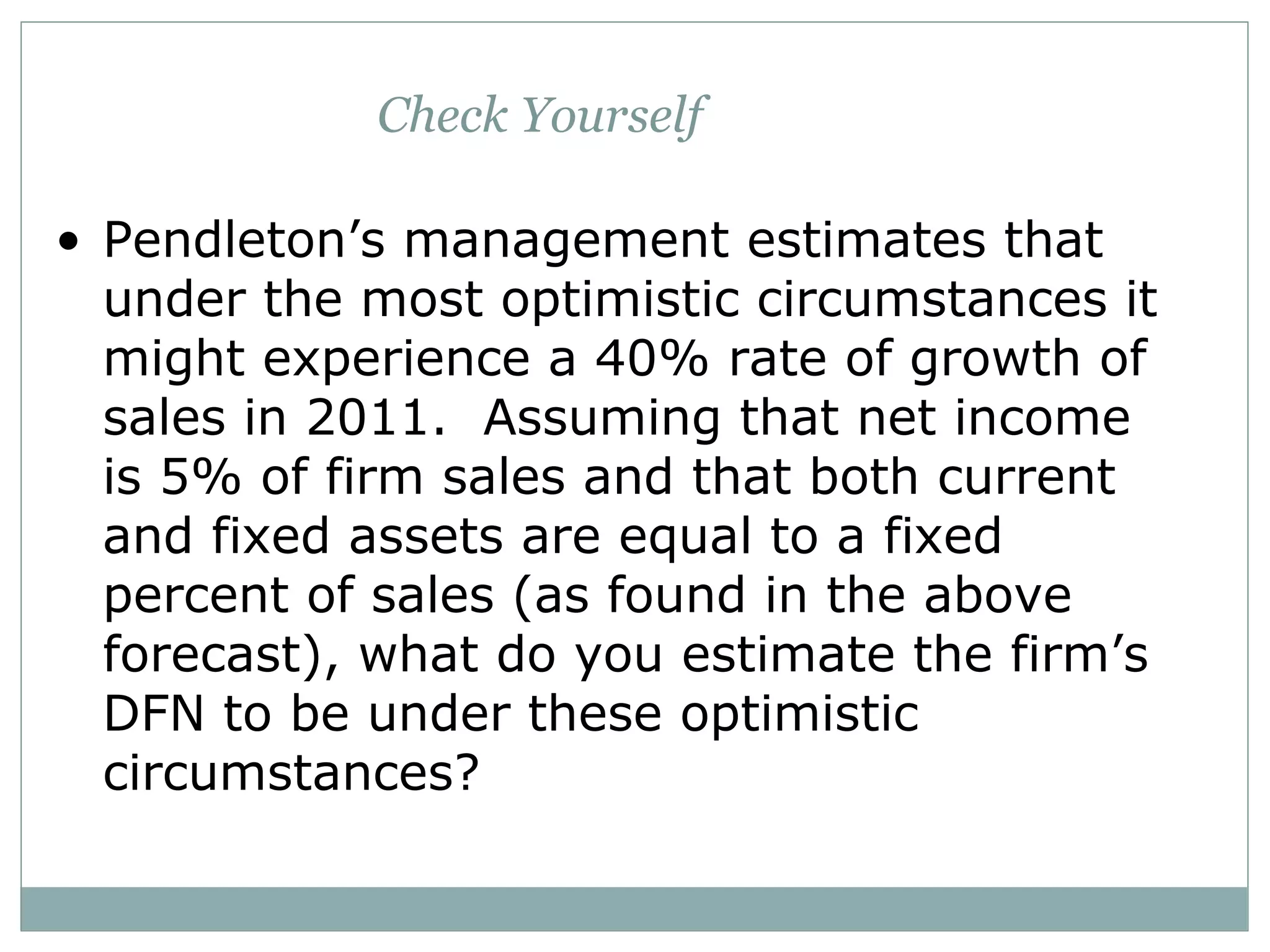

The document discusses developing long-term and short-term financial plans, including using the percent of sales method to forecast financing needs, preparing pro forma financial statements and cash budgets, and analyzing how changes in variables like sales growth, profitability, and dividend policy impact a firm's discretionary financing needs. It also covers uses of the cash budget to predict financing requirements and monitor operations.