Download to read offline

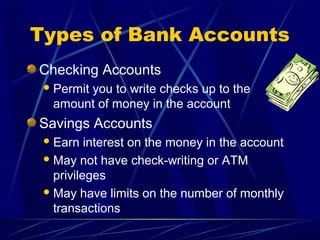

Bank accounts provide essential services for managing money. There are several types of accounts like checking, savings, and money market accounts. Checking accounts allow writing checks and debit card use, while savings accounts earn interest but have limits on transactions. It's important to choose a bank based on location, fees, and account features. Maintaining good records and being aware of fraud prevention helps manage accounts responsibly.