Recommended

Recommended

More Related Content

Similar to Balance SheetTrevose Fitness Center Balance Sheet (numbers are in .docx

Similar to Balance SheetTrevose Fitness Center Balance Sheet (numbers are in .docx (20)

More from ikirkton

More from ikirkton (20)

Recently uploaded

Recently uploaded (20)

Balance SheetTrevose Fitness Center Balance Sheet (numbers are in .docx

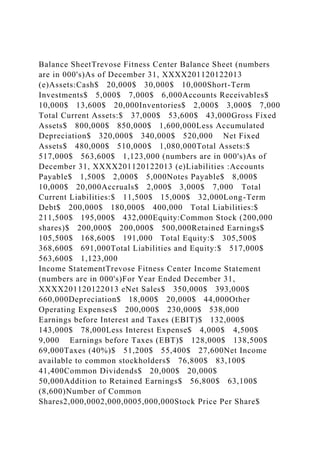

- 1. Balance SheetTrevose Fitness Center Balance Sheet (numbers are in 000's)As of December 31, XXXX201120122013 (e)Assets:Cash$ 20,000$ 30,000$ 10,000Short-Term Investments$ 5,000$ 7,000$ 6,000Accounts Receivables$ 10,000$ 13,600$ 20,000Inventories$ 2,000$ 3,000$ 7,000 Total Current Assets:$ 37,000$ 53,600$ 43,000Gross Fixed Assets$ 800,000$ 850,000$ 1,600,000Less Accumulated Depreciation$ 320,000$ 340,000$ 520,000 Net Fixed Assets$ 480,000$ 510,000$ 1,080,000Total Assets:$ 517,000$ 563,600$ 1,123,000 (numbers are in 000's)As of December 31, XXXX201120122013 (e)Liabilities :Accounts Payable$ 1,500$ 2,000$ 5,000Notes Payable$ 8,000$ 10,000$ 20,000Accruals$ 2,000$ 3,000$ 7,000 Total Current Liabilities:$ 11,500$ 15,000$ 32,000Long-Term Debt$ 200,000$ 180,000$ 400,000 Total Liabilities:$ 211,500$ 195,000$ 432,000Equity:Common Stock (200,000 shares)$ 200,000$ 200,000$ 500,000Retained Earnings$ 105,500$ 168,600$ 191,000 Total Equity:$ 305,500$ 368,600$ 691,000Total Liabilities and Equity:$ 517,000$ 563,600$ 1,123,000 Income StatementTrevose Fitness Center Income Statement (numbers are in 000's)For Year Ended December 31, XXXX201120122013 eNet Sales$ 350,000$ 393,000$ 660,000Depreciation$ 18,000$ 20,000$ 44,000Other Operating Expenses$ 200,000$ 230,000$ 538,000 Earnings before Interest and Taxes (EBIT)$ 132,000$ 143,000$ 78,000Less Interest Expense$ 4,000$ 4,500$ 9,000 Earnings before Taxes (EBT)$ 128,000$ 138,500$ 69,000Taxes (40%)$ 51,200$ 55,400$ 27,600Net Income available to common stockholders$ 76,800$ 83,100$ 41,400Common Dividends$ 20,000$ 20,000$ 50,000Addition to Retained Earnings$ 56,800$ 63,100$ (8,600)Number of Common Shares2,000,0002,000,0005,000,000Stock Price Per Share$

- 2. 150.00$ 180.00Earnings Per Share$ 38.40$ 41.55$ 8.28 Financial RatiosFinanicial Ratios for Trevose Fitness CenterLiquidity Ratios:201120122013 (e)Industry AverageCurrent3.223.571.342Quick3.043.371.131.8Asset Management Ratios:201120122013 (e)Industry AverageTotal Asset Turnover0.680.700.590.5DSO10.43 Days12.63 Days11.06 Days30 DaysDebt Management Ratios:201120122013 (e)Industry AverageDebt to Equity0.680.520.610.5Times Interest Earned33.0031.788.6710Profitabiltiy Ratios:201120122013 (e)Industry AverageNet Profit Margin0.220.210.060.1Return on Equity (ROE)0.250.230.060.12Market Value Ratio:201120122013 (e)Industry AveragePrice/Earnings (P/E)3.914.333 TVMPresent Value =5,000,000Compounding Rate =Monthly12Annuity Payments =0Interest Rate per Year8Number of Years5Future Value$7,449,228.54 in 000Assets:201120122013 (e)0Libilities :201120122013 (e)Cash$ 20,000,000.00$ 30,000,000.00$ 10,000,000.00$ - 0Accounts Payable$ 1,500,000.00$ 2,000,000.00$ 5,000,000.00Short-Term Investments$ 5,000,000.00$ 7,000,000.00$ 6,000,000.00Notes Payable$ 8,000,000.00$ 10,000,000.00$ 20,000,000.00Accounts Receivables$ 10,000,000.00$ 13,600,000.00$ 20,000,000.00Accurals$ 2,000,000.00$ 3,000,000.00$ 7,000,000.00Inventories$ 2,000,000.00$ 3,000,000.00$ 7,000,000.00 Total Current Liabilities:$ 11,500,000.00$ 15,000,000.00$ 32,000,000.00 Total Current Assets:$ 37,000,000.00$ 53,600,000.00$ 43,000,000.00Long-Term Debt$ 200,000,000.00$ 180,000,000.00$ 400,000,000.00Gross Fixed Assets$ 800,000,000.00$ 850,000,000.00$ 1,600,000,000.00 Total Liabilities:$ 211,500,000.00$ 195,000,000.00$ 432,000,000.00Less Accumulated Depreciation$ 320,000,000.00$ 340,000,000.00$ 520,000,000.00Equity: Net Fixed Assets$ 480,000,000.00$ 510,000,000.00$ 1,080,000,000.00Common Stock (200,000 shares)$ 200,000,000.00$ 200,000,000.00$ 500,000,000.00Total

- 3. Assets:$ 517,000,000.00$ 563,600,000.00$ 1,123,000,000.00Retained Earnings$ 105,500,000.00$ 168,600,000.00$ 191,000,000.00 Total Equity:$ 305,500,000.00$ 368,600,000.00$ 691,000,000.00Total Liabilities and Equity:$ 517,000,000.00$ 563,600,000.00$ 1,123,000,000.00Income Statement (numbers are in 000's)201120122013 eNet Sales$ 350,000,000.00$ 393,000,000.00$ 660,000,000.00Depreciation$ 18,000,000.00$ 20,000,000.00$ 44,000,000.00Other Operating Expenses$ 200,000,000.00$ 230,000,000.00$ 538,000,000.00 Earnings before Interest and Taxes (EBIT)$ 132,000,000.00$ 143,000,000.00$ 78,000,000.00Less Interest $ 4,000,000.00$ 4,500,000.00$ 9,000,000.00 Earnings before Taxes (EBT)$ 128,000,000.00$ 138,500,000.00$ 69,000,000.00Taxes (40%)$ 51,200,000.00$ 55,400,000.00$ 27,600,000.00Net Income available to common stockholders$ 76,800,000.00$ 83,100,000.00$ 41,400,000.00Common Dividends$ 20,000,000.00$ 20,000,000.00$ 50,000,000.00Addition to Retained Earnings$ 56,800,000.00$ 63,100,000.00$ (8,600,000.00)Number of Common Shares2,000,0002,000,0005,000,000Stock Price Per Share$ 150.00$ 180.00?Earnings Per Share$ 38.40$ 41.55$ 8.28 Sheet1Balance Sheet (numbers are in 000's)As of December 31, XXXXBalance Sheet (numbers are in 000's)As of December 31, XXXX201120122013 (e)201120122013 (e)Assets:Libilities :Cash$ 20,000$ 30,000$ 10,000Accounts Payable$ 1,500$ 2,000$ 5,000Short-Term Investments$ 5,000$ 7,000$ 6,000Notes Payable$ 8,000$ 10,000$ 20,000Accounts Receivables$ 10,000$ 13,600$ 20,000Accurals$ 2,000$ 3,000$ 7,000Inventories$ 2,000$ 3,000$ 7,000 Total Current Liabilities:$ 11,500$ 15,000$ 32,000 Total Current Assets:$ 37,000$ 53,600$ 43,000Long-Term Debt$ 200,000$ 180,000$ 400,000Gross Fixed Assets$ 800,000$ 850,000$ 1,600,000 Total Liabilities:$ 211,500$ 195,000$ 432,000Less Accumulated Depreciation$ 320,000$ 340,000$ 520,000 Net Fixed Assets$ 480,000$ 510,000$

- 4. 1,080,000Equity:Total Assets:$ 517,000$ 563,600$ 1,123,000Common Stock (200,000 shares)$ 200,000$ 200,000$ 500,000Retained Earnings$ 105,500$ 168,600$ 191,000 Total Equity:$ 305,500$ 368,600$ 691,000Total Liabilities and Equity:$ 517,000$ 563,600$ 1,123,000For Year EndedIncome Statement (numbers are in 000's)201120122013 eNet Sales$ 350,000$ 393,000$ 660,000Depreciation$ 18,000$ 20,000$ 44,000Other Operating Expenses$ 200,000$ 230,000$ 538,000Liquidity:201120122013 (e)Industry Average Earnings before Interest and Taxes (EBIT)$ 132,000$ 143,000$ 78,000Current3.21739130433.57333333331.343752good but in est yearLess Interest $ 4,000$ 4,500$ 9,000Quick3.04347826093.37333333331.1251.8 Earnings before Taxes (EBT)$ 128,000$ 138,500$ 69,000Taxes (40%)$ 51,200$ 55,400$ 27,600Asset ManagementNet Income available to common stockholders$ 76,800$ 83,100$ 41,400Total Asset Turnover0.680.700.590.5goodDSO10.4312.6311.0630 DaysgoodCommon Dividends$ 20,000$ 20,000$ 50,000Addition to Retained Earnings$ 56,800$ 63,100$ (8,600)Debt Management RatiosNumber of Common Shares2,000,0002,000,0005,000,000Debt to Equity68%52%61%50%closeStock Price Per Share$ 150.00$ 180.00?Times Interest Earned3331.77777777788.666666666710Earnings Per Share$ 38.40$ 41.55$ 8.28Profitabiltiy RatiosNet Profit Margin22%21%6%10%good but in est yearReturn on Equity (ROE)25%23%6%12%Market Value RatioPrice/Earnings Ratio3.914.333 FIN534 Week 1 Scenario Script: The Primary Objective of the Corporation: Value Maximization Slide # Scene/Interaction

- 5. Narration Slide 1 Scene 1 · Opening scene is in a commercial format using several pictures in a gym in a slide show · Fade at end as you go into the next slide Narrator(Man): Trevose Fitness Center is more than just working out. It is an Experience! From the time you enter our facility you are taken to a whole new level of working out. We have state of the art equipment, which offers many classes to fit your needs, and provide the best in training and experience that one can have. Look at everyone having fun…….. (Break – show some people working out) Workout Woman: “I never wanted to work out. Ever since I joined Trevose Fitness Center, I don’t want to leave. They make working out fun!” Narrator(Man): Here at Trevose Fitness Center we like to say that we took the “work” out of working out and made it “Fun”! Remember, it is not fun unless you are having the TFC Experience………. We hope to see you soon…..(fade) Slide 2 Scene 2 · Joseph Jacobs is in office · Have him move around the office · Show a map of the US? · Go to next slide FIN534_1_2_Joe-1: Hi everyone. You just saw parts of our most recent commercial that is running all over the East Coast. I am Joseph Jacobs, the Chief Executive Officer at Trevose Fitness Center or better known as TFC. My family started the business about twenty years ago having a different twist to

- 6. working out. We like to say that you will have Fun, Fun, Fun until your Daddy takes TFC away………. Remember that Beach Boys song?? (Laughter) FIN534_1_2_Joe-2: Over the years we have seen our business model really take off. In the past twenty years we have also grown to one hundred Fitness Centers all on the East Coast. I have been involved with every one of the openings and am proud to say that each one is still open today. FIN534_1_2_Joe-3: During that time we have been approached by many companies about selling, but there is too much sentimental value; therefore, we do not want sell the company. However we have an opportunity to expand our operations out west and could really use your help. As you may have figured out, I am not a financial guru. A fitness guru, yes, and I like getting out there and selling the TFC brand. I leave all of the financial decisions to our expert, Don Rising. Slide 3 Scene 3 · Don Rising is in office · Show Strayer MBA banner · Show a map of the US? · Go to next slide FIN534_1_3_Don-1: Thanks Joe. Hi everyone, I am Don Rising, the Chief Financial Office,r who has been put in charge of overseeing this big expansion project by Joe. I joined TFC ten years ago as the manager of new operations after working in the financial industry for years. I was able to work my way up the ladder here at TFC largely due to the education I received at Strayer University, where I completed my MBA. GO STRAYER! FIN534_1_3_Don-2: I am not full of all the physical energy that Joe has and am more of a numbers person. So, I have the mental

- 7. energy! This expansion is huge for us and we have built a solid team to oversee it. Let me introduce you to Linda Smith, the manager of new operations. Slide 4 Scene 4 · Linda Smith · Show Strayer MBA banner · Joe comes in · Go to next slide FIN534_1_4_Linda-1: Thanks Don. Hi everyone, I am Linda Smith and also received my MBA from Strayer University. Awwwwww, I remember my school days! As Don said, I am the manager of new operations. This expansion project can help us easily double our company size, so we need to make sure that we analyze it thoroughly. During my six years at TFC, I have seen us grow, but not to this extent. Joe has selected Don, me and one other person to analyze this project. FIN534_1_4_Linda-2: Congratulations, we have selected you as an intern to help with the project! Your strong educational background with Strayer made this decision easy. So, let's put our education and know-how to practice. FIN534_1_4_Linda-3: As you can see, Joe is full of energy about this project so we want to do our best on this analysis. Over the next few weeks, we will be looking at many different areas of the financial management process to make a recommendation on the project. We will be faced with some tough decisions to make, but working together, I am sure we will reach our goal. Welcome to the Team! Slide 5 Scene 5 Review all characters · Use a slide where you show the corporate structure for this project

- 8. · Put their pictures and titles underneath them · Go to next slide Animation – list all characters here · Joe – CEO · Don – CFO · Linda – New Operations · Intern – Expansion Project FIN534_1_5_Linda-1: Looks like you have met everyone involved in this effort. To recap, Joe is our CEO. Don is our CFO who reports to Joe. And I am the manager of new operations who is overseeing this project with you. Slide 6 Scene 6 Check Point: Why is TFC looking at expanding? (select best choice) A) To be the biggest fitness center in the United States Answer: Nice try but not correct. Businesses don’t expand to because they want to be the biggest. There is a better underlying meaning B) To be able to attract new customers Answer: Good choice but not correct. While expanding will attract new customers, business look at expanding for internal and external reasons. C) To build shareholder wealth

- 9. Answer: Correct. When businesses look at projects, they are concerned with the primary well-being of the company and its investors. Projects that create positive cash for a company increases its bottom line and overall shareholder wealth. Slide 7 Scene 7 Linda gives an overview of company and what to look for in value maximization · · Standing in her office · Discusses Value Maximization FIN534_1_7_Linda-1: Now that you got to meet everyone, let’s roll up our sleeves and get started on this project. FIN534_1_7_Linda-2: We are looking into this project to maximize shareholder wealth for TFC. What do we mean by that? It can be confusing. Slide 8 Scene 8 · Linda Speaks · Standing in her office · Show two points here – Market Price and Fundamental Price · Simple Corporate Structure (top-down) · Show Market Price versus Intrinsic/Fundamental Price · Discusses Value Maximization FIN534_1_8_Linda-1: As you know, the shareholders are the ones who own the corporation…remember what you learned in in your Strayer accounting classes? Shareholders purchase stock in companies, like Trevose Fitness Center, because they want to see their investment grow or meaning that they want a return on their equity. Shareholders also vote for directors, who in turn hire managers to run the company. Here at TFC, we have a board of directors who hired Joe and Don along with other senior managers. Don hired me, which led me to suggest the

- 10. need for an intern, like you. Do you see how this cycle evolves? FIN534_1_8_Linda-2: The primary interest of the managers is shareholder wealth maximization. But that can be taken differently. You see, shareholders see the market price of the stock which is what people can pay for a share of TFC in the open market. They base their return on how high the share price goes. However, there is another price, called the intrinsic price. The intrinsic price is also called the Fundamental Price. Slide 9 Scene 9 · Linda Speaks · Have something on the screen about the intrinsic/fundamental value on screen · Discusses Value Maximization FIN534_1_9_Linda-1: So, which price is more important? Of course it is the Intrinsic Price. That is the price that is derived assuming all available information is known about a company; this is rare!. For example, if we told our competitors all of our plans, then we won’t be able to have that competitive advantage. Also, timing of company actions may show better results than we actually have. These are just a few examples of where “what you see is not really what you get.” However, this Intrinsic Price is the price that managers need to consider when they are trying to maximize shareholder wealth. You see, in order to maximize shareholder wealth you need to know everything about a company. Then, you can put a value on a company. So, managers should really be concerned with the value of a company and not its Market Price FIN534_1_9_Linda-2: As you dig deeper into your analysis of TFC, keep that in mind. Slide 10 Scene 10

- 11. · Linda Speaks · Is intrinsic value maximization good or bad for society? · Put reasons on a chart FIN534_1_10_Linda-1: Then, the question that comes up “Is intrinsic value maximization good for society?” FIN534_1_10_Linda-2: Of course, it is good. Here are some reasons. One, more people are invested in the stock market; Two, company Efficiency; And three, employee benefits. Let’s look at each one as it relates to TFC. Slide 11 Scene 11 Linda: List number 1 on the slide. · 1) More people are invested in the stock market 2) Company Efficiency 3) Employee Benefits FIN534_1_11_Linda-1: Today more and more people have a direct or indirect interest in the markets. More companies are offering defined contribution plans that invest mainly in mutual funds by employees. Also, with investing being more available now, people are investing in the markets, including stocks, bonds, money markets, mutual funds, and even exchange traded funds or ETFs. Also, many parents are starting early with tax benefit college funds. You may have heard of them. They are called section five-twenty-nine plans. The list can go on, but what to see here is more people are investing than years ago. That is a good thing for society FIN534_1_11_Linda-2: At TFC, our employees, called Crew

- 12. Builders, participate in a four-o-one k retirement plan. They are also educated on the many investment options for them to build a better financial future. Slide 12 Scene 12 Linda: List number 2 on the slide. · Linda Speaks 1) More people are invested in the stock market 2) Company Efficiency 3) Employee Benefits FIN534_1_12_Linda-1: With competition being so great companies are always looking for better ways of doing things at a lower cost. Technological enhancements or product upgrades can help the bottom line of a company. When this happens and a business starts to grow, investors and competitors take notice. The result is a benefit to society. FIN534_1_12_Linda-2: Here at TFC we are always looking at ways to improve efficiencies. We recently installed effective work out machines that have less maintenance and are more durable. We also have redesigned our facilities. Consequently, the feedback from our “Body Builders” has been very positive. By the way, our fitness members are called Body Builders… Slide 13 Scene 13 Linda: List number 3 on the slide. · Linda Speaks 1) More people are invested in the stock market 2) Company Efficiency 3) Employees Benefit FIN534_1_13_Linda-1: Growth is good. When companies grow, there is also a good chance that they will see their stock price, revenue, and employee base grow as well. TFC is a good example of that. We have expanded from one center to one hundred centers and have also added many new employees.

- 13. Business has been good but this expansion project is really making me nervous. We have to keep in mind our cash flow through this project. Slide 14 Scene 14 Checkpoint M/C – check all that applies What price should managers be focused on when running a corporation? Fundamental Price (yes) Market Price (No) Intrinsic Price (Yes) Futures Price (No) Fundamental Price – correct. Fundamental price is determined from ALL available information known for the corporation. Market Price (No) – Nice try but incorrect. Market price is what investors see but there may be some information not made available to the public that can alter the value of a corporation. Intrinsic Price (Yes) - . Intrinsic price is determined from ALL available information known for the corporation. Futures Price (No) – Nice try, but incorrect. Futures price is based on some point in time down the road and not a part of current day pricing for a corporation. Slide 15 Scene 15 · In comes Don · Laugh FIN534_1_15_Don-1: Hi Linda. Are you giving our Intern the overview on financial management? FIN534_1_15_Linda-1: Yes, Don. As a matter of fact, our next topic is to talk about the project and cash flows.

- 14. FIN534_1_15_Don-2: Did Linda tell you how nervous she gets when talking about cash flow? (Linda smiles) FIN534_1_15_Don-3: You see the way a company determines its value is “how it is able to generate cash flows now and in the future” (insert cash symbol). It is not just about today but also later on….forward thinking! The cash flows that we are talking about are the “Free Cash Flows or FCF, which can be thought of as being free to its investors and shared holders. FIN534_1_15_Linda-2: Here at TFC, we have had a lot of free cash flows………… But, this project is still making me nervous…….will we still have those free cash flows? You see, we have worked hard to build up a nice amount of cash flow for our company. However, by us undertaking a project like this, cash is going to be needed to help with the major expenses. When we put an intrinsic price on TFC, we are using projected free cash flows. If this project depletes our cash flows in the future, we are in trouble. That is what keeps me up at night…….. FIN534_1_15_Don-4: Linda, no need to worry. That is why we have our Strayer Intern, to help us evaluate the project. FIN534_1_15_Linda-3: Okay Don. But I am still nervous………… (They all laugh) Slide 16 Scene 16 · Don in room · Linda in room · Ending slide FIN534_1_16_Don-1: Linda, thanks for giving our Strayer

- 15. Intern the overview of why we are looking at the financial management side of this project. We have never done an analysis like this before, so it is an exciting time for everyone. With that, I already have a job for the both of you addressing our financial statements. And, of course, I need the results as soon as possible. FIN534_1_16_Linda-1: Thanks Don. We can’t wait to learn more about this job……. FIN534_1_16_Linda-2: Before we end for the day, let’s briefly go over some of the important aspects that I covered today. FIN534_1_16_Linda-3: We talked about what price a company looks at when trying to maximize shareholder value. We are all familiar with Market Price as it is out there for everyone to see, but it is Intrinsic or also known as Fundamental Price that needs managers' focus and ultimate attention. We also learned that current and future cash flows help determine the value of a firm. You can say that cash is the driving force behind corporate value. FIN534_1_16_Linda-4: I hope you enjoyed your first day. Don’t forget to complete your weekly discussion questions based on your learning experience today.