Downloaded 63 times

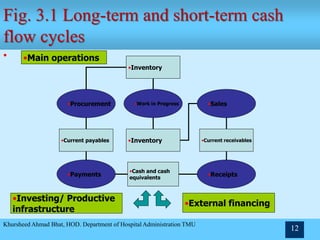

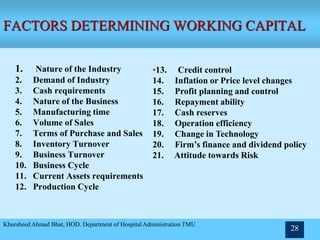

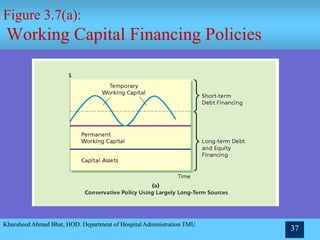

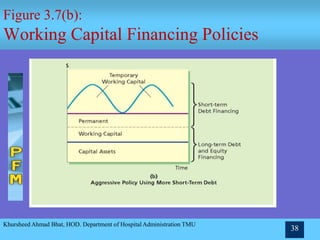

1. The document discusses the cash flow statement, which presents information about a company's cash flows from operating, investing, and financing activities. It explains the usefulness of cash flow information and the relationship between cash flows and profits. 2. The cash flow statement is prepared using either the direct or indirect method. The direct method shows actual cash inflows and outflows, while the indirect method reconciles net income to cash flows from operations. Cash flows from investing and financing activities are also presented. 3. Effective management of working capital and the appropriate mix of short-term versus long-term financing of current assets is important for business liquidity and performance. The document discusses various principles and policies for working capital management.