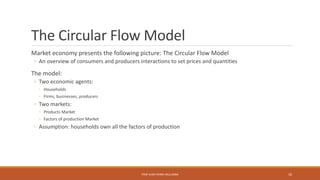

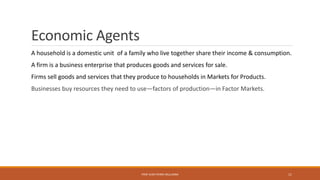

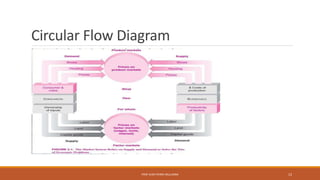

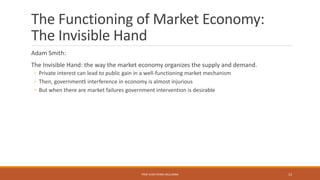

This chapter discusses the modern mixed economy. It begins by defining a market as a mechanism that allows buyers and sellers to set prices and exchange goods. It then explains how markets solve the three fundamental economic questions of what, how, and for whom through the interaction of consumers and producers. While the invisible hand of the market guides much of the economy, the visible hand of government also plays an important role by increasing efficiency, promoting equity, and ensuring stability. Government works to address market failures from monopolies, externalities, and public goods through regulations and tax-funded programs. The chapter establishes the foundation for understanding the roles of markets and government in modern economies.