Downloaded 541 times

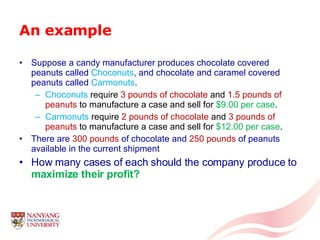

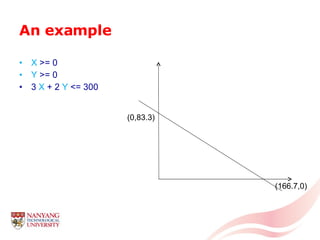

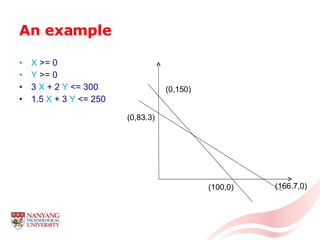

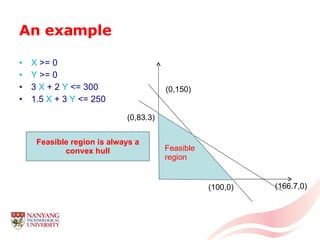

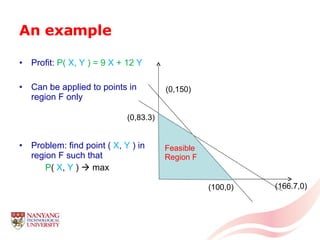

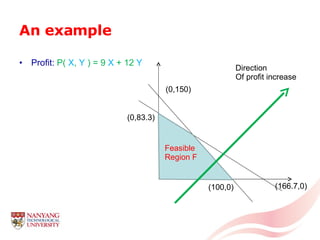

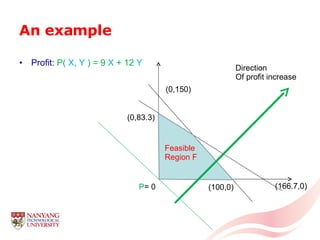

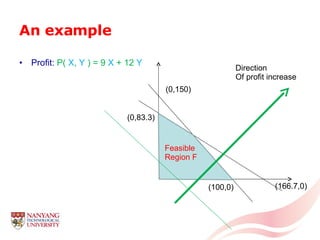

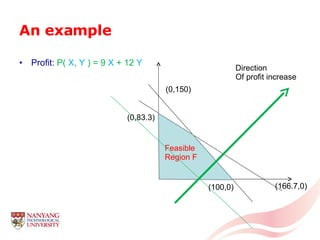

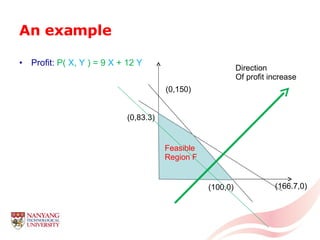

The document introduces linear programming through an example of a candy manufacturer that must determine how many cases of two candy products to make to maximize profit given constraints on available ingredients. It defines variables and constraints, graphs the feasible region, determines the optimal solution that maximizes profit, and discusses how linear programming can be applied to problems with multiple variables and constraints.