Downloaded 75 times

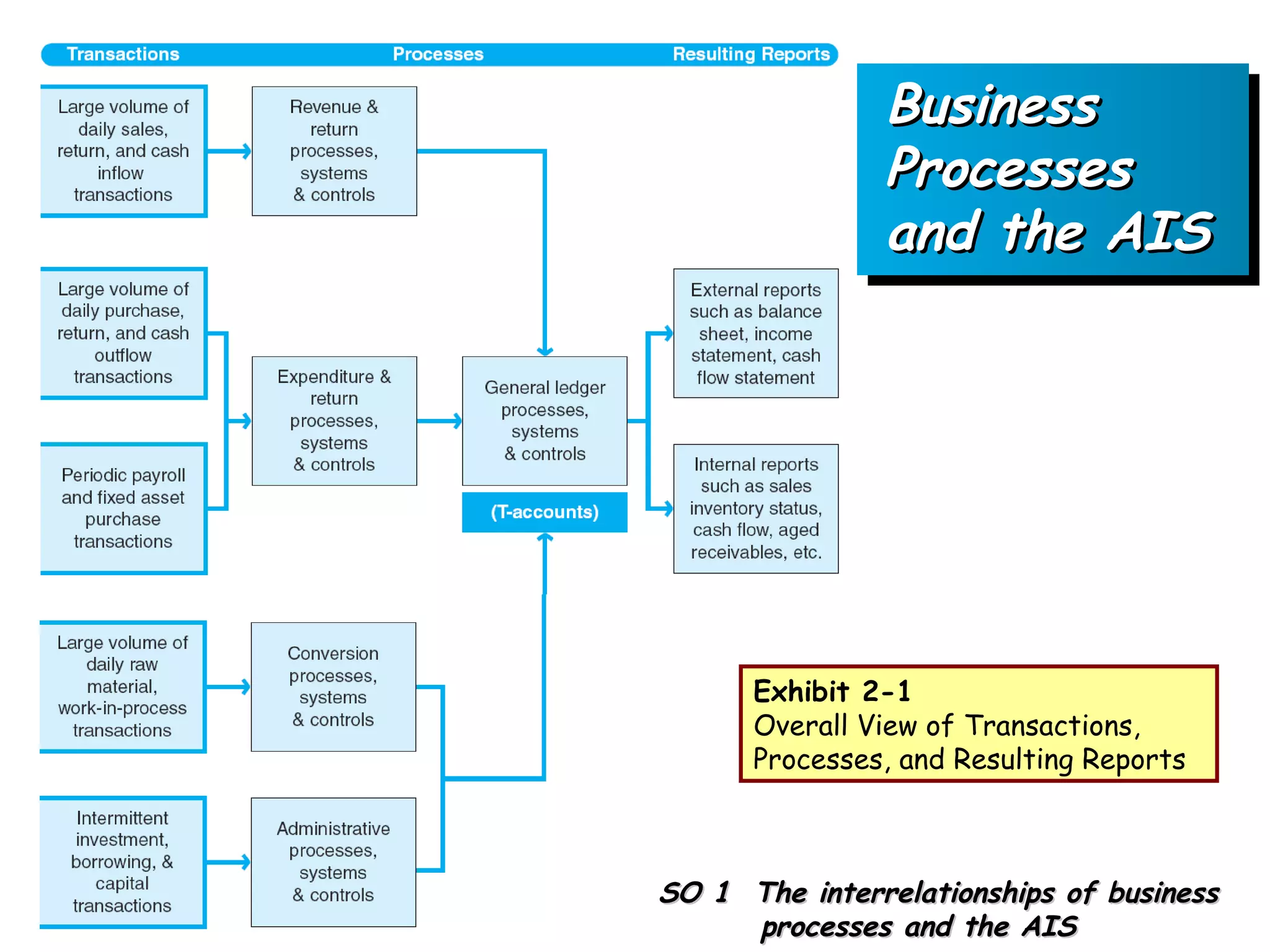

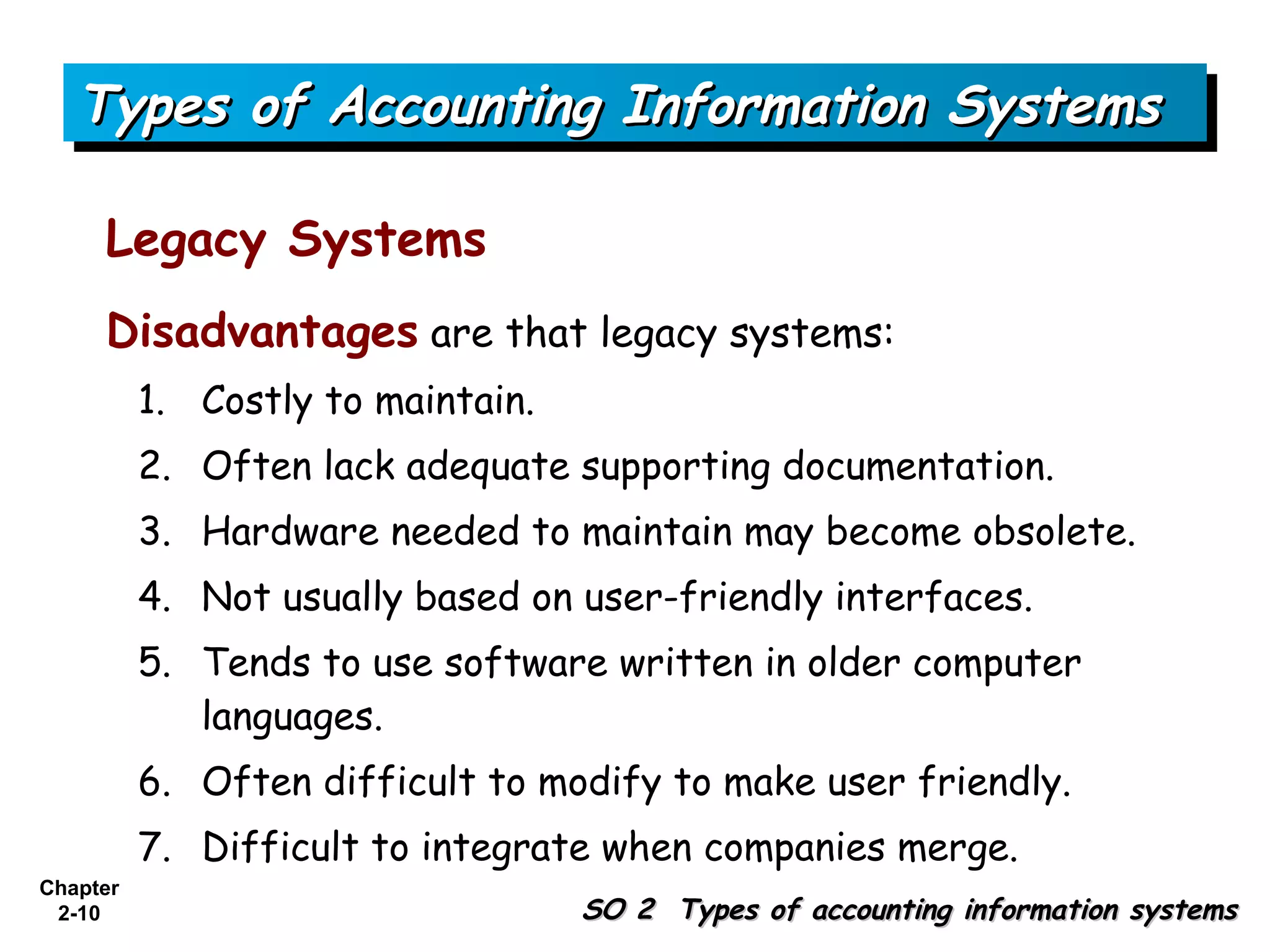

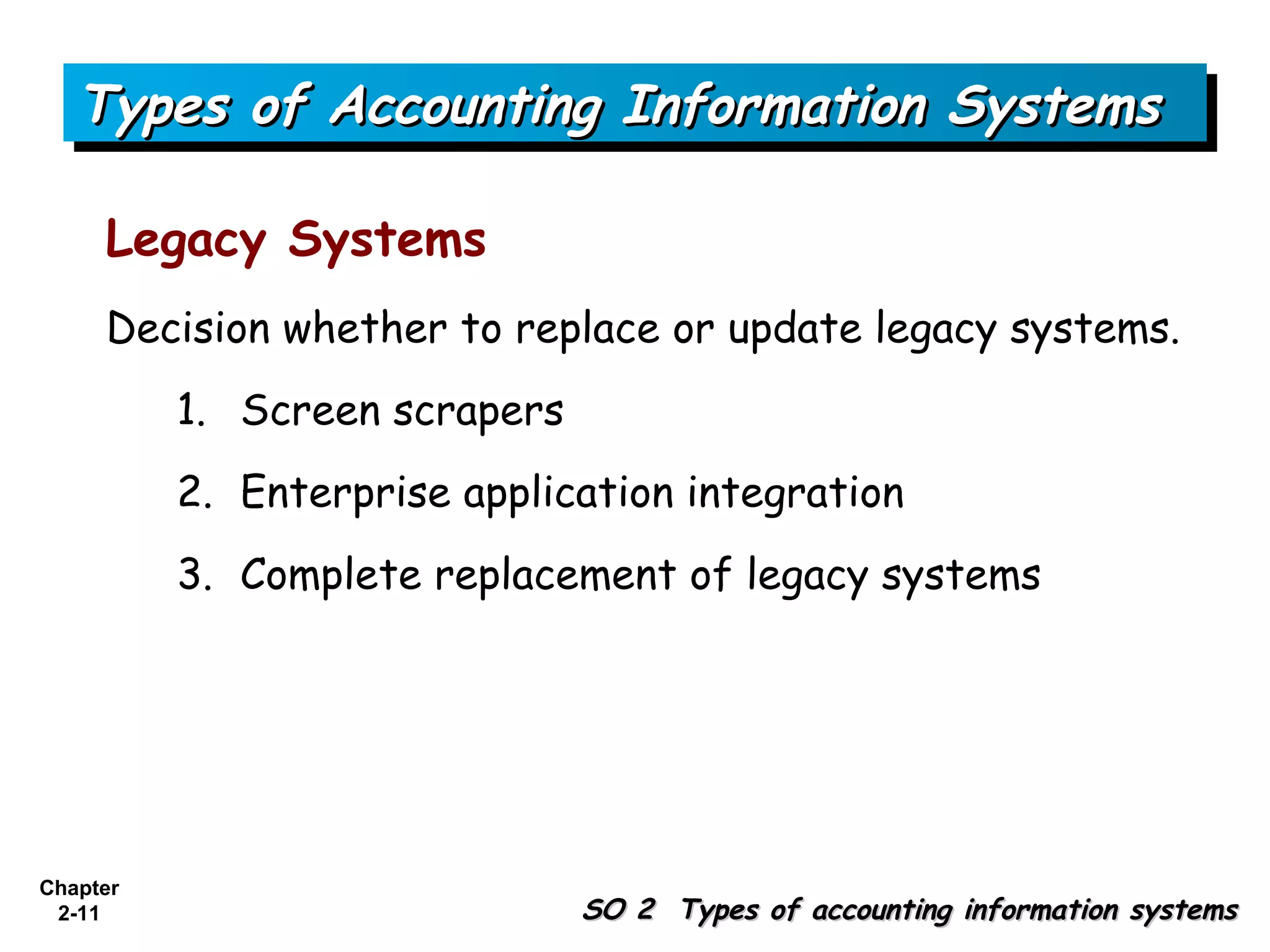

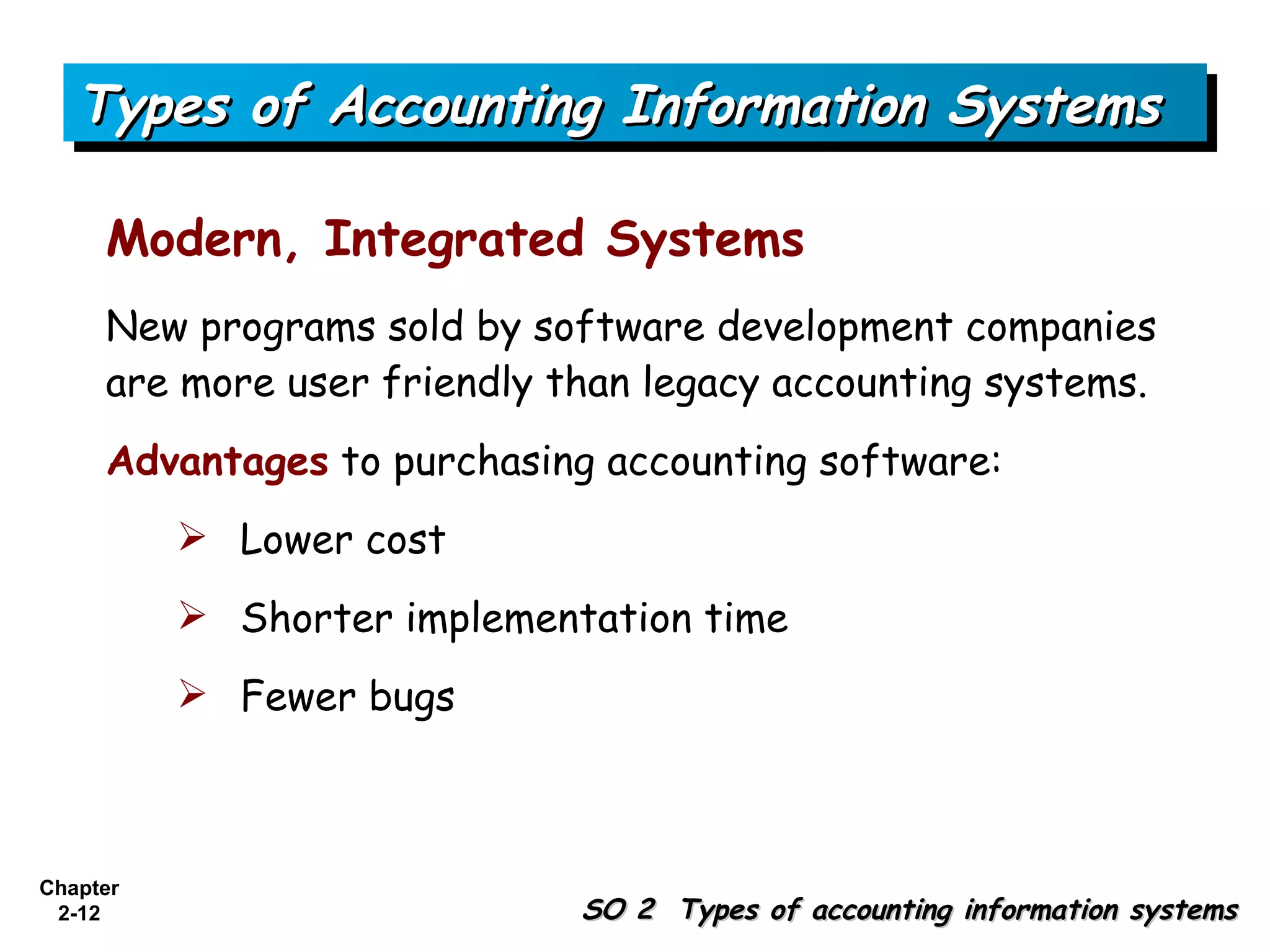

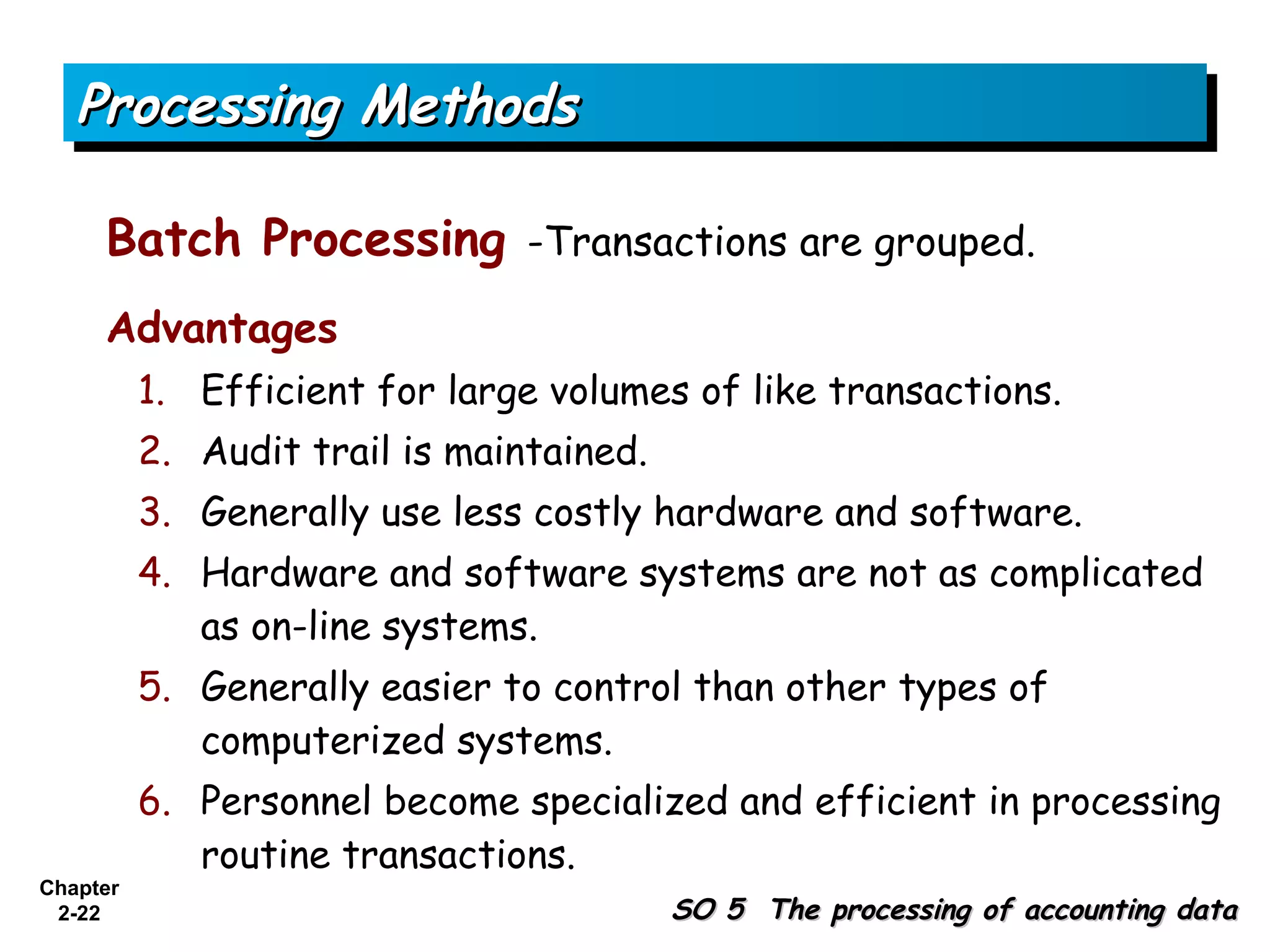

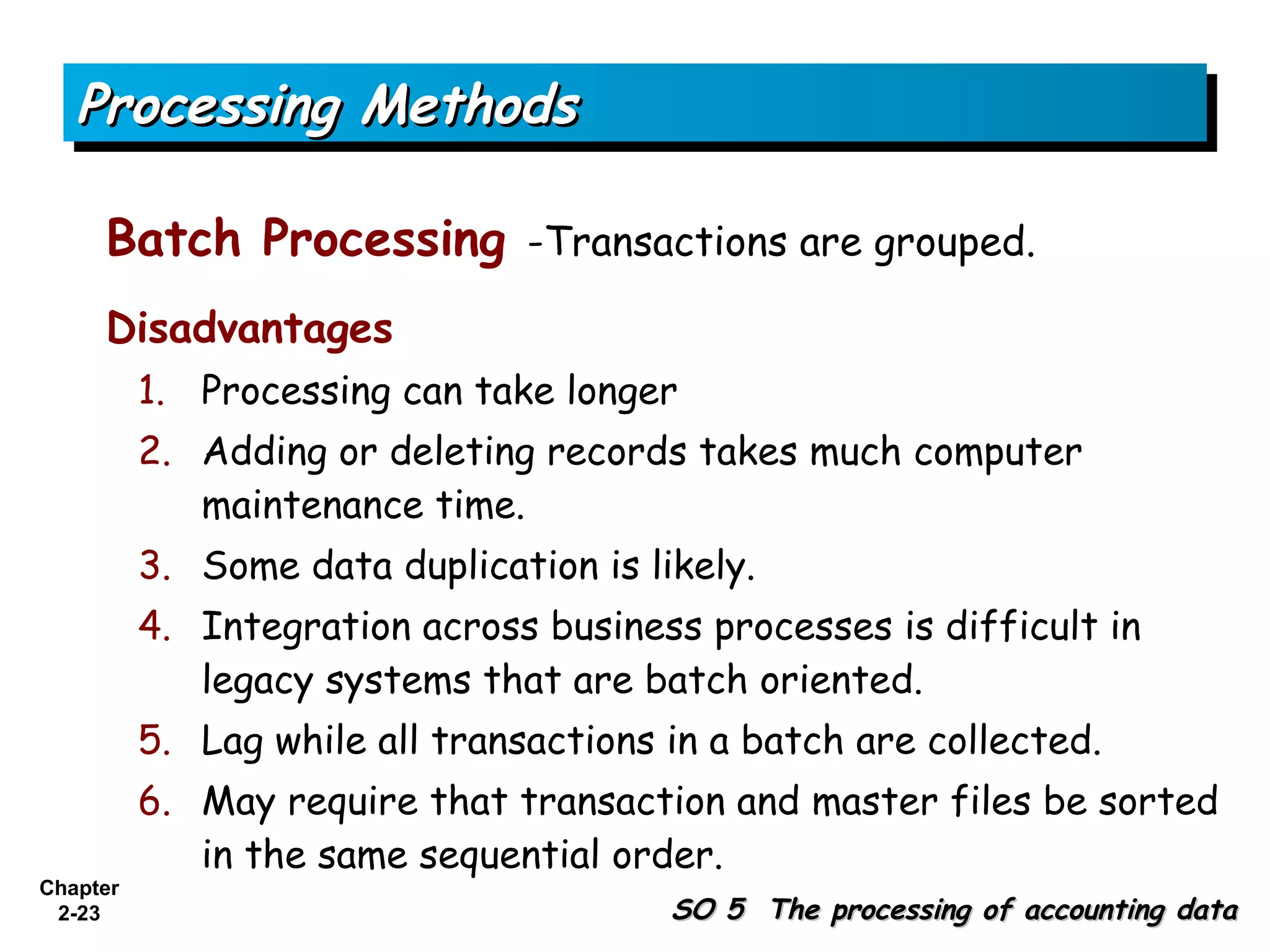

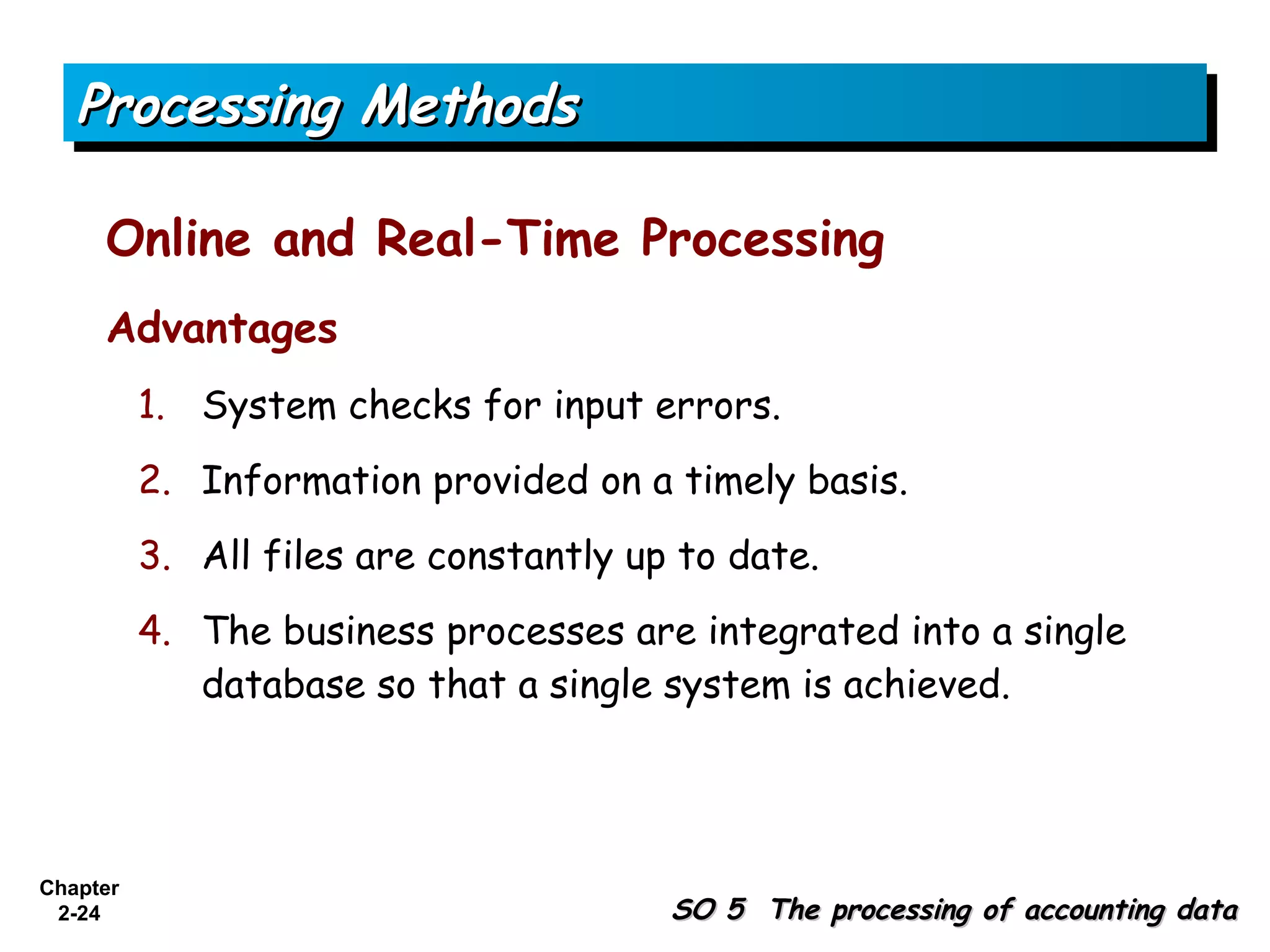

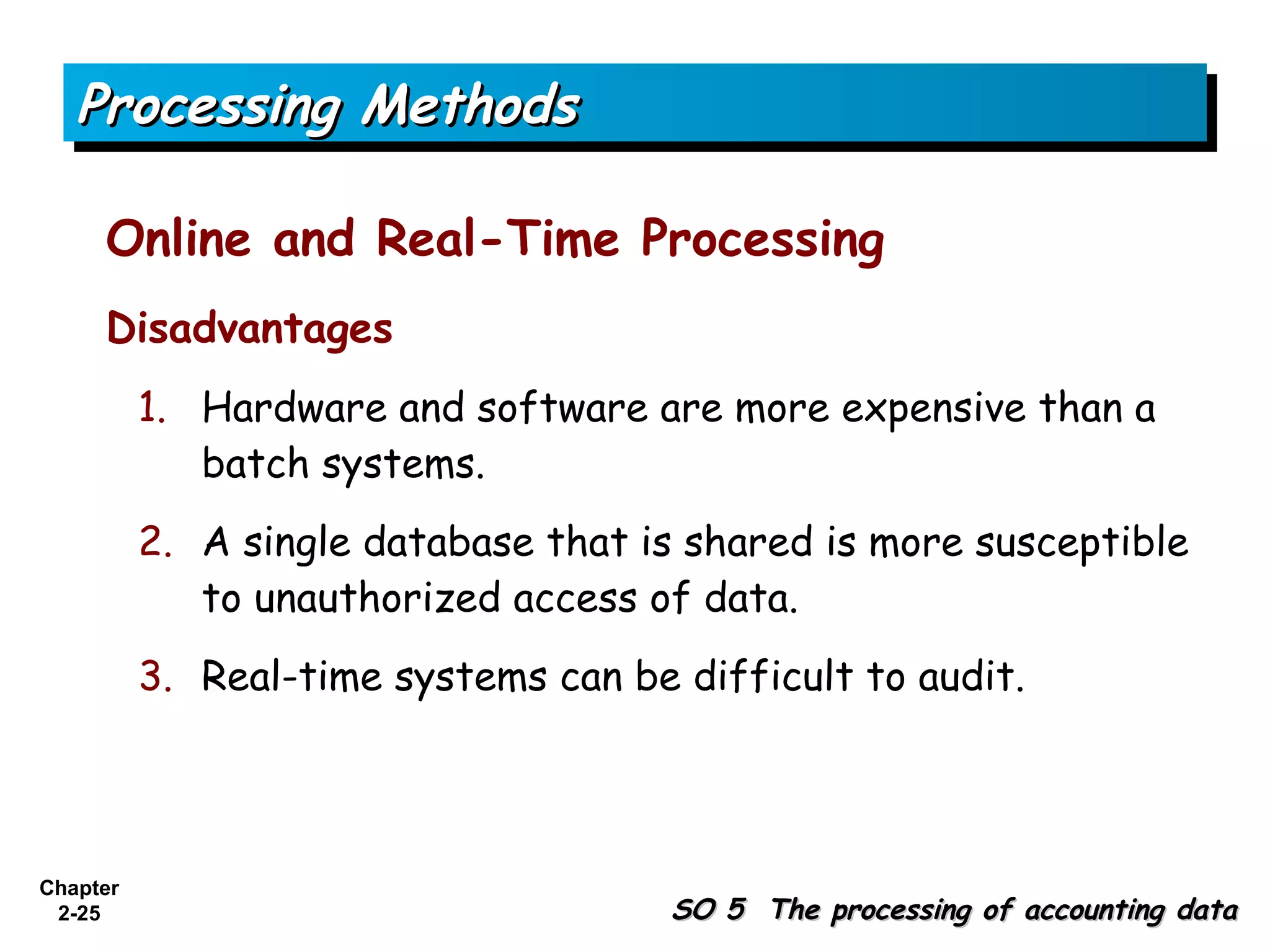

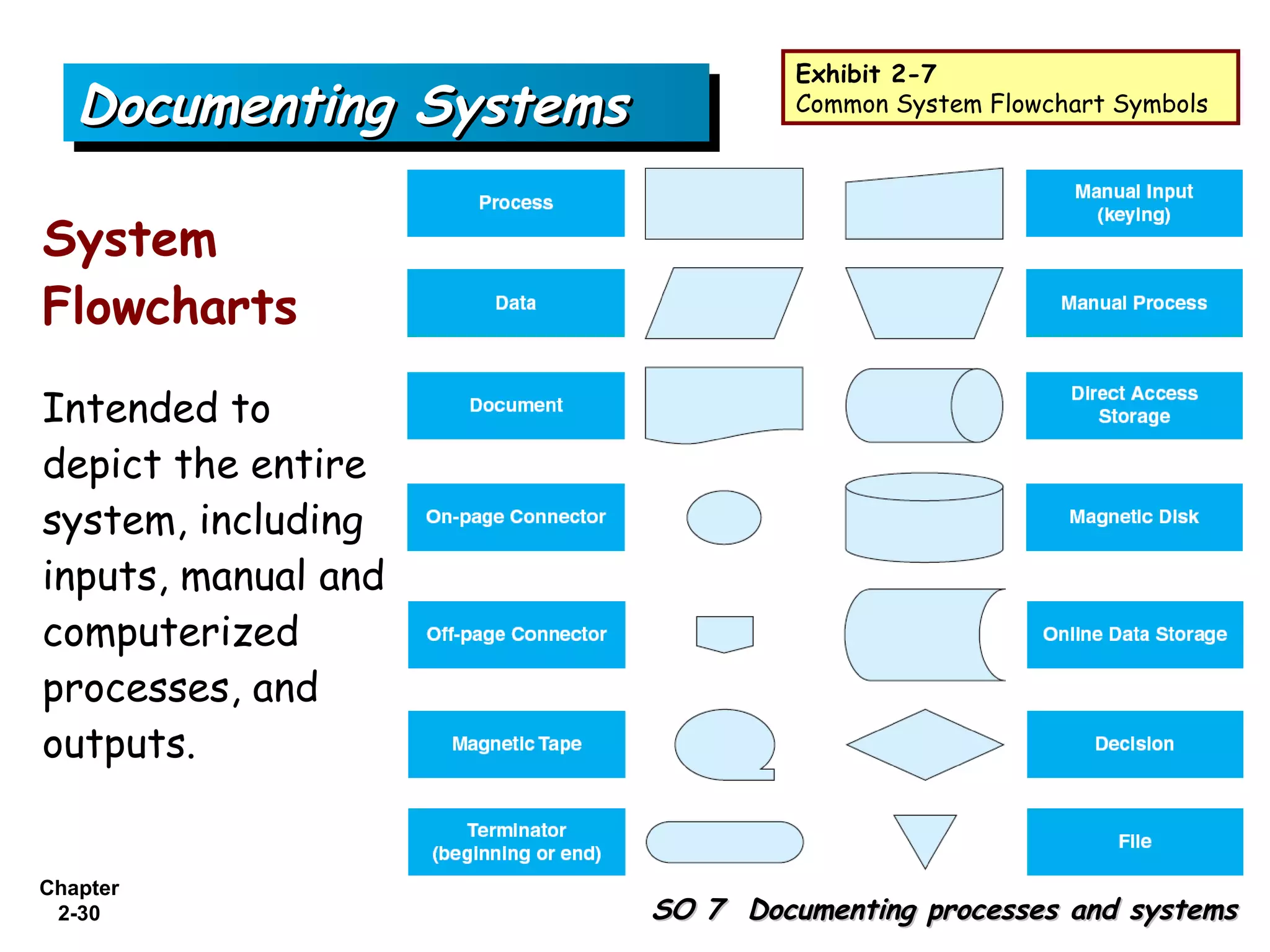

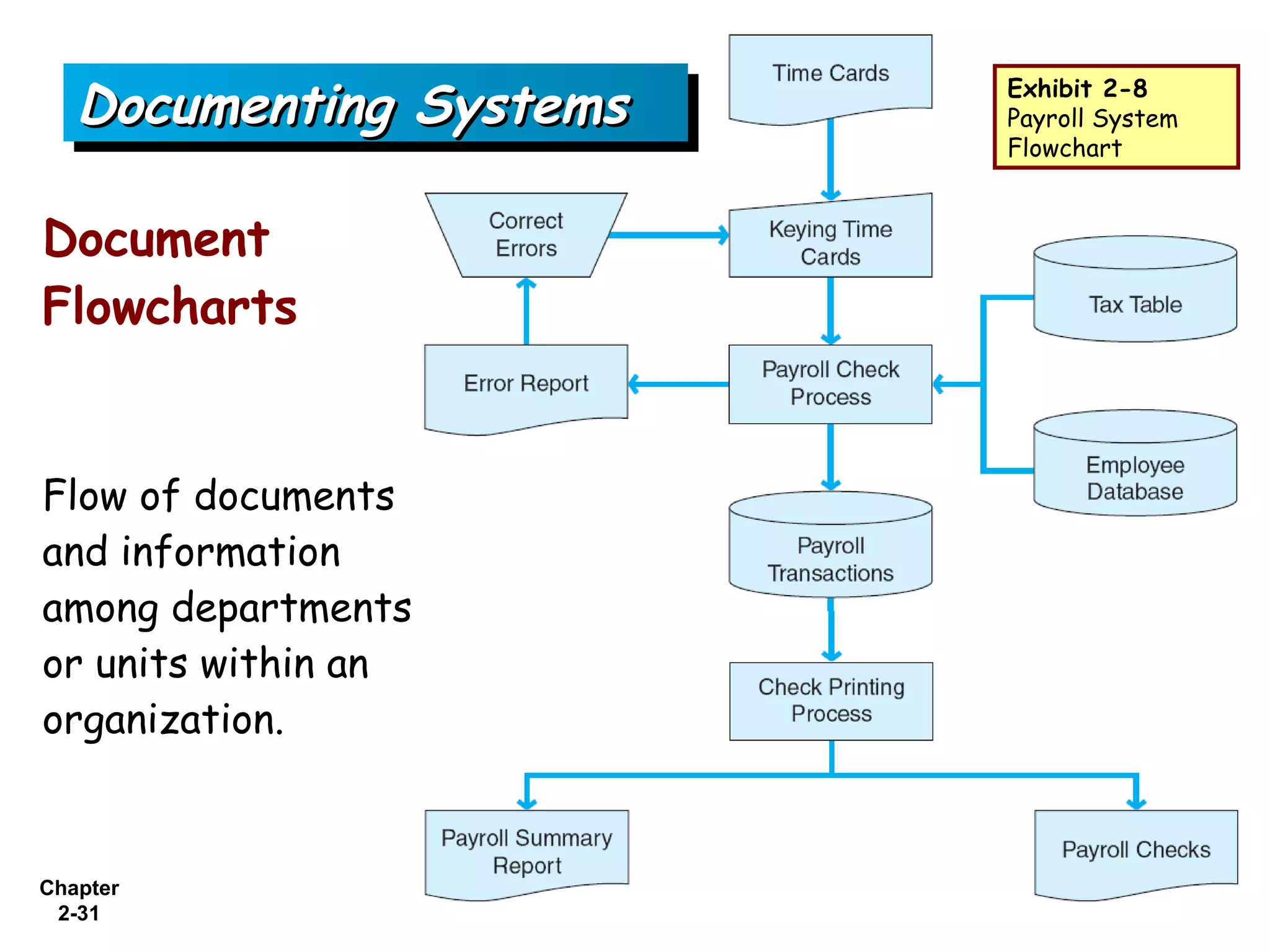

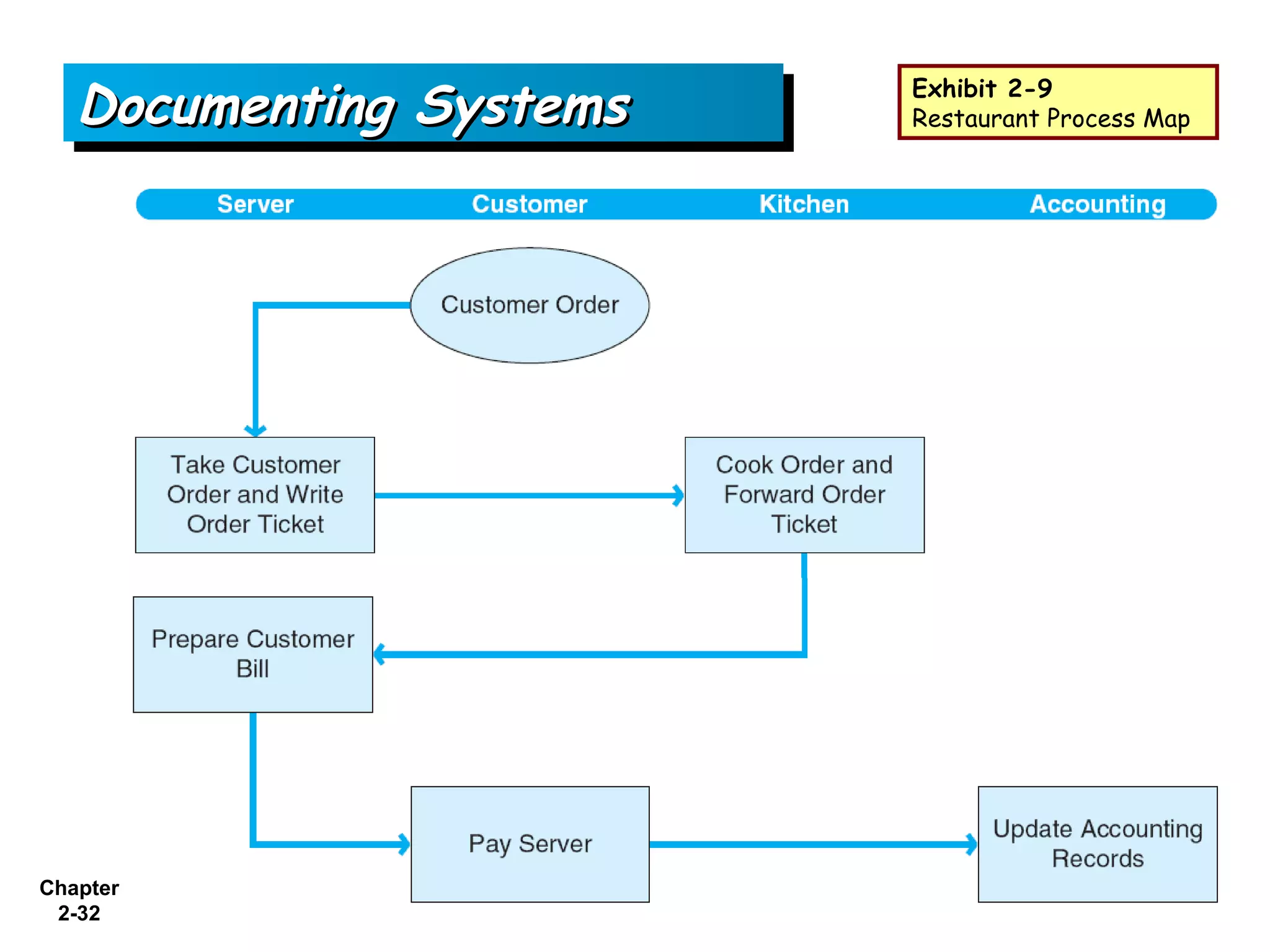

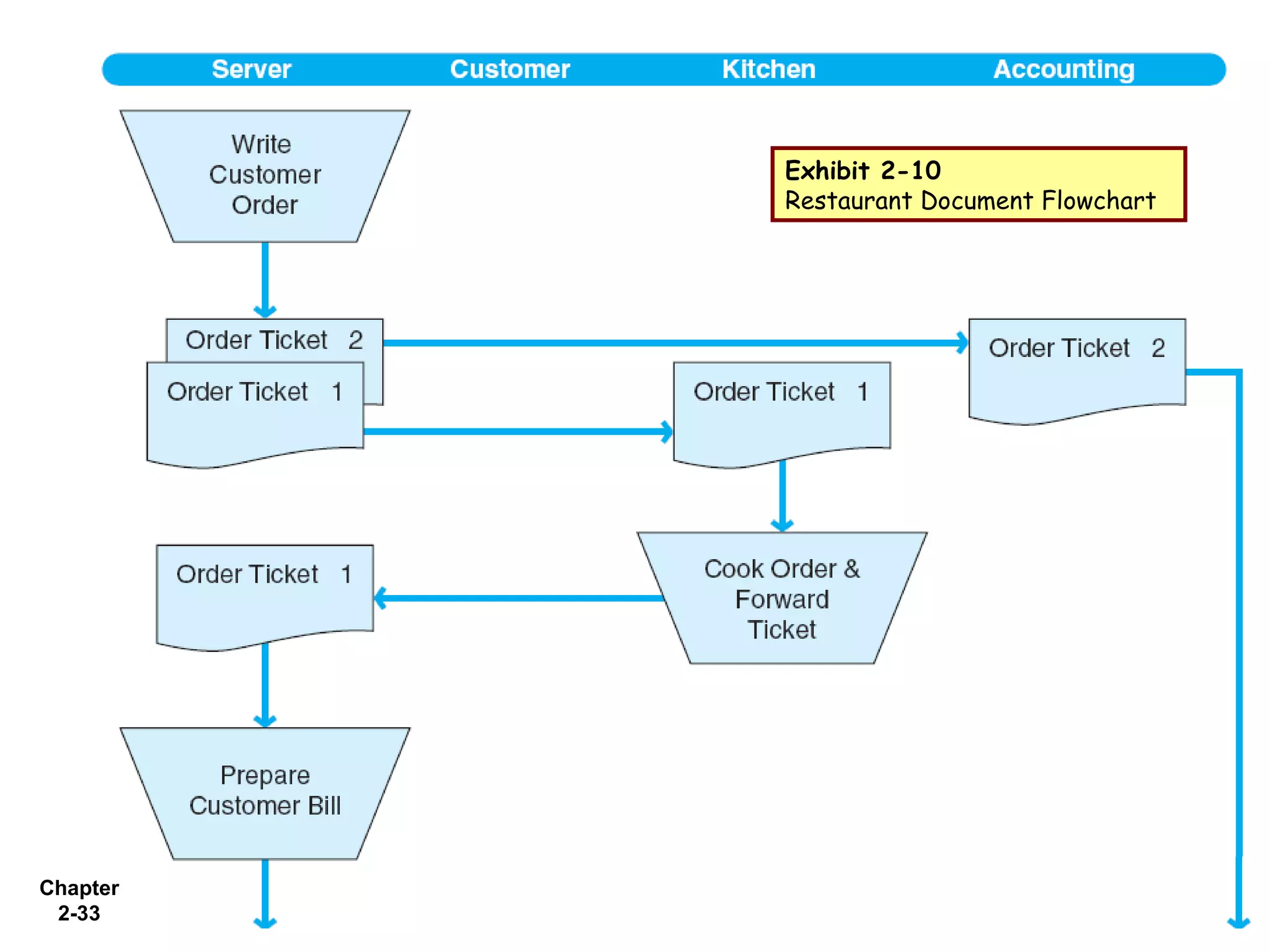

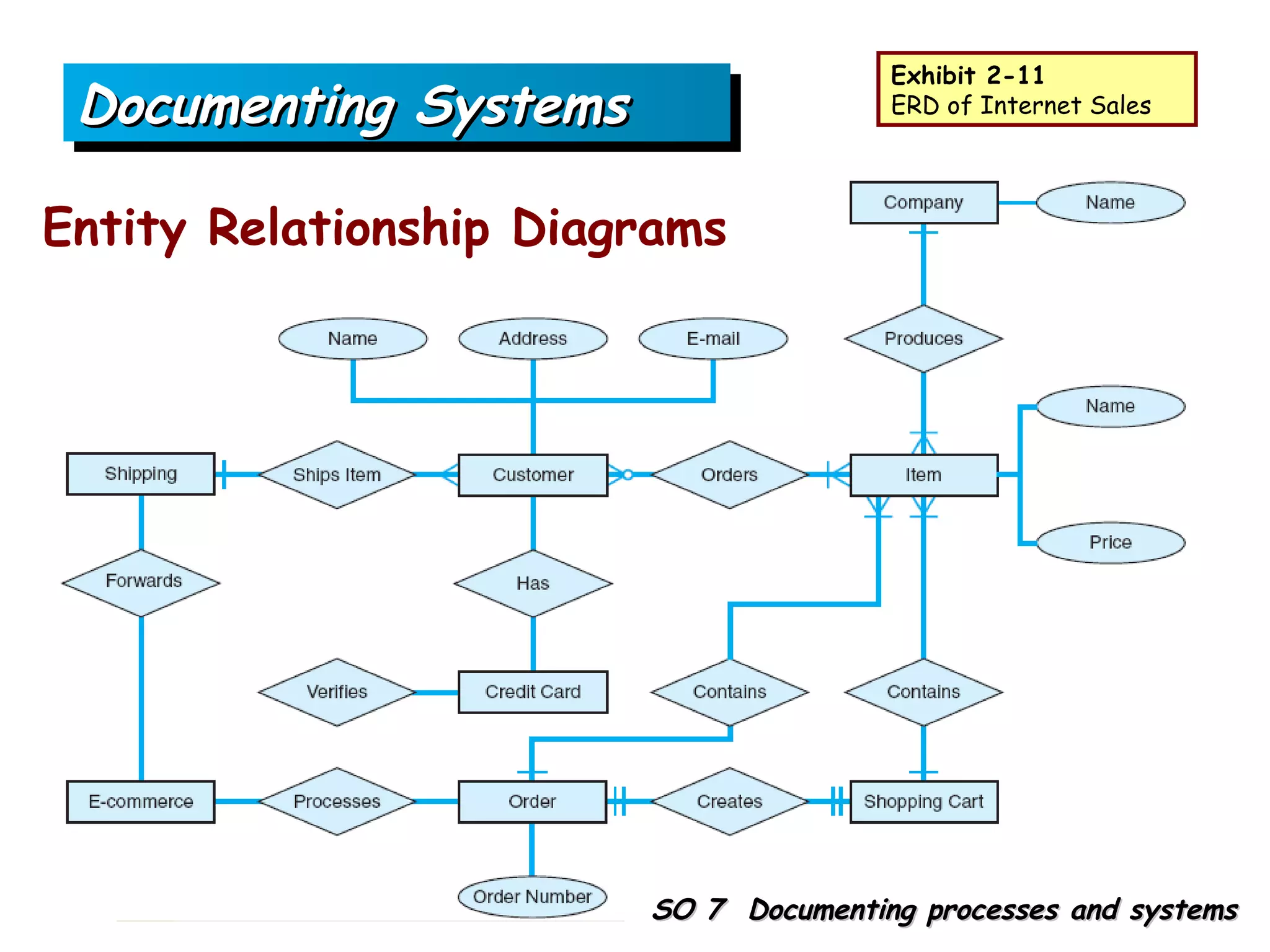

The document provides an overview of key concepts in accounting information systems including: business processes and their relationship to AIS, types of AIS (manual, legacy, modern), accounting software market segments, input and processing methods, outputs of AIS, documenting systems through various diagrams, client-server computing, and ethical considerations of AIS. It includes exhibits that illustrate these concepts through examples, diagrams, and concept check questions.

![Dividends and _dividend_policy_powerpoint_presentation[1]](https://cdn.slidesharecdn.com/ss_thumbnails/dividendsanddividendpolicypowerpointpresentation1-130929215028-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)