Downloaded 682 times

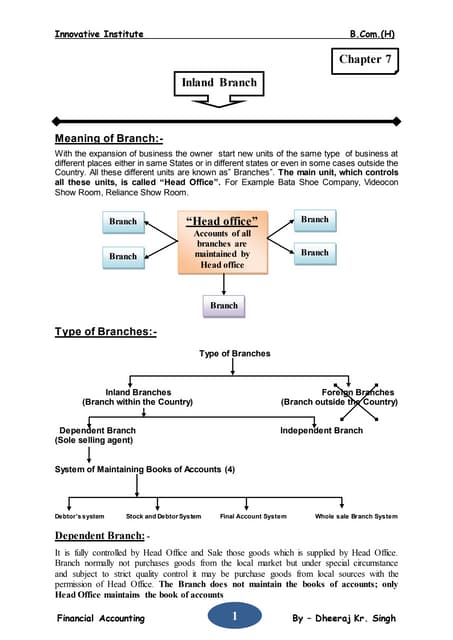

![In the books of H.O.

Trading Account for the year ended……………

Note: 1. Discount allowed to customer will appear in Branch Profit & Loss Account.

2. Loss through natural wastage is a normal loss and as such, the same should be charged

against branch gross profit. So, no adjustment is required.

SOLUTION:

Particulars Amount Amount Particulars Amount Amount

To Opening Stock

Less: Loading

,, Goods sent to Branch

Less: Returns to H.O.

Less: Loading

(1/4× 2,40,000)

[1/3 on CP = 1/4 on

SP]

,, Gross Profit c/d

40,000

10,000

2,50,000

10,000

2,40,000

60,000

30,000

1,80,000

2,35,000

4,45,000

By Sales:

Cash

Credit

,, Closing Stock

Less : Loading

(1/4× 60,000)

1,00,000

3,00,000

60,000

15,000

400000

45000

4,45,000](https://image.slidesharecdn.com/branchaccounting-150606163115-lva1-app6891/75/Branch-accounting-11-2048.jpg)

- A branch is a business unit located away from the home office that carries out similar business activities. It obtains inventory from the home office, makes sales, approves customer credit, and collects payments. - Branches are classified as dependent or independent based on where their accounting records are maintained. Foreign branches operate in a country other than where the company is incorporated. - There are different methods for accounting for branch operations, including the final accounts method, debtors method, and stock and debtors method. Goods may be invoiced to branches at cost or above cost price.