Downloaded 10 times

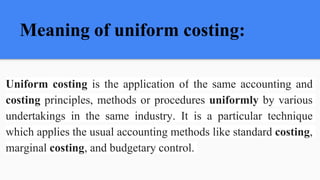

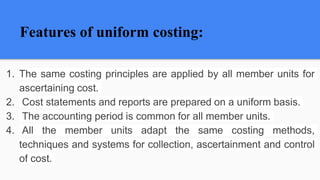

This document provides an overview of uniform and inter-firm costing methods. It defines uniform costing as applying consistent accounting principles across companies in the same industry. The key features are using common costing principles, preparing standardized cost statements, and adopting uniform costing techniques. Uniform costing aims to enable better cost comparisons between firms and improve performance. An effective uniform costing system requires cooperation between companies and information sharing. Inter-firm comparison allows companies to evaluate their costs and profits relative to others in the industry in order to identify weaknesses and improve efficiency.