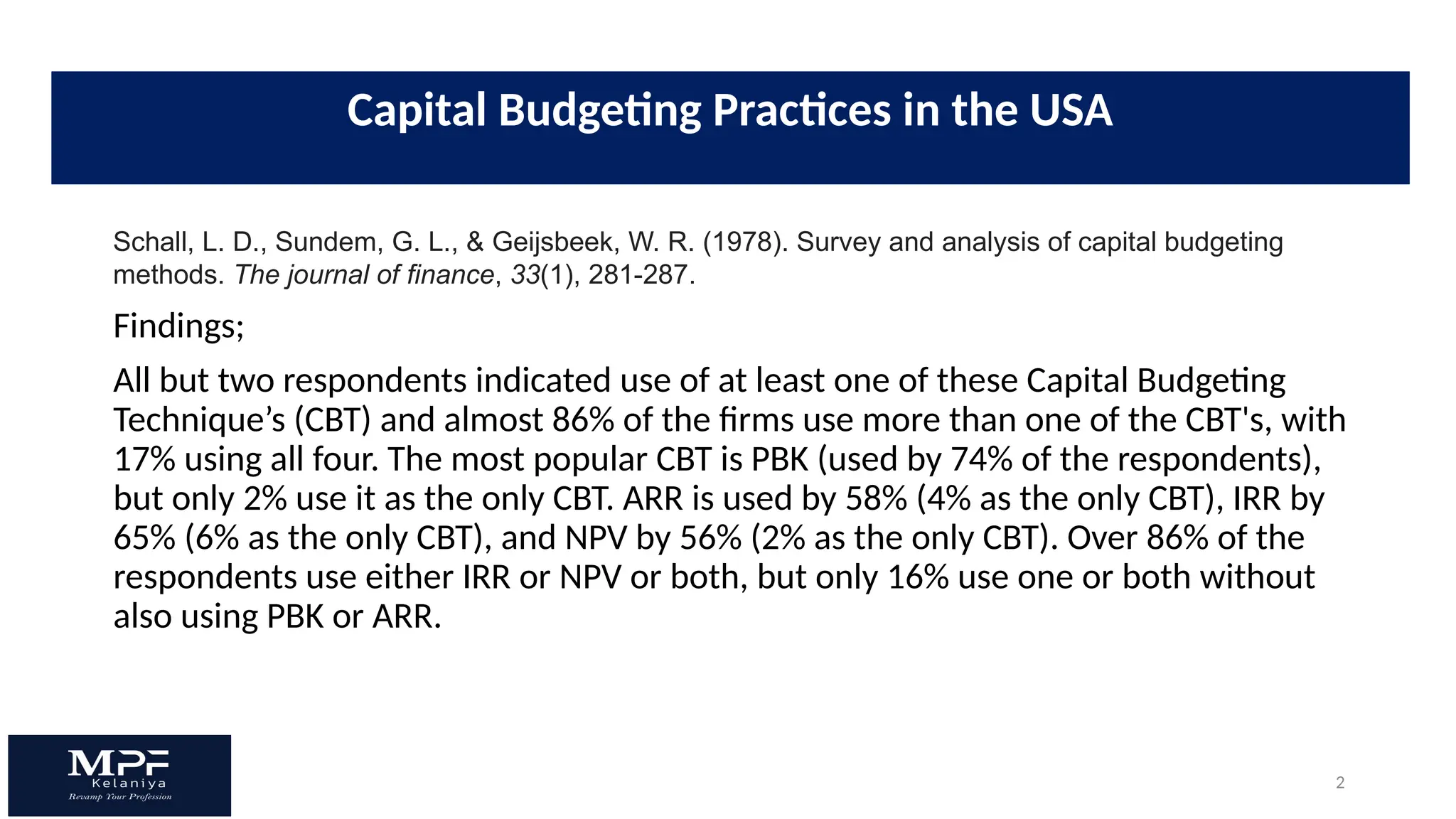

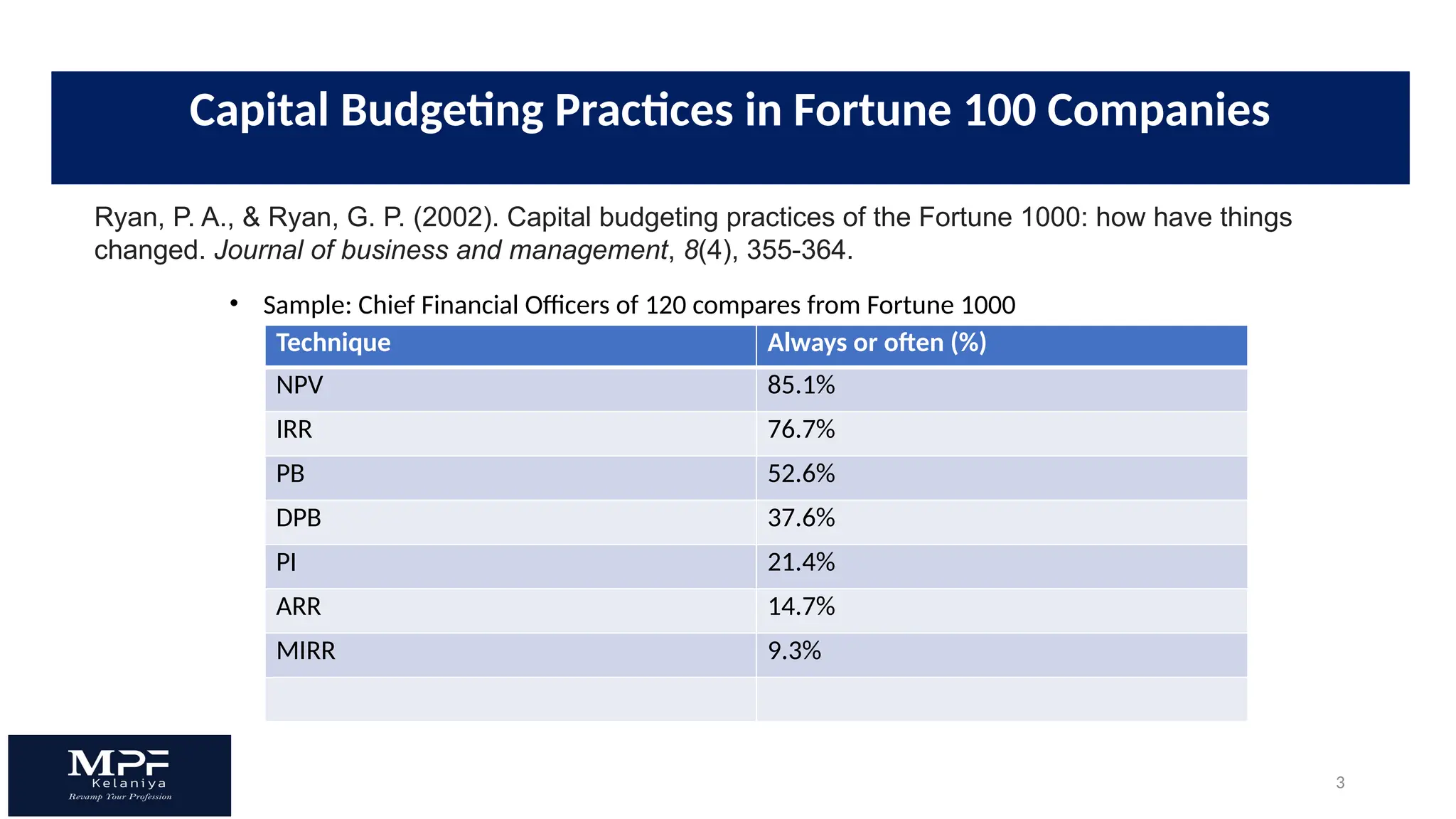

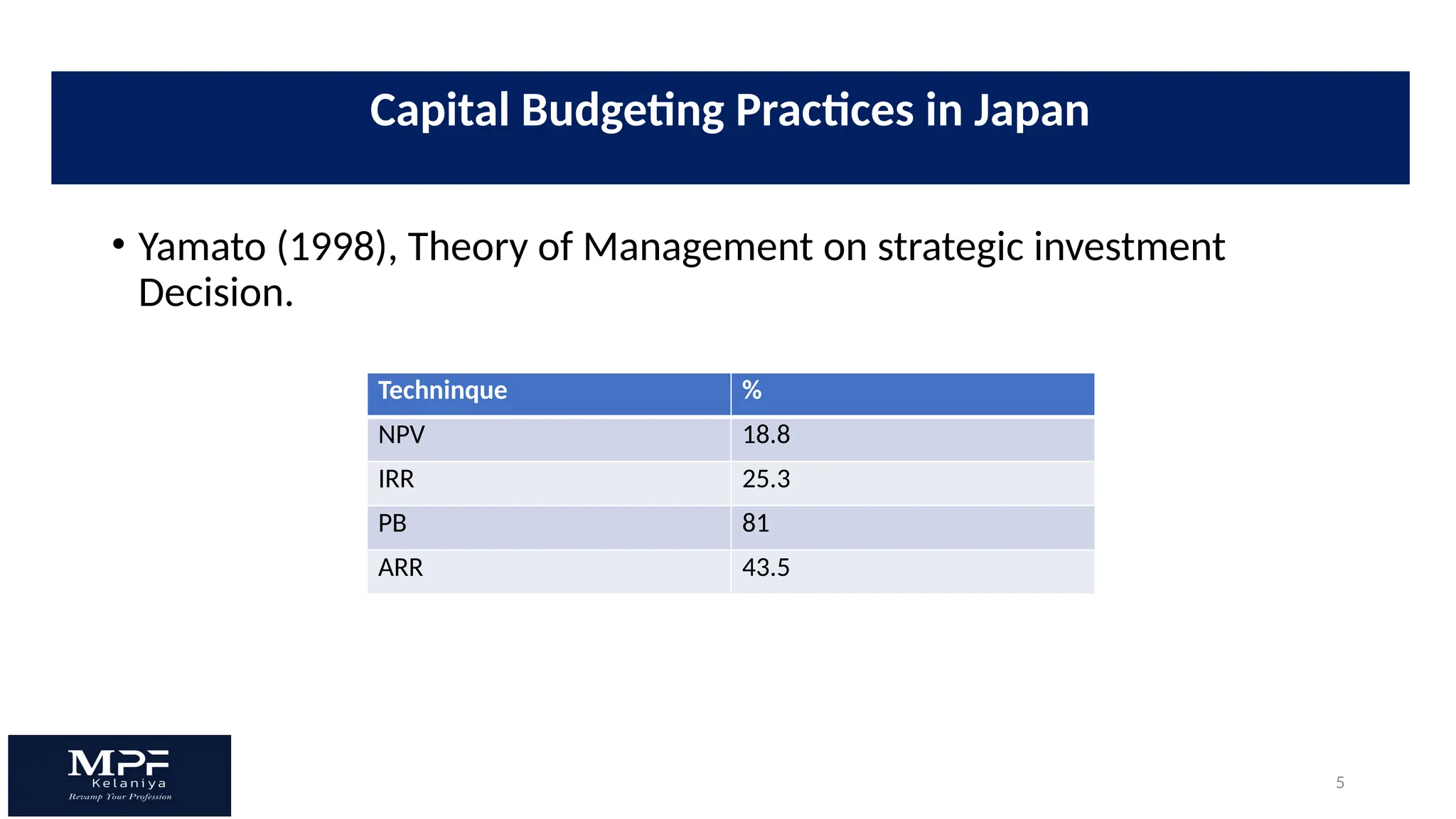

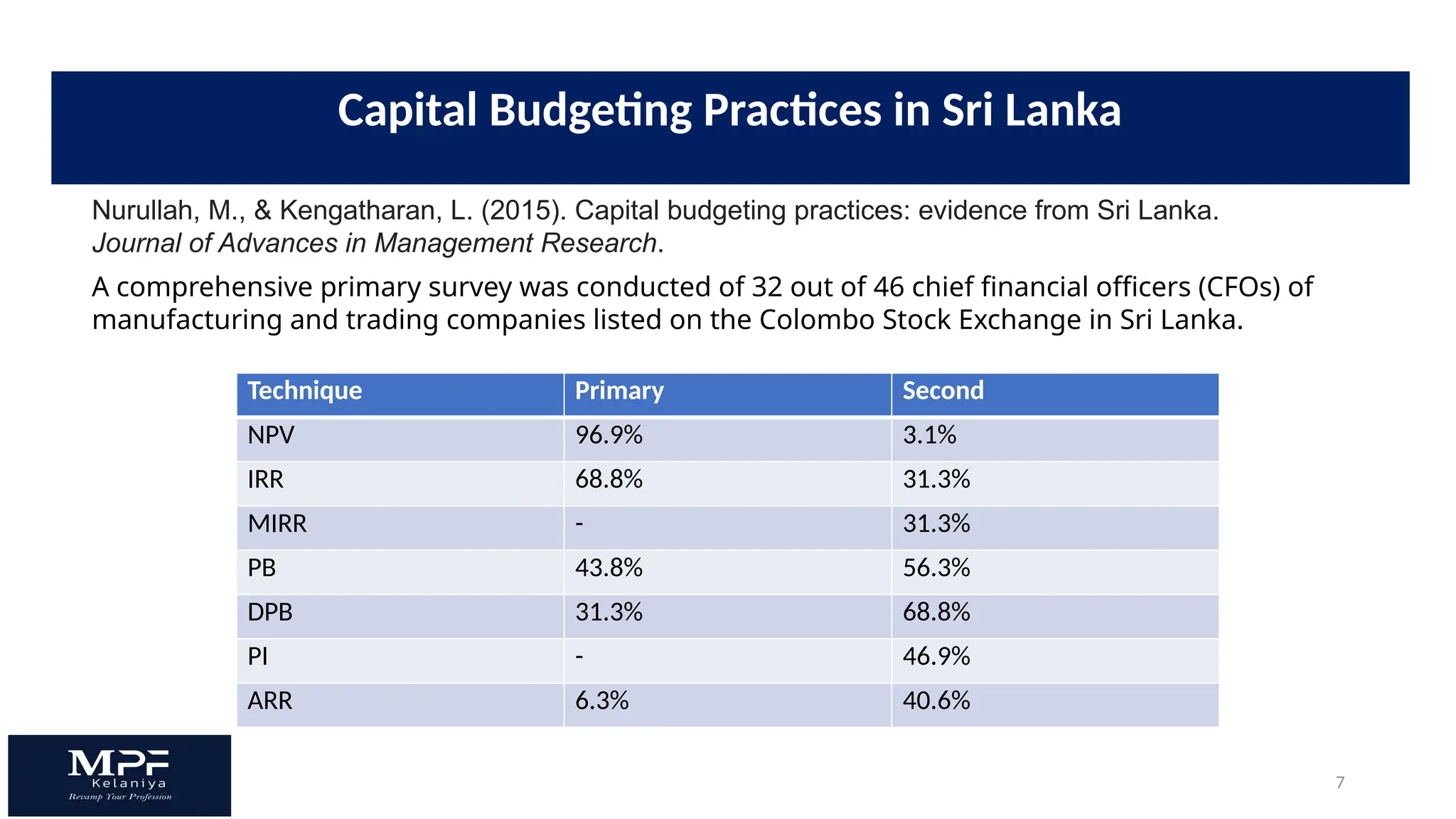

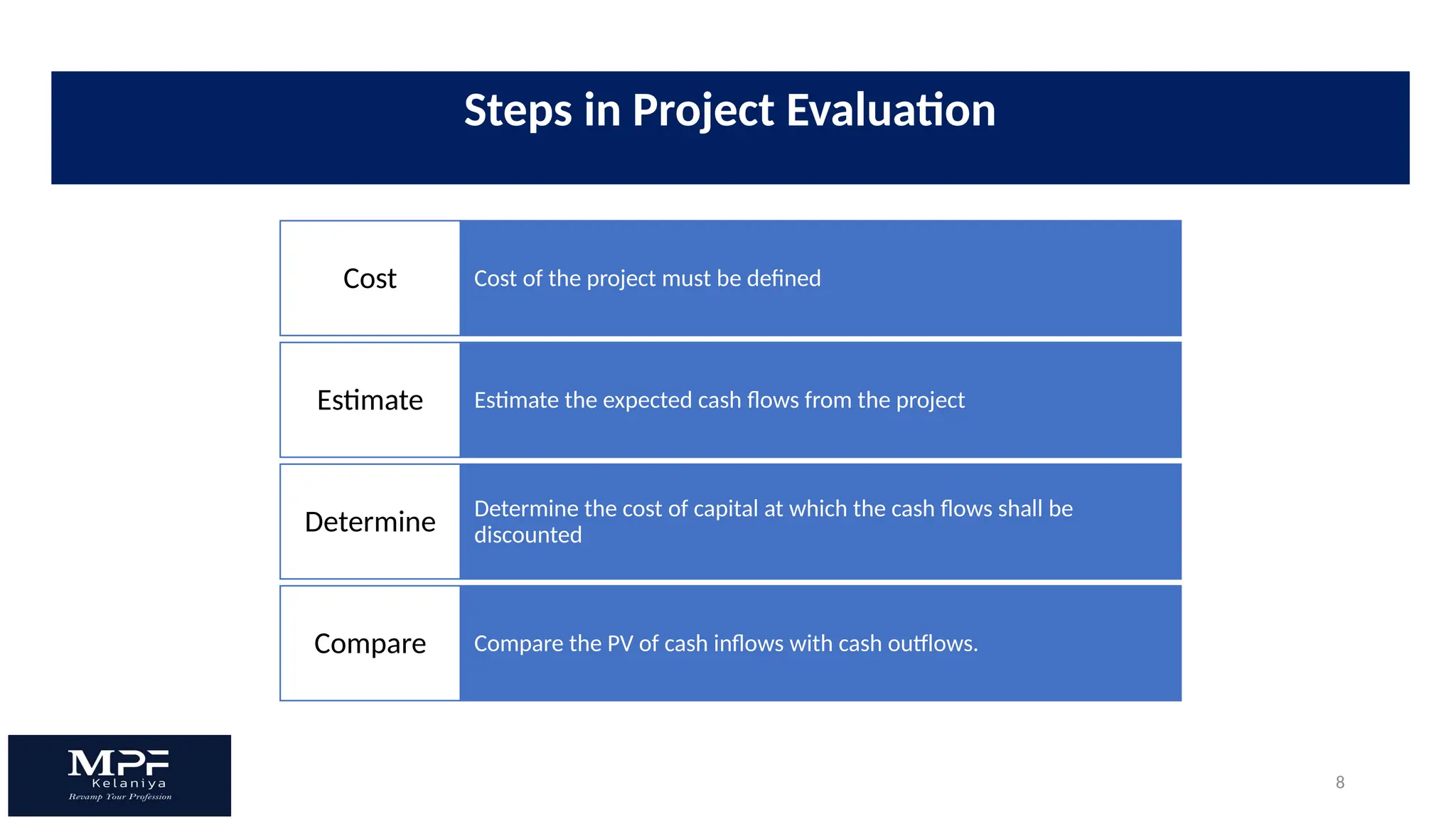

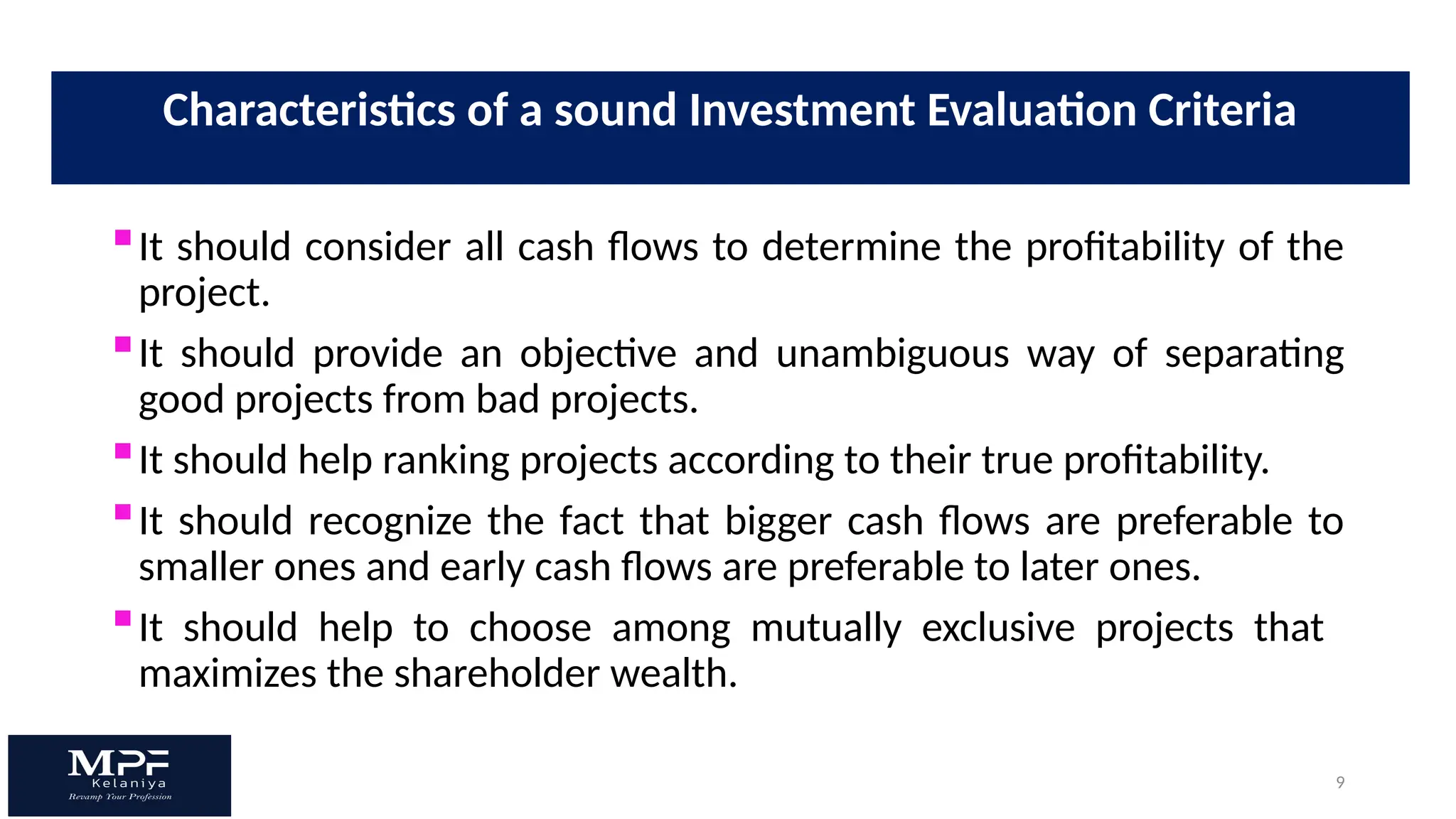

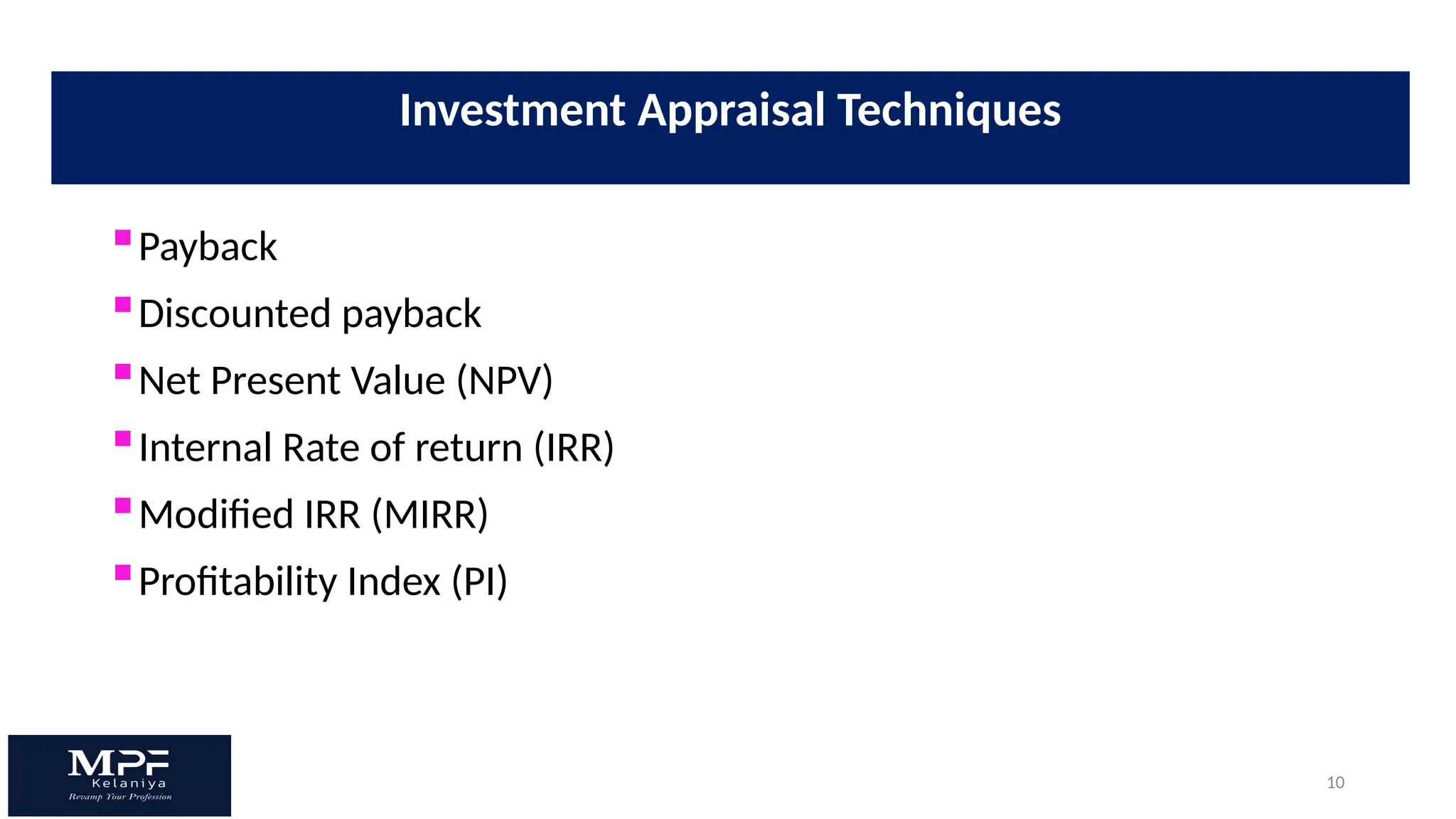

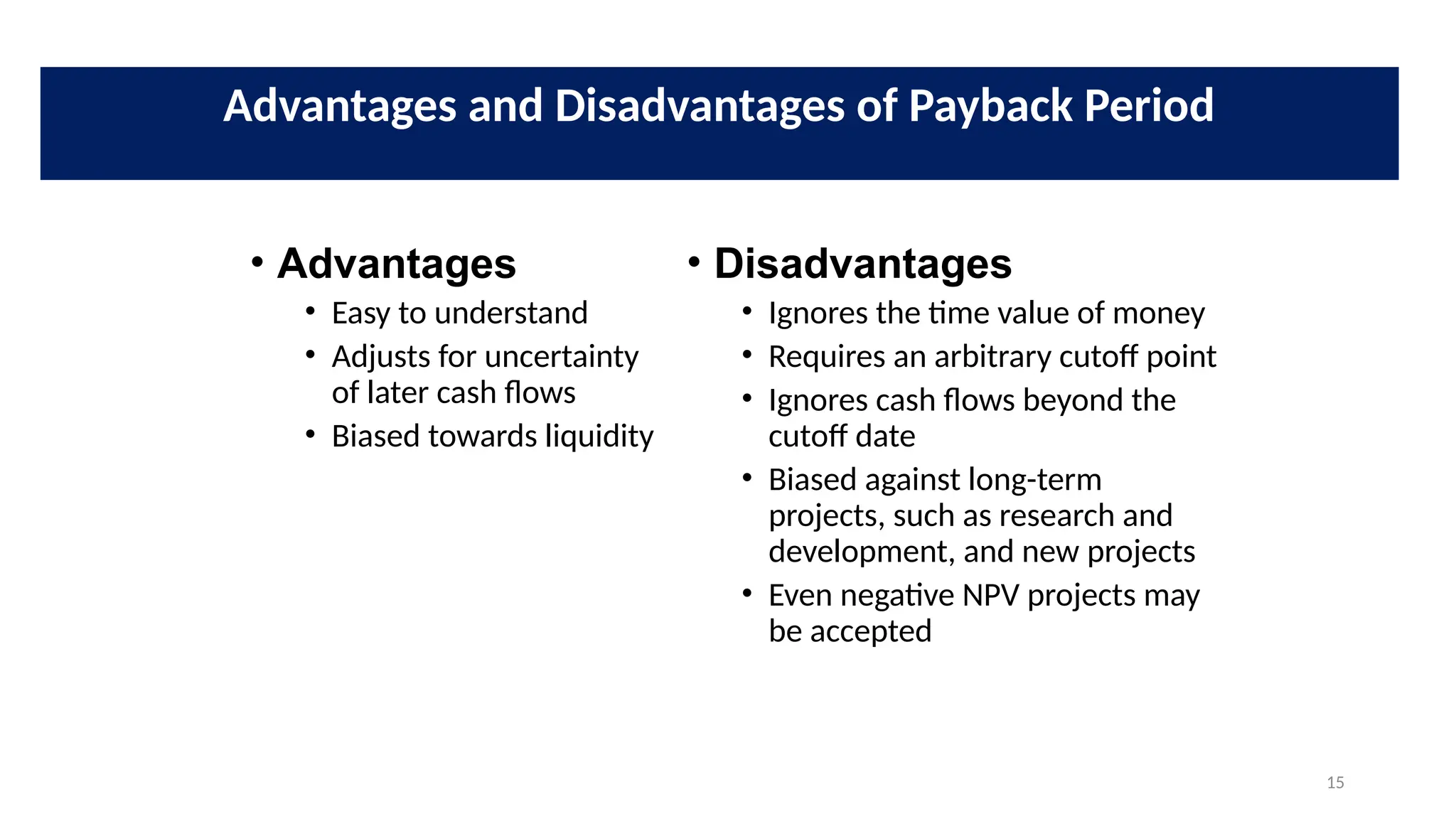

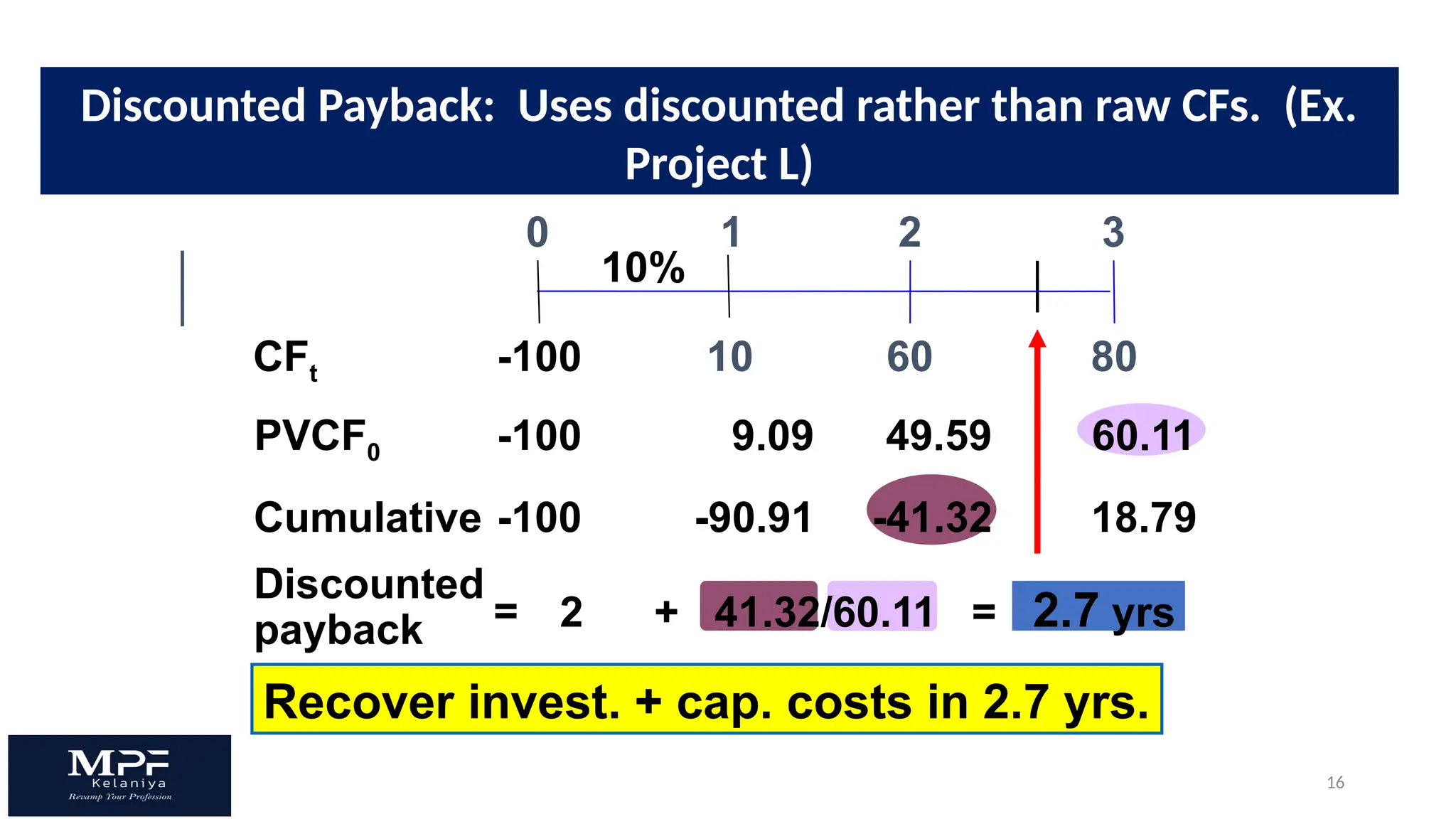

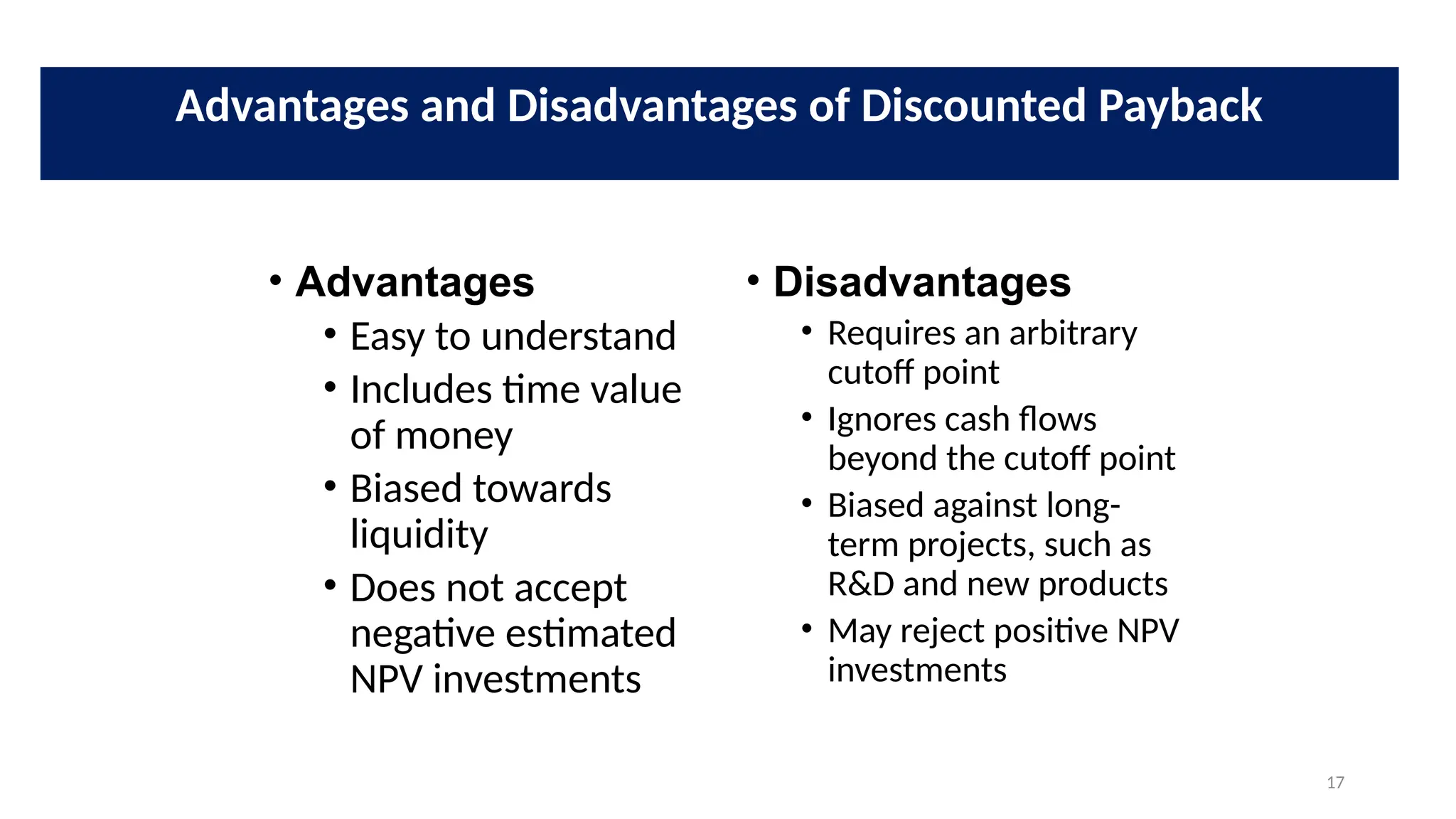

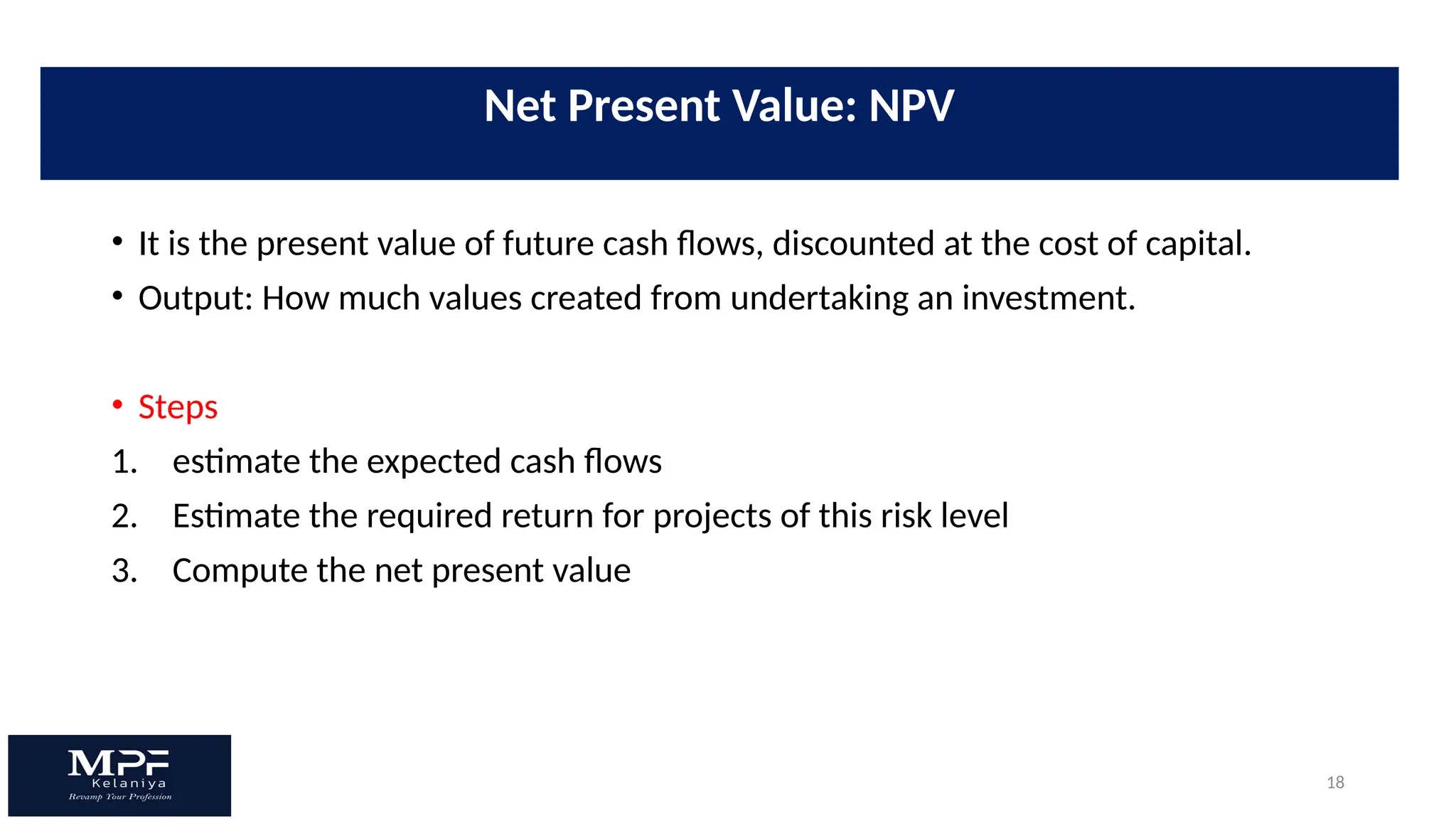

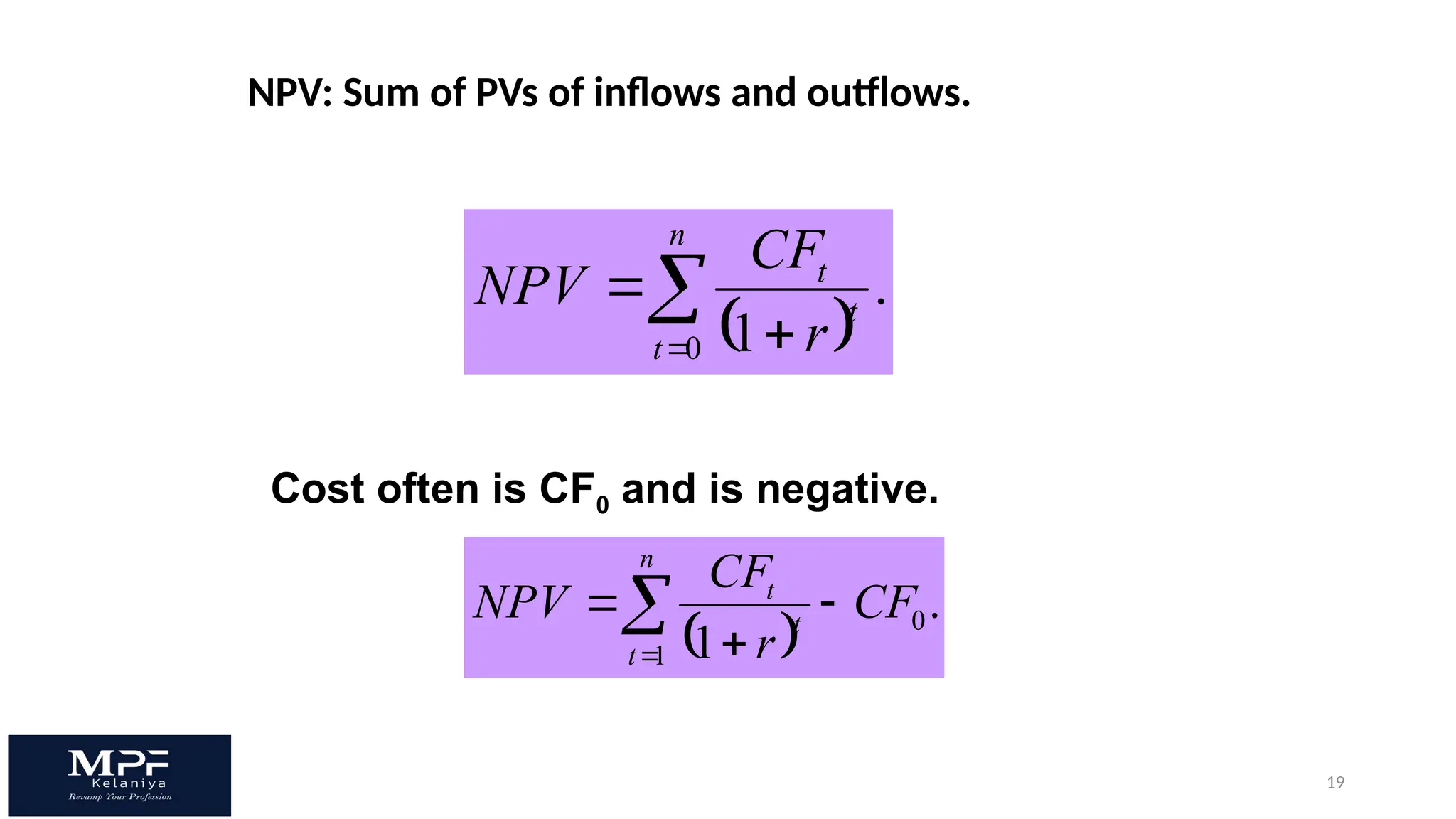

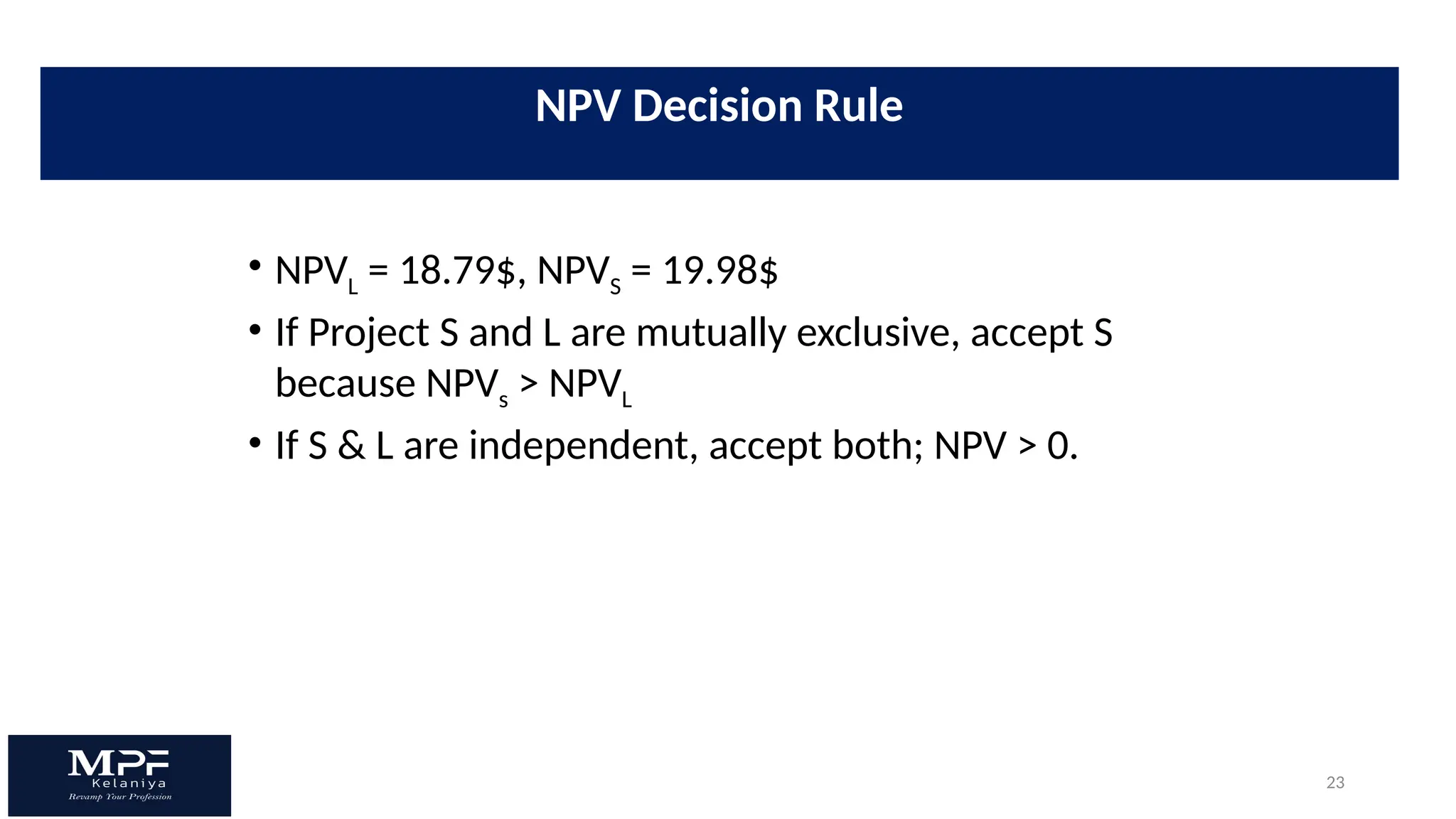

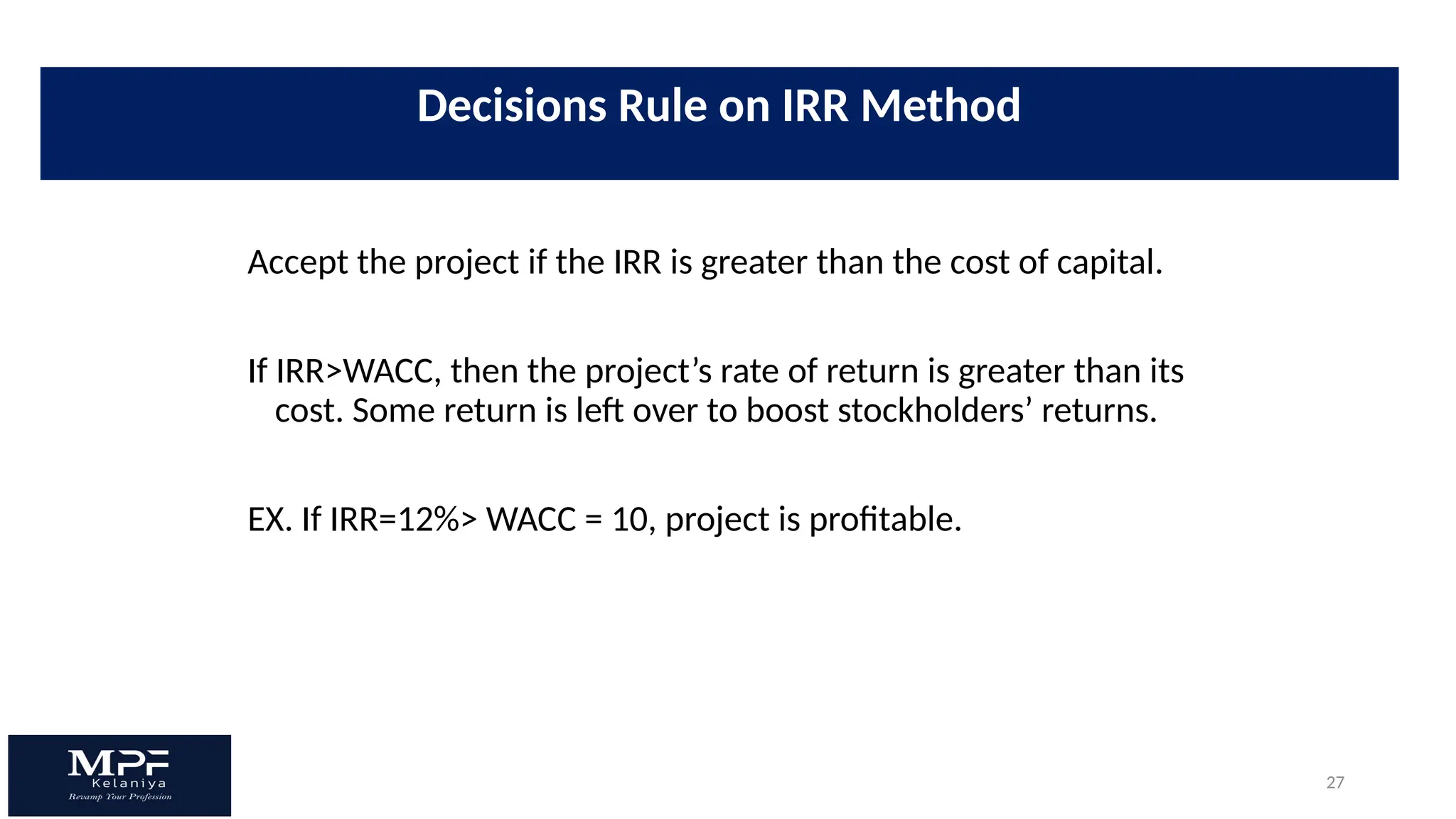

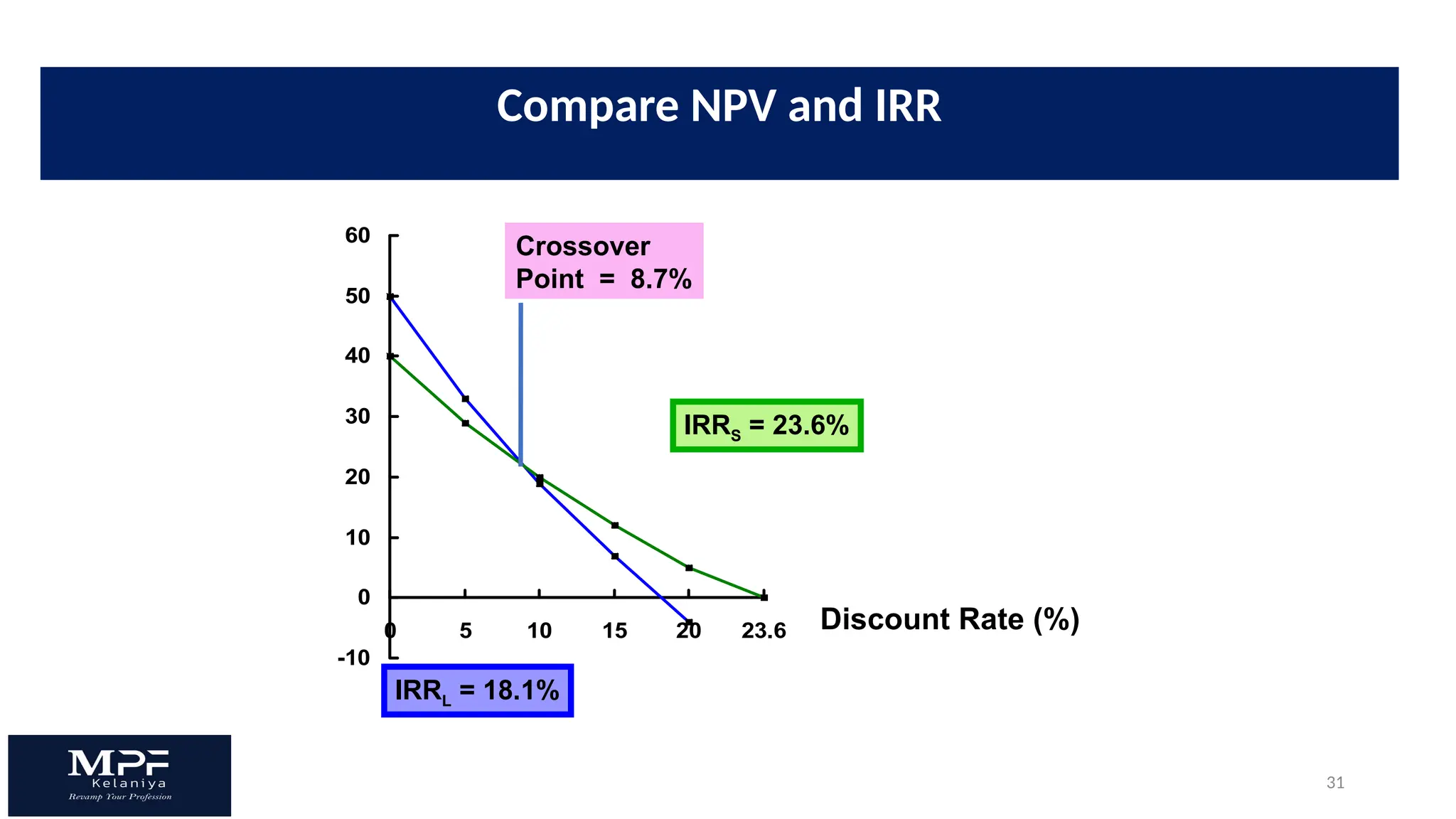

The document discusses capital budgeting practices in different countries, highlighting the usage of various techniques such as NPV, IRR, and ARR among firms. A majority of respondents utilize multiple techniques, with NPV and IRR being the most favored in corporate finance decision-making. It also details the advantages and disadvantages of different capital budgeting methods and emphasizes the importance of sound investment evaluation criteria.

![5) capital_budgeting_(1)_-(2)[1].ppt.pdf](https://cdn.slidesharecdn.com/ss_thumbnails/5capitalbudgeting121-250323135834-146732f6-thumbnail.jpg?width=640&height=640&fit=bounds)