Downloaded 132 times

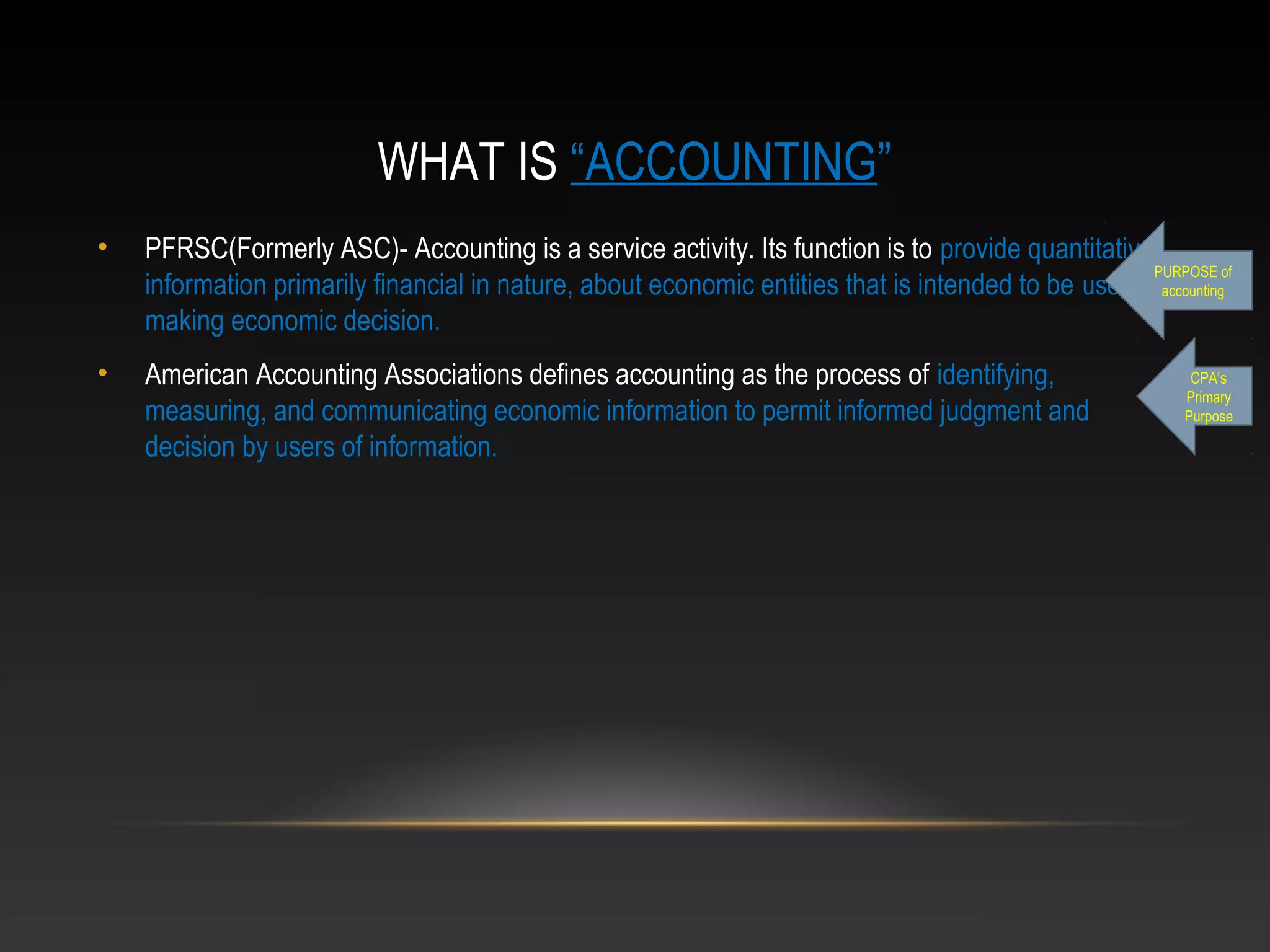

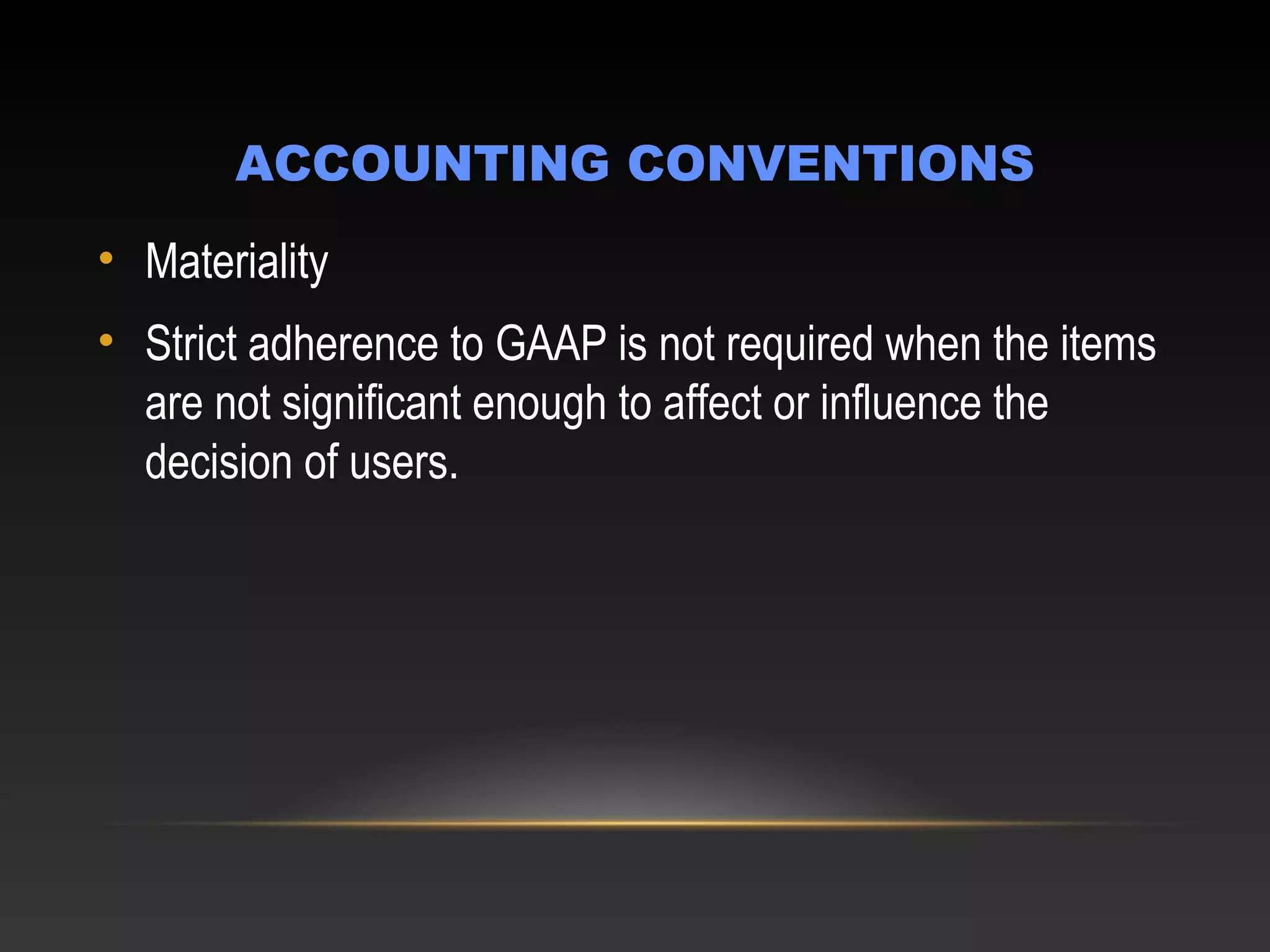

This document provides an overview of accounting as an information system. It discusses key topics such as the definitions of accounting and information systems, the differences between financial and management accounting, the users of accounting information, and the accounting cycle. It also covers accounting principles, concepts, and conventions like accrual, going concern, consistency and conservatism. The purpose of accounting is to provide quantitative financial information to help users make informed economic decisions. Accounting acts as an information system that collects, processes, and communicates useful data to both internal and external parties.

![MEFA_UNIT-IV_Part-1[1].pptx kkkkkkkkkkkkkkkkkkkkkkk](https://cdn.slidesharecdn.com/ss_thumbnails/mefaunit-ivpart-11-250504093650-39e41996-thumbnail.jpg?width=640&height=640&fit=bounds)