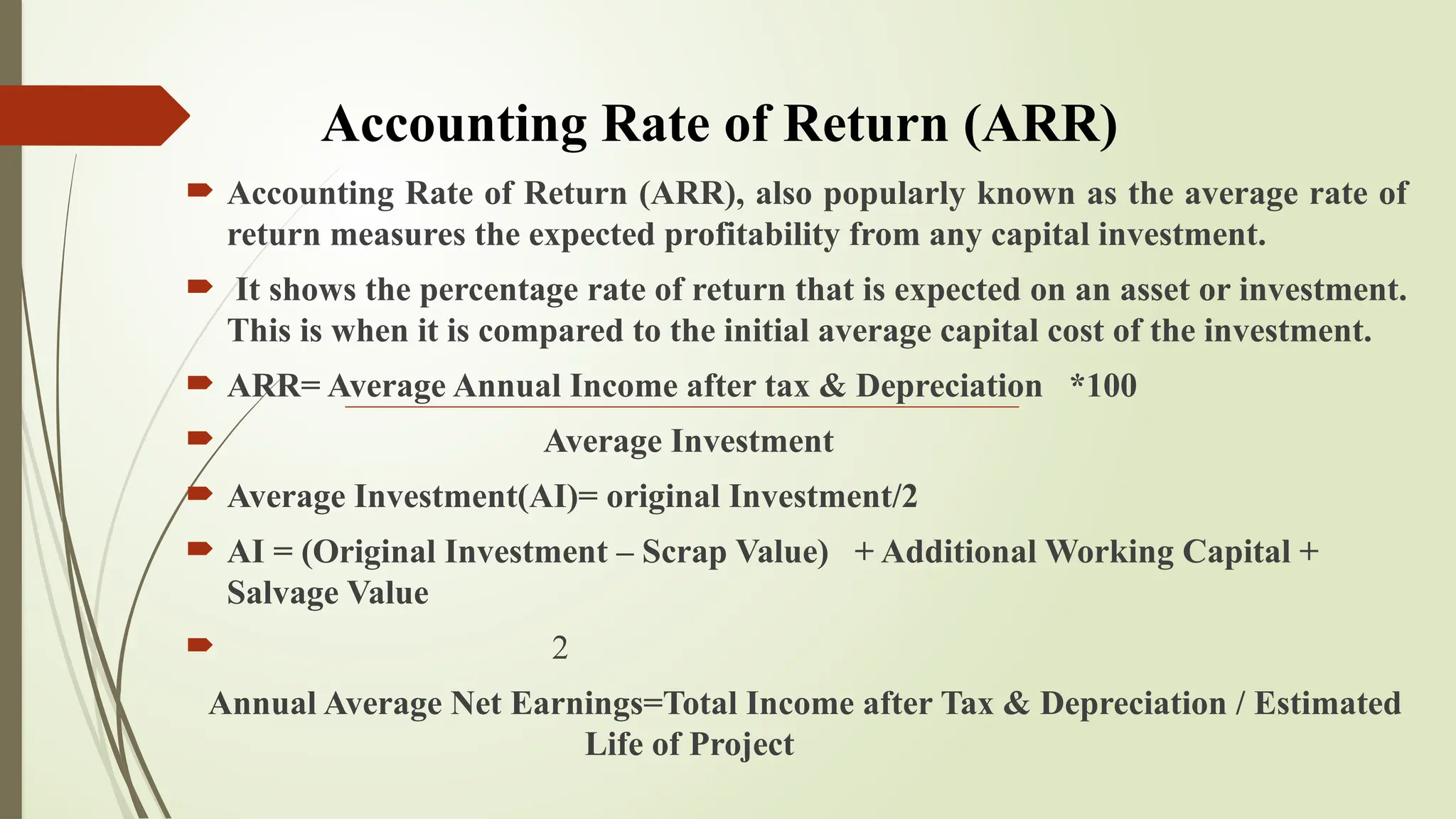

Accounting Rate ofReturn (ARR)

Accounting Rate of Return (ARR), also popularly known as the average rate of

return measures the expected profitability from any capital investment.

It shows the percentage rate of return that is expected on an asset or investment.

This is when it is compared to the initial average capital cost of the investment.

ARR= Average Annual Income after tax & Depreciation *100

Average Investment

Average Investment(AI)= original Investment/2

AI = (Original Investment – Scrap Value) + Additional Working Capital +

Salvage Value

2

Annual Average Net Earnings=Total Income after Tax & Depreciation / Estimated

Life of Project

2.

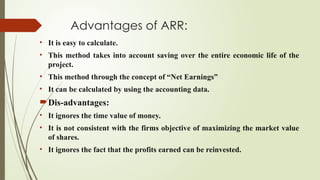

Advantages of ARR:

•It is easy to calculate.

• This method takes into account saving over the entire economic life of the

project.

• This method through the concept of “Net Earnings”

• It can be calculated by using the accounting data.

Dis-advantages:

• It ignores the time value of money.

• It is not consistent with the firms objective of maximizing the market value

of shares.

• It ignores the fact that the profits earned can be reinvested.

3.

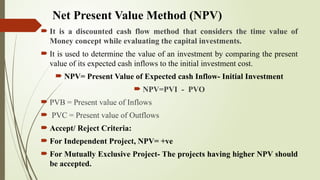

Net Present ValueMethod (NPV)

It is a discounted cash flow method that considers the time value of

Money concept while evaluating the capital investments.

It is used to determine the value of an investment by comparing the present

value of its expected cash inflows to the initial investment cost.

NPV= Present Value of Expected cash Inflow- Initial Investment

NPV=PVI - PVO

PVB = Present value of Inflows

PVC = Present value of Outflows

Accept/ Reject Criteria:

For Independent Project, NPV= +ve

For Mutually Exclusive Project- The projects having higher NPV should

be accepted.

4.

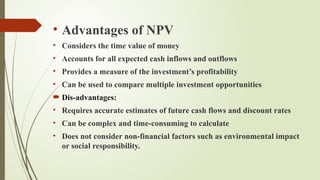

• Advantages ofNPV

• Considers the time value of money

• Accounts for all expected cash inflows and outflows

• Provides a measure of the investment’s profitability

• Can be used to compare multiple investment opportunities

Dis-advantages:

• Requires accurate estimates of future cash flows and discount rates

• Can be complex and time-consuming to calculate

• Does not consider non-financial factors such as environmental impact

or social responsibility.

5.

Profitability Index (PI)

Itis also known as Benefit Cost (B/C) ratio. It is similar to

NPV method.

It is the ratio of total present value of cash Inflows equals to

cash outflows.

PI = Total Present Value of Cash Inflow/ )Original

Investment

Accept/Reject Criteria:

Accept if PI > 1

Reject if PI < 1

6.

Internal Rate ofReturn (IRR)

It is the rate at which the sum of discounted cash Inflows equals to sum

of the discounted cash outflows.

It is the rate at which NPV of investment is Zero.

It is also known as time adjusted rate of return or trial and error

method. IRR= A + C-O/ C-D (B – A)

Where A is Discount factor of Lower trial Rate

B is discount factor of Higher Trial Rate

C is Present value of Cash inflow at Lower Trial rate

D is Present Value of Cash Inflow at Higher Trial Rate.

O is Original Investment

7.

• Advantages ofIRR

• Considers the time value of money

• It considers the profitability

• Share Holders value.

• Can be used to compare multiple investment opportunities

Dis-advantages:

• Difficult to understand.

• Can be complex and time-consuming to calculate

Based on Assumptions

8.

Accept/Reject Criteria

Accept ifIRR is higher or equal to minimum required

rate of return. The minimum rate of return is also known

as cut off rate or firms cost of capital.

Rejected if IRR < Minimum rate of return

Accepted of IRR > Minimum rate of return

For two or more projects

Higher IRR would be prefereed.