Downloaded 670 times

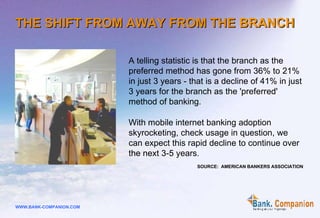

The document discusses various topics related to mobile technology and banking. It provides statistics showing that the US lags behind other countries in mobile adoption but that 4G networks will help close the gap. Mobile video usage is growing significantly and location-based services are popular. Mobile banking adoption is increasing in the US, with over 40 million users expected by 2012, and incentives help drive adoption especially among younger customers. Banks can reduce costs through mobile banking by lowering transaction costs and replacing repetitive tasks done by employees.