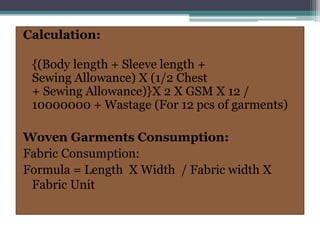

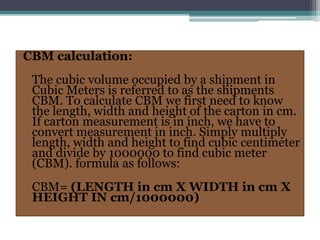

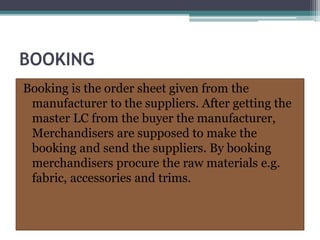

Downloaded 471 times

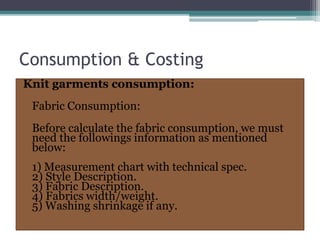

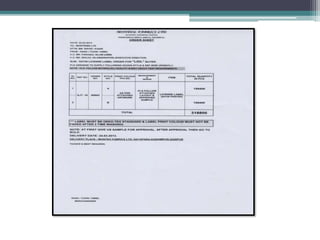

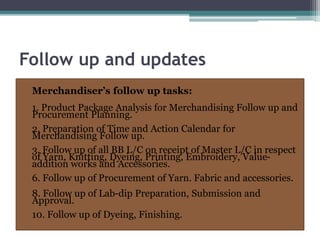

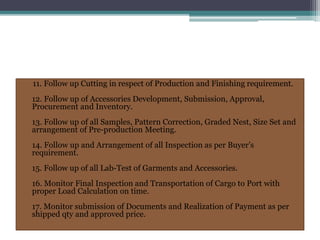

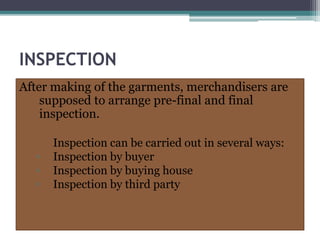

![Cost of Manufacturing (CM) Calculation:

COST OF MAKING (CM) ={(Monthly total

expenditure of the following factory / 26) / (Qty

of running Machine of your factory of the

following month) X (Number of machine to

complete the layout)} / [{(Production capacity

per hr from the existing layout, excluding alter &

reject) X 8}] X 12 / (Dollar conversion rate)](https://image.slidesharecdn.com/activitiesofmerchandiser-140502104016-phpapp02/85/Activities-of-merchandiser-18-320.jpg)

The document provides an in-depth overview of apparel merchandising, detailing the process of managing garment orders, from product development to shipment. It outlines the responsibilities of merchandisers, the objectives in garment merchandising, sample types, production costing, and various payment methods used in international trade. It emphasizes the critical role of merchandisers in coordinating between different sections of the textile industry to ensure successful order fulfillment.