Downloaded 43 times

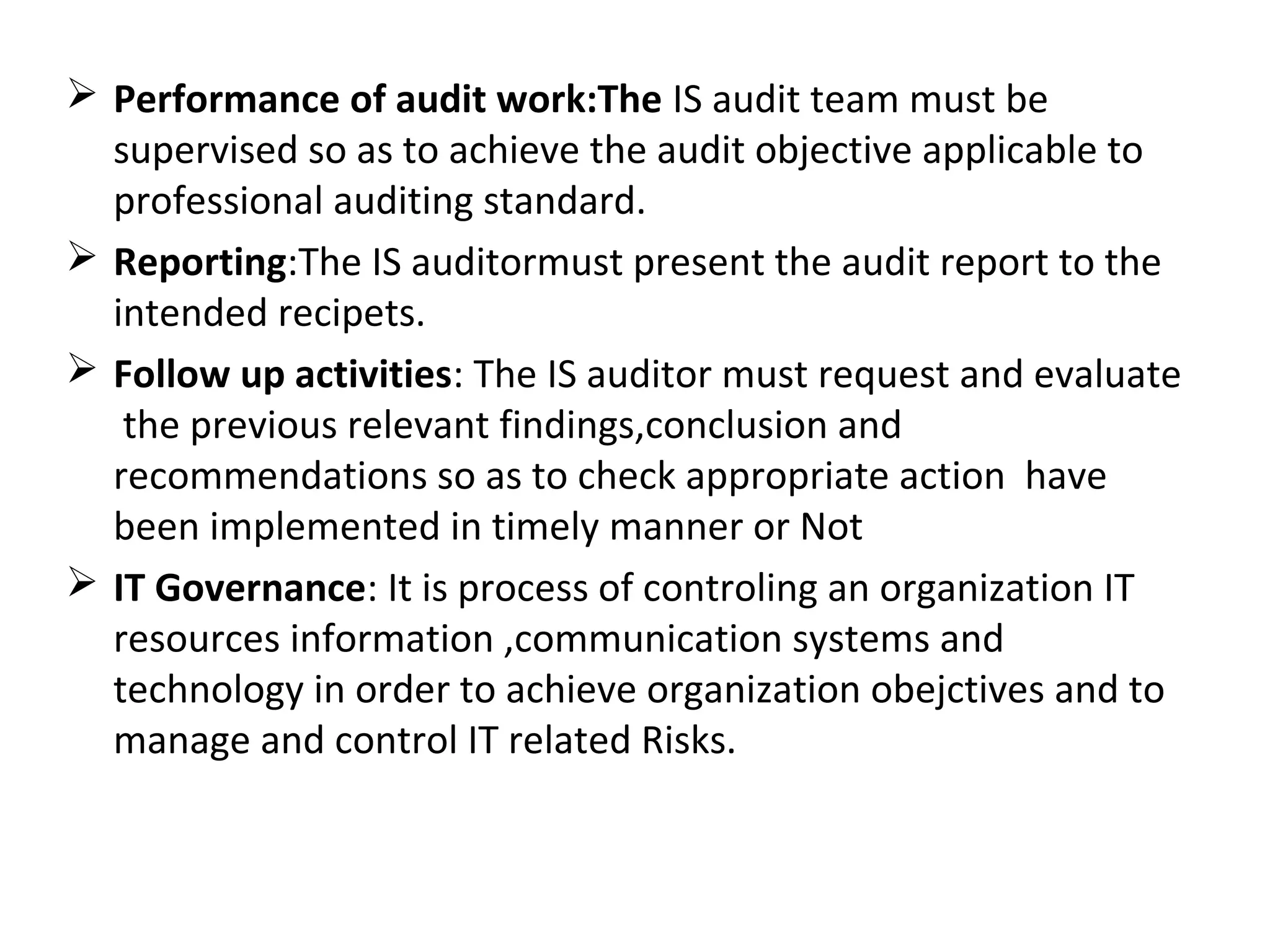

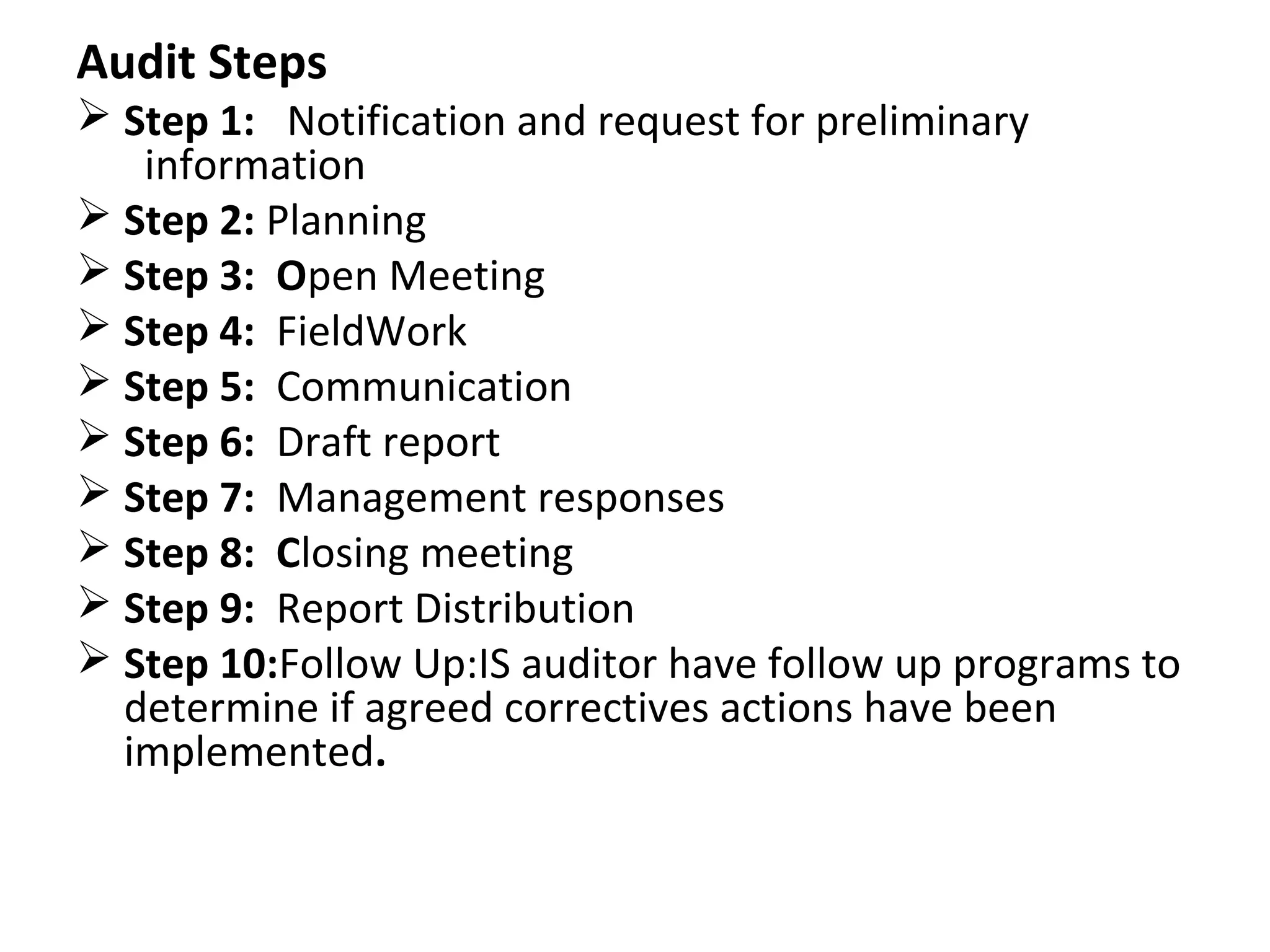

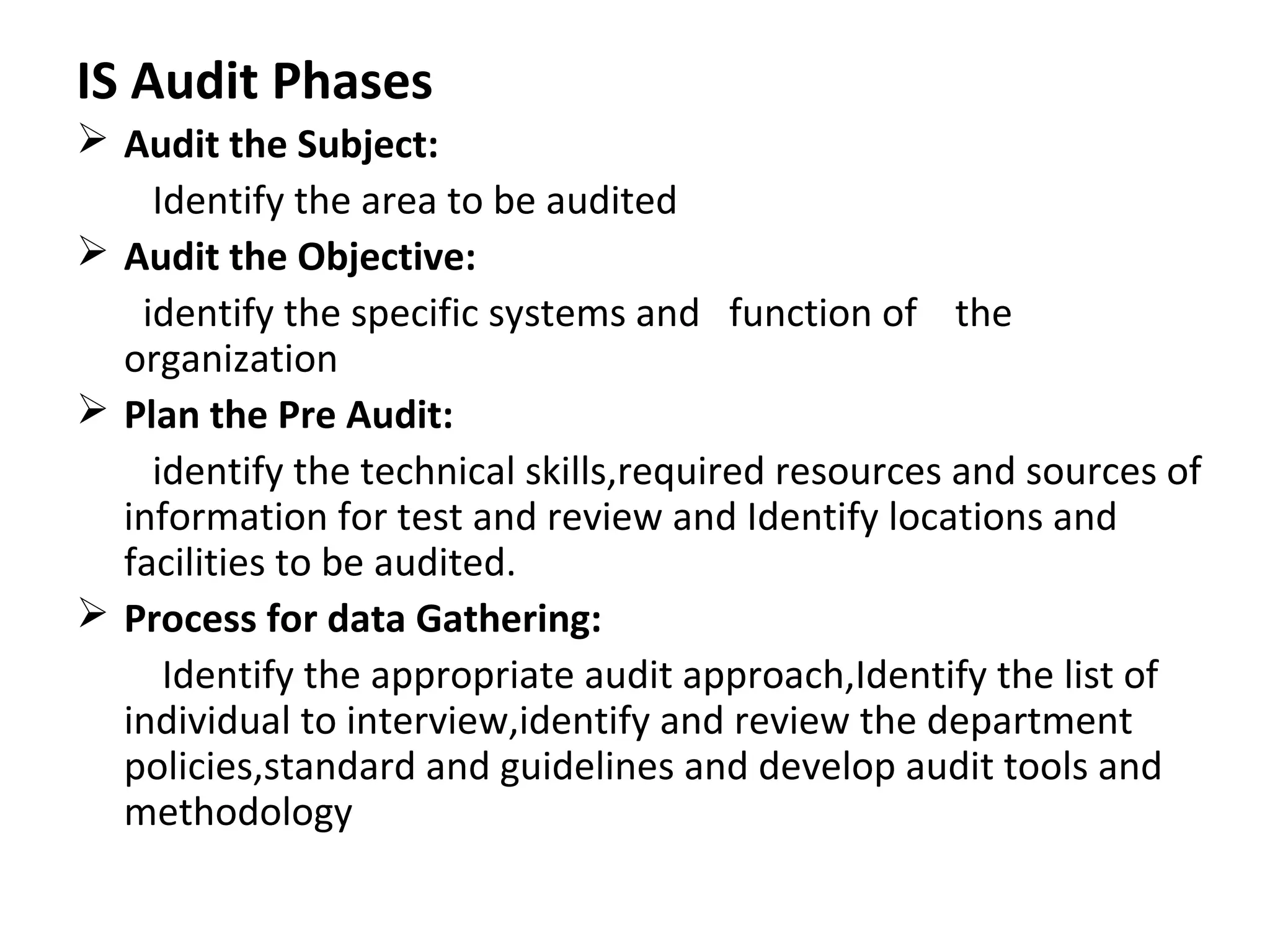

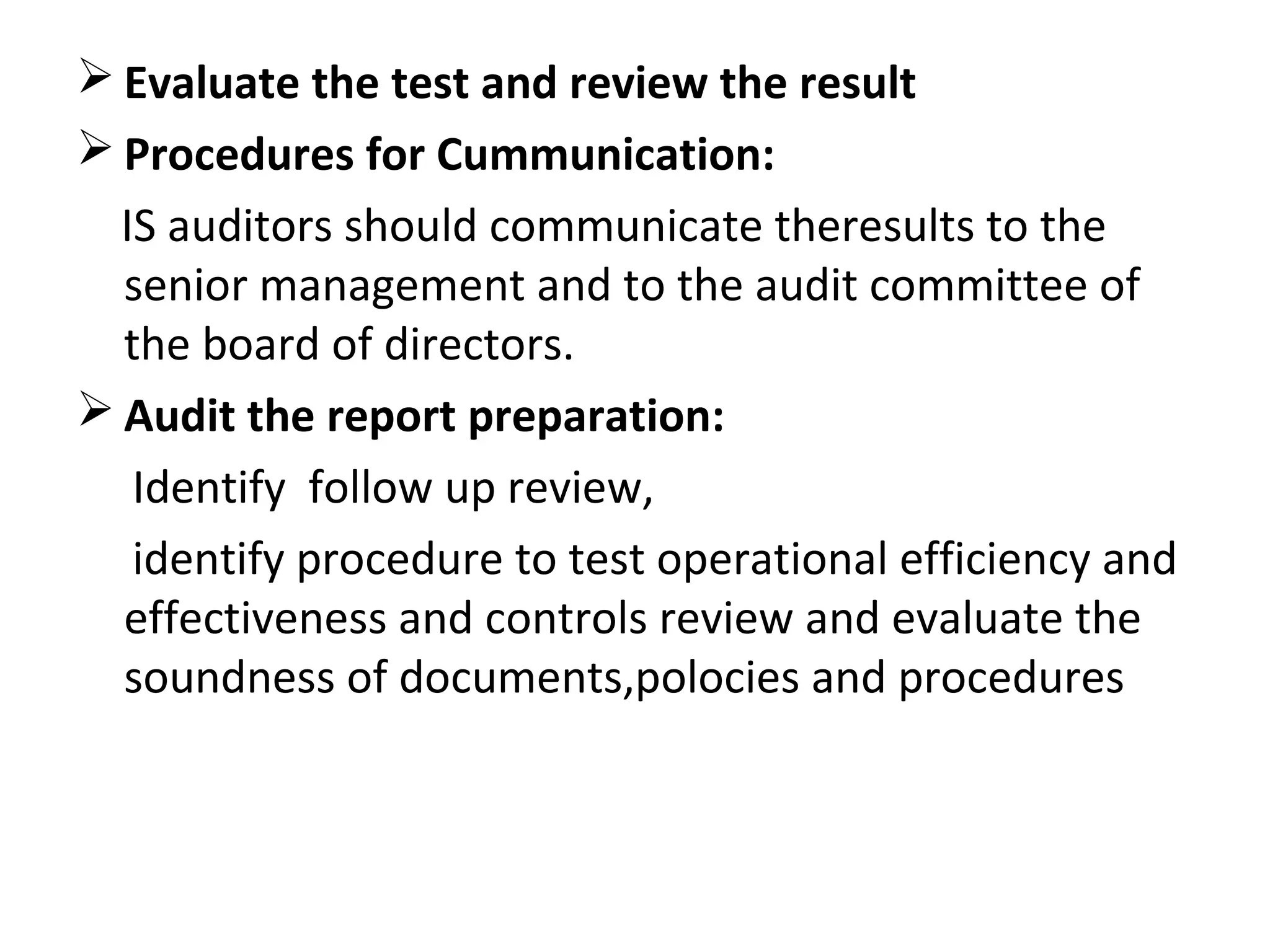

Auditing is the process of independently examining and evaluating records and activities. It helps management by providing suggestions to help an organization achieve its goals. There are two main types of auditing - internal auditing, which depends on management, and external auditing, which is done by individuals outside the company. Information system auditing evaluates whether a system safeguards assets and maintains data integrity. It is a serious process requiring experienced auditors to conduct reviews of areas like finances, operations, administration and information systems. Proper planning, work performance, reporting, and follow up are important parts of the auditing process.

![AUDIT REPORT [ AUDITING ]](https://cdn.slidesharecdn.com/ss_thumbnails/auditingtypesofauditreport-210303052610-thumbnail.jpg?width=640&height=640&fit=bounds)