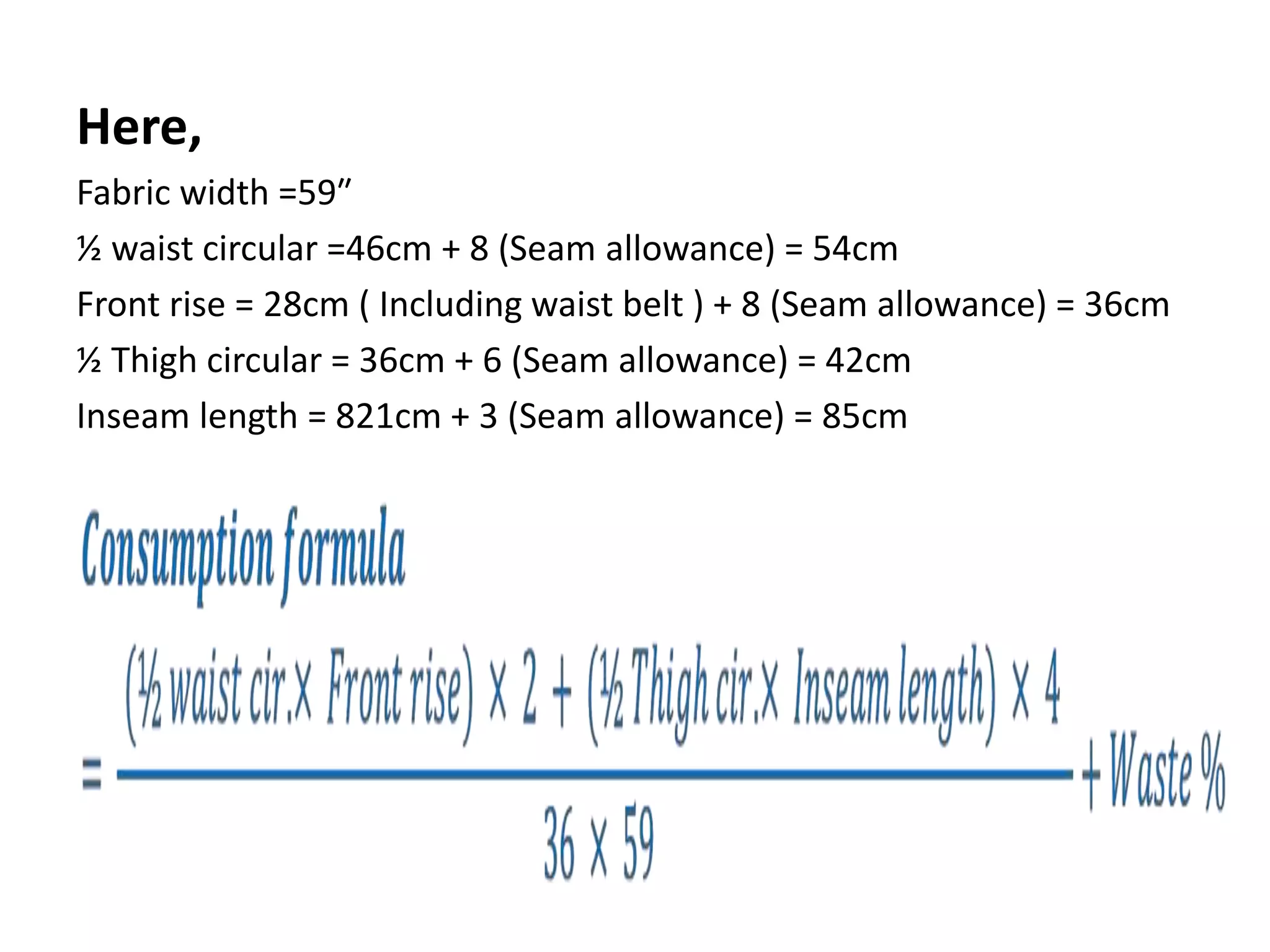

Downloaded 444 times

![Calculation Formula:

Fabric Consumption:

[{(B.L +S.L + 4-10 cm) ×( ½ chest+ 2-4 cm) ×2}×GSM ]

=……………………………………………………………………

10000000

Labour cost per minute = (Monthly salary of

an operators/Total minutes available in the

month](https://image.slidesharecdn.com/garmentscosting-160826190210/75/Garments-costing-4-2048.jpg)

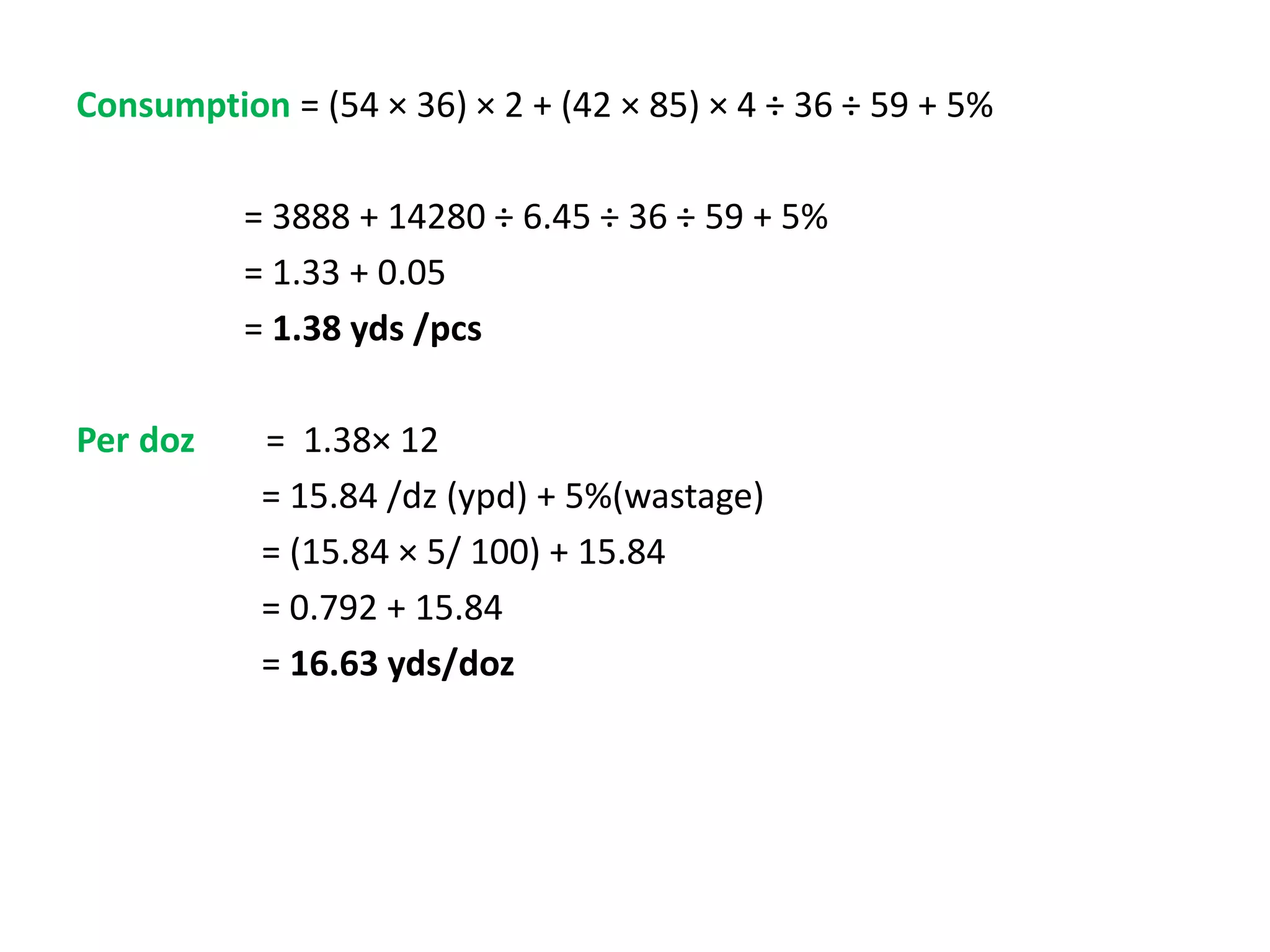

![Solution :-

The fabric consumption can be calculated as

[{(B.L +S.L + 4-10 cm) ×( ½ chest+ 2-4 cm) ×2}×GSM ]

=……………………………………………………………………………………

10000000

[{(75+25 + 4) ×( 60+ 2) ×2}×180 ]

=……………………………………………………..

10000000

= 0.232 + Wastage 10% [if consider 10% wastage]

= 0.255 kg/pcs

CMT (cost of making with trimming) charges may be calculated as follows

Labour cost per minute = (Monthly salary of an operators/Total minutes available in

the month

= 6000/ (26×8×60)

= 0.48 tk.](https://image.slidesharecdn.com/garmentscosting-160826190210/75/Garments-costing-8-2048.jpg)

The document outlines garment costing calculations, including fabric consumption, labor costs, and various direct and indirect costs involved in apparel manufacturing. It includes specific formulas for calculating costs per garment based on dimensions and efficiencies, as well as examples of calculating the costs for a polo neck t-shirt and woven pants. Additionally, it details the breakdown of costs including accessories, transportation, overheads, and profit margins to derive net pricing.