highly fragmented Indian specialty chemicals industry currently has revenues of USD 30 Bn and is expected to grow ~14% per annum over the next decade. It is observed that companies who have invested in product development have grown rapidly and have also expanded globally. Hence, these companies become attractive for large global players and equity investors. Recent M&A transactions in the speciality chemicals space show that most speciality chemical companies were able to attract valuations in excess of 10X EBITDA multiples. The pace of deal making activity is expected to continue with attractive valuations as India is the preferred investment destination in Asia

CRM: MAHINDRA FIRST CHOICE SERVICES: CREATING A VALUE PROPOSITIONDisha Ghoshal

As part of Customer Relationship Management taught by D. Sriram who is an ace in the field of Market Research and Marketing Management and teach at Great Lakes Institute of Management Chennai

Information was complied by the data available on the Internet, personal interviews, a social experiment and I have tried my best to maintain correctness and credits as far as possible. This is a Value Proposition Case Study.

Shifting Trade Rules and the Future for North America’s Auto IndustryBoston Consulting Group

Two major initiatives by the US to overhaul trade rules could have a massive impact on North America’s automotive manufacturing industry. Here’s how companies should prepare.

MGI: From poverty to empowerment: India’s imperative for jobs, growth, and ef...McKinsey & Company

Some 680 million people, or 56% of India, live below MGI’s Empowerment Line and lack acceptable minimum standards of living; the Empowerment Gap is 4% of GDP in value terms (about 7 times the official poverty gap)

From 2005 to 2012, 75% of the improvement in living standards was due to rising incomes, the rest due to government spending; to reduce the gap faster, India needs more productive jobs and higher effectiveness of government spending (e.g., 85 million people below the official poverty line could have been lifted to minimum living standards just by improving delivery of public services)

Almost 40% of the Empowerment Gap comes from health care, drinking water and sanitation; in addition, hunger is a major issue for the poorest segments, and housing for the urban vulnerable

Apart from lacking the means, Indians also lack access to 46% of the basic services they need, with significant variations in the pattern of access deprivation across districts

A path of Stalled Reforms would leave 36% of India below the Empowerment Line and 12% below the Poverty Line in 2022, but the path of Inclusive Reforms can bring these down to 7% and 1% respectively – while achieving fiscal consolidation and reducing access deficit in basic services to 17%, from 46% currently. Raising government spending on subsidies alone delivers just 8% of the total impact. 4 themes are critical

Non-farm jobs deliver >50% of impact; 115 million jobs are needed (38 million more than Stalled Reforms) through 6 broad-ranging reforms and investments in 70-100 job creation engines

Agricultural yield growth delivers ~20% of impact, needing 9 farm sector initiatives and investment rebalancing towards rural infrastructure, research and extension

Public spending on basic services should grow at 7% p.a. in real terms and share of health, water and sanitation to rise from 20% to nearly 50%

Government spending effectiveness must improve from 50% to 75%, by working with private and social sector, community involvement and tight monitoring using technology

Six themes are essential to improve governance across the board (raise institutional capacity and strengthen external accountability)

BCG has launched its Telco Sustainability Index, designed to capture the four dimensions most relevant to a telco’s environmental strategy. The index tracks the company’s commitment to sustainability, its emissions intensity and that of its upstream and downstream partners, its elimination of waste, and its customer enablement.

Business Strategy Presentation Template 2023 - By ex-Mckinsey and BCG consult...Slideworks

A comprehensive, end-to-end strategy presentation template based on proven frameworks created by ex-McKinsey and BCG consultants.

277 PowerPoint slides organized in a complete storyline with best-practice slide-layouts, titles, and graphics

4 real-life full-length examples from Fortune500 companies so you can see how a strategy is presented in other organizations

Helpful checklist used in top-tier consulting firms

Excel model to support your strategy document.

Access full powerpoint at www.slideworks.io.

One in four customers is planning to either use branches less or stop visiting branches altogether after the COVID-19 crisis, according to new BCG retail banking consumer “pulse” survey.

CRM: MAHINDRA FIRST CHOICE SERVICES: CREATING A VALUE PROPOSITIONDisha Ghoshal

As part of Customer Relationship Management taught by D. Sriram who is an ace in the field of Market Research and Marketing Management and teach at Great Lakes Institute of Management Chennai

Information was complied by the data available on the Internet, personal interviews, a social experiment and I have tried my best to maintain correctness and credits as far as possible. This is a Value Proposition Case Study.

Shifting Trade Rules and the Future for North America’s Auto IndustryBoston Consulting Group

Two major initiatives by the US to overhaul trade rules could have a massive impact on North America’s automotive manufacturing industry. Here’s how companies should prepare.

MGI: From poverty to empowerment: India’s imperative for jobs, growth, and ef...McKinsey & Company

Some 680 million people, or 56% of India, live below MGI’s Empowerment Line and lack acceptable minimum standards of living; the Empowerment Gap is 4% of GDP in value terms (about 7 times the official poverty gap)

From 2005 to 2012, 75% of the improvement in living standards was due to rising incomes, the rest due to government spending; to reduce the gap faster, India needs more productive jobs and higher effectiveness of government spending (e.g., 85 million people below the official poverty line could have been lifted to minimum living standards just by improving delivery of public services)

Almost 40% of the Empowerment Gap comes from health care, drinking water and sanitation; in addition, hunger is a major issue for the poorest segments, and housing for the urban vulnerable

Apart from lacking the means, Indians also lack access to 46% of the basic services they need, with significant variations in the pattern of access deprivation across districts

A path of Stalled Reforms would leave 36% of India below the Empowerment Line and 12% below the Poverty Line in 2022, but the path of Inclusive Reforms can bring these down to 7% and 1% respectively – while achieving fiscal consolidation and reducing access deficit in basic services to 17%, from 46% currently. Raising government spending on subsidies alone delivers just 8% of the total impact. 4 themes are critical

Non-farm jobs deliver >50% of impact; 115 million jobs are needed (38 million more than Stalled Reforms) through 6 broad-ranging reforms and investments in 70-100 job creation engines

Agricultural yield growth delivers ~20% of impact, needing 9 farm sector initiatives and investment rebalancing towards rural infrastructure, research and extension

Public spending on basic services should grow at 7% p.a. in real terms and share of health, water and sanitation to rise from 20% to nearly 50%

Government spending effectiveness must improve from 50% to 75%, by working with private and social sector, community involvement and tight monitoring using technology

Six themes are essential to improve governance across the board (raise institutional capacity and strengthen external accountability)

BCG has launched its Telco Sustainability Index, designed to capture the four dimensions most relevant to a telco’s environmental strategy. The index tracks the company’s commitment to sustainability, its emissions intensity and that of its upstream and downstream partners, its elimination of waste, and its customer enablement.

Business Strategy Presentation Template 2023 - By ex-Mckinsey and BCG consult...Slideworks

A comprehensive, end-to-end strategy presentation template based on proven frameworks created by ex-McKinsey and BCG consultants.

277 PowerPoint slides organized in a complete storyline with best-practice slide-layouts, titles, and graphics

4 real-life full-length examples from Fortune500 companies so you can see how a strategy is presented in other organizations

Helpful checklist used in top-tier consulting firms

Excel model to support your strategy document.

Access full powerpoint at www.slideworks.io.

One in four customers is planning to either use branches less or stop visiting branches altogether after the COVID-19 crisis, according to new BCG retail banking consumer “pulse” survey.

Chinese Internet Economy White Paper 2.0 - Decoding the Chinese Internet 2.0:...Boston Consulting Group

Now that China’s major online players have conquered the consumer space, they’re intent on, digitizing B2B industries and building platform-based businesses. China’s consumer internet is driving the development of the industrial internet, according to a new report by Boston Consulting Group (BCG), AliResearch and the Baidu Development Research Center. Comparing the development of China’s consumer internet and industrial internet with foreign markets for the first time, the report systematically reviews China’s internet players’ entrance into the industrial internet, revealing the unique digitalization path in China and its underlying causes.

The COVID-19 crisis is threatening the lives and well-being of the global community. Health, political, societal, and business leaders must drive an integrated response to navigate, manage, and lead through it.

COVID-19’s uneven trajectory has created a slower-than-expected rebound in urban travel worldwide. Some mobility modes, however, are poised to exceed pre-pandemic levels. BCG provides a breakdown of recovery levels in urban mobility by region and mode--and over time.

The enterprise software industry is being transformed by substantial investor capital, Cloud 2.0, artificial intelligence, data protection, preferred platforms, and a talent shortage, leading stakeholders of all kinds to make big changes, and big choices.

By 2030, it is anticipated that the Singapore Nutrition and Supplements market will reach a value of $xx Mn from $458 Mn in 2022, growing at a CAGR of xx% during 2022-2030. The market is primarily dominated by local players such as Eu Yan Sang International, Bio-Life Science Group, and Blackmores.

To get a detailed report, contact us at - info@insights10.com

China Exit or Co-Investment Opportunities for German PE InvestorsL.E.K. Consulting

L.E.K.'s Karin von Kienlin recently presented at BVK on a study conducted by L.E.K. Munich and Shanghai. They wished to:

- Understand developments in Chinese equity investments in both the domestic China / pan-Asian market and cross-border investments between China and Germany / Europe

- Identify trends in likely future investment behavior and its drivers

- Defining success factors both for Chinese and German investors / corporates as to how to benefit from the potential opportunities of cross-border investments and cooperation

Learn more in the presentation here.

Tata Acquired Jaguar Land Rover A Strategic Decision towards Liquidity, Cost ...ijtsrd

Mergers and acquisitions are being considered as one of the most important parts of any internationalisation strategies practised by any multinational company. When any organisation is involved in mergers and acquisitions, they generally used it to accelerate growth and to have access to various valuable assets of other company such as human capital and also to reduce competition in the marketplace to gain absolute competitive advantage in the market. Furthermore there are multiple empirical evidences proved that many mergers and acquisitions fail and being a reason to loss of market shares and exit of key top management personnel from the company. Different examples of failed mergers and acquisitions are found in almost all industries in different contexts. Many failure cases show us genuine discrepancy between the expectations, motivating acquisitions and the difficulty encountered to realise the expected value in the market and a complete miscalculations by the company and without knowing the ground reality they opted for or the acquisition. In June 2008 India based Tata Motors Limited had announced that it had completed the acquisition of the two extremely glamorous and iconic British brands Jaguar and Land Rover from the US based food Motors for 2.3 billion USD. There are many experts who had shared their comments and it was mentioned that such acquisition would eventually help the parent company in several ways especially to attract the global audience, to get an international footprint and it will also help the parent company to enter the high end premium segment of the global automobile market and with the help of that the company would able to strengthen their presence in premium segment. Pritam Chattopadhyay "Tata Acquired Jaguar Land Rover: A Strategic Decision towards Liquidity, Cost Control and New Product" Published in International Journal of Trend in Scientific Research and Development (ijtsrd), ISSN: 2456-6470, Volume-5 | Issue-4 , June 2021, URL: https://www.ijtsrd.compapers/ijtsrd42361.pdf Paper URL: https://www.ijtsrd.commanagement/business-policies-and-strategies/42361/tata-acquired-jaguar-land-rover-a-strategic-decision-towards-liquidity-cost-control-and-new-product/pritam-chattopadhyay

The trends & facts of mergers & acquisitions in the international markets. India\'s & India Inc.\'s role & progress in the Global markets.

Chinese Internet Economy White Paper 2.0 - Decoding the Chinese Internet 2.0:...Boston Consulting Group

Now that China’s major online players have conquered the consumer space, they’re intent on, digitizing B2B industries and building platform-based businesses. China’s consumer internet is driving the development of the industrial internet, according to a new report by Boston Consulting Group (BCG), AliResearch and the Baidu Development Research Center. Comparing the development of China’s consumer internet and industrial internet with foreign markets for the first time, the report systematically reviews China’s internet players’ entrance into the industrial internet, revealing the unique digitalization path in China and its underlying causes.

The COVID-19 crisis is threatening the lives and well-being of the global community. Health, political, societal, and business leaders must drive an integrated response to navigate, manage, and lead through it.

COVID-19’s uneven trajectory has created a slower-than-expected rebound in urban travel worldwide. Some mobility modes, however, are poised to exceed pre-pandemic levels. BCG provides a breakdown of recovery levels in urban mobility by region and mode--and over time.

The enterprise software industry is being transformed by substantial investor capital, Cloud 2.0, artificial intelligence, data protection, preferred platforms, and a talent shortage, leading stakeholders of all kinds to make big changes, and big choices.

By 2030, it is anticipated that the Singapore Nutrition and Supplements market will reach a value of $xx Mn from $458 Mn in 2022, growing at a CAGR of xx% during 2022-2030. The market is primarily dominated by local players such as Eu Yan Sang International, Bio-Life Science Group, and Blackmores.

To get a detailed report, contact us at - info@insights10.com

China Exit or Co-Investment Opportunities for German PE InvestorsL.E.K. Consulting

L.E.K.'s Karin von Kienlin recently presented at BVK on a study conducted by L.E.K. Munich and Shanghai. They wished to:

- Understand developments in Chinese equity investments in both the domestic China / pan-Asian market and cross-border investments between China and Germany / Europe

- Identify trends in likely future investment behavior and its drivers

- Defining success factors both for Chinese and German investors / corporates as to how to benefit from the potential opportunities of cross-border investments and cooperation

Learn more in the presentation here.

Tata Acquired Jaguar Land Rover A Strategic Decision towards Liquidity, Cost ...ijtsrd

Mergers and acquisitions are being considered as one of the most important parts of any internationalisation strategies practised by any multinational company. When any organisation is involved in mergers and acquisitions, they generally used it to accelerate growth and to have access to various valuable assets of other company such as human capital and also to reduce competition in the marketplace to gain absolute competitive advantage in the market. Furthermore there are multiple empirical evidences proved that many mergers and acquisitions fail and being a reason to loss of market shares and exit of key top management personnel from the company. Different examples of failed mergers and acquisitions are found in almost all industries in different contexts. Many failure cases show us genuine discrepancy between the expectations, motivating acquisitions and the difficulty encountered to realise the expected value in the market and a complete miscalculations by the company and without knowing the ground reality they opted for or the acquisition. In June 2008 India based Tata Motors Limited had announced that it had completed the acquisition of the two extremely glamorous and iconic British brands Jaguar and Land Rover from the US based food Motors for 2.3 billion USD. There are many experts who had shared their comments and it was mentioned that such acquisition would eventually help the parent company in several ways especially to attract the global audience, to get an international footprint and it will also help the parent company to enter the high end premium segment of the global automobile market and with the help of that the company would able to strengthen their presence in premium segment. Pritam Chattopadhyay "Tata Acquired Jaguar Land Rover: A Strategic Decision towards Liquidity, Cost Control and New Product" Published in International Journal of Trend in Scientific Research and Development (ijtsrd), ISSN: 2456-6470, Volume-5 | Issue-4 , June 2021, URL: https://www.ijtsrd.compapers/ijtsrd42361.pdf Paper URL: https://www.ijtsrd.commanagement/business-policies-and-strategies/42361/tata-acquired-jaguar-land-rover-a-strategic-decision-towards-liquidity-cost-control-and-new-product/pritam-chattopadhyay

The trends & facts of mergers & acquisitions in the international markets. India\'s & India Inc.\'s role & progress in the Global markets.

Mergers & acquisitions in india december 2014ajsh123

A Leading CA Firm in Delhi offers chartered accountant services & financial services all over the world. Call +91-9810661322 for a financial plan for your Business.

Dai Ichi Karkaria: Buy at CMP and add on declinesIndiaNotes.com

At CMP of Rs 85, the company is trading at 6.1x its FY14 Adjusted EPS of Rs 13.9. Investors could buy the stock at the CMP and add on dips to Rs.70-76 band (~5.25 xFY14 EPS) for sequential target prices of Rs 111 and 125.

With India’s GDP to clock 7 to 7.5%, the Indian Paints Industry is expected to grow rapidly in the coming years. The decorative paints segment has been the main revenue driver. In the decorative segment, customer preferences are changing, and companies are using innovation to cater to the demand.

However, there will be an upstick in demand for industrial paints in the months ahead, on the back of the massive infrastructure moves by Government of India – from roads to ports; from smart cities to urban mission.

This CMR IMG report will help readers to get the big picture on the Indian Paints Industry. Readers will be able to understand current demand and supply drivers in the paints market, and spot future trends.

This IMG report analyzes Asian Paints, Kansai Nerolac, Berger Paints, Akzo Nobel and Shalimar Paints.

With the government targeting implementation

of GST in the next financial year, the

Indian industry will be busy understanding

its impact and deciding on how to do

business in the changed environment. The USD 40 bn.

Pharmaceutical industry is no exception as it has to prepare

itself for GST readiness and reevaluate its complex

supply chain network which span across India.

Feedstock availability, difficult access to latest technology and unfavourable duty structures have led to muted investments resulting in a plethora of chemicals being imported in India across the value chain. The net imports have risen from USD 2.6 bn in FY08 to USD 13.8 bn in FY15. Imports of several chemicals and polymers today are equivalent to a global scale plant output. With chemical demand shifting towards Asia, and China reassessing its chemical industry play, it could offer opportunities for chemical companies to invest selectively in India. To top it, government’s enhanced focus on `Make in India` and several states making chemicals as one of the preferred industries will facilitate realizing such opportunities. To make the most of the USD 12 bn opportunity in petrochemical intermediates, we believe companies need to reassess their business model & manufacturing footprint.

Telecom towers have traditionally relied on Gensets and Batteries for their power backup. With these methods, the challenges of high operating costs due to maintenance, repairs and cost of fuel are well known. Fuel cells have lately emerged as a potential alternate for this application. It is a market to watch closely as further technology improvements in the coming years will happen. The time is right to further improve upon the backup power technology. The Government, TRAI and telecom operators will need to work together to make fuel cells usage mainstream. Given the competitiveness of solar power, a hybrid of fuel cell & solar could emerge as a perfect combination which is reliable, sustainable, and a green alternative in future

The opportunities for the Indian pharmaceutical industry are immense but increasing competition, increasing regulatory pressures and stringent price control means that companies need to constantly improve their costs and service levels. Supply chain efficiencies will play a crucial role going forward and will become the key differentiator for companies. Companies will therefore need to adopt an approach that encompasses strategic, tactical and operational interventions to remain competitive and create value for their customers

This CII report on “Securing our water resources”, prepared by Tata Strategic Management

Group, has a holistic view on the current state of domestic and industrial water management

practices, with an overview of the state of water affairs in Gujarat. The key focus of the

report is on identifying a set of solutions that can mitigate the growing water challenges.

These solutions are developed as part of a structured framework aimed at analysing and

resolving the water issues.

This report on “O&M Strategies for Superior Performance”, prepared by Tata Strategic Management Group, has a holistic view on the current state of Operations and Maintenance at the Indian power plants. The key focus of the report is on identifying key external and internal challenges in the Indian market and how power producers could ensure superior returns through effective O&M in this challenging environment.

This report on “Solar PV Sector in India: Challenges & Way ahead”, prepared by Tata Strategic Management Group, has a holistic view on the current state of solar sector in India. The key focus of the report is on identifying key challenges faced by different stakeholders in the Indian market and how a collaborative effort in the right direction could ensure the growth of the sector to realize its true potential

This report on “Energy Efficiency in India: PAT Scheme - Success and Failures”, prepared by Tata Strategic Management Group, has a holistic view on the current state of energy efficiency and energy management in India. The focus of this report is on identifying key challenges faced by designated consumers in implementation of PAT Cycle I and how a collaborative effort in the right direction could ensure fast adoption of EE and robust energy management in India. It would gear India towards reducing energy intensity of the future growth, one of the prime objectives under NAPCC

This report provides an overview of the Indian plastic industry, its past growth, challenges faced, emerging applications and its future growth prospects. The focus of the report is on agriculture (Plasticulture) and Packaging plastic applications. It also highlights the role northern states of India are expected to play as the demand for plastics is expected to double by 2020.

The report is presented by TATA Strategic Management Group with an objective to highlight key trends in the Indian bulk liquid storage industry and opportunities present in this sector

The Indian plastic industry is making significant contribution to the economic development and growth of various key sectors in the country which includes Automotive, Construction, Electronics, Healthcare, Textiles, and FMCG. The developments in the plastic machinery sector are coupled with developments in the petrochemical sector, both of which support the plastic processing sector. This has facilitated plastic processors to build capacities for the service of both the domestic market and the markets oversea.

The Government of India is taking every possible initiative to boost the infrastructure sector with investments of INR 25 lakh crore over the next 3 years in roads, railways and shipping infrastructure. Investments in water and sanitation management, irrigation, building & construction, power, transport and retail have been encouraged. Plastics play an important role in these sectors through various products like pipes, wires & cables, water proofing membranes, wood PVC composites and other sectors. Consequently, higher investments in these sectors will drive the demand for plastics.

Chemicals industry is a diversified industry and covers more than 80,000 commercial products. It provides key building blocks to a host of downstream industries such as automobiles, textiles, papers, paints, soaps, detergents, pharmaceuticals among many others. It is a capital intensive industry which employs approx. 2 Mn people in India. As a result, it plays a key role in the economic and social development of the country. It is a critical element of the manufacturing industry and is highly fragmented in the downstream sector. Globally, chemical industry was valued at $ 4.5 Tn in 2016 and is expected to grow at 5.5% per annum till 2020 driven by demand from end use industries. The industry is increasingly shifting eastwards in line with the shift of its key consumer industries (e.g. automotive, electronics, etc.), to leverage higher manufacturing competitiveness of emerging Asian economies and to serve the increasing local demand. China, as result of this shift, is the largest contributor with 34% share followed by European Union (17%) and North America (16%) to the global chemical industry.

Agriculture holds a prime importance in the socio-economic fabric of India. Agriculture and allied sectors have remained the backbone of the Indian economy and account for ~17% of the country's GDP. India, with a second largest agricultural land in the world (157 Mn hectares), is also ranked 2nd globally in terms of agricultural output (USD 382 Bn) behind China (USD 1,005 Bn). Agriculture in India employs more than 50% of India's working population. A split of major Agricultural produce in India (FY15) is provided in the graph below. Sugarcane and Fruits & vegetable contributed to 57% of the total volume of 1,080 Million tonnes

The Indian chemical industry is overall the 3rd largest in Asia after China and Japan in terms of volume contribution to the global market. The chemical industry in India has started to evolve rapidly since the last five years and has grown to an estimated USD 148 billion in FY16. Despite its large size and significant GDP contribution, the industry accounted for only around 3% of the global chemicals industry (~USD 4.3 Trillion). As per UN Comtrade Database for 2015, India ranks 17th in the world exports of chemicals (excluding pharmaceutical products) and ranks 6th in the world imports of chemicals (excluding pharmaceutical products).

Globally, the demand for industrial catalysts is driven by the surging demand for chemicals in various end applications in industries such as personal care products, lubricants, petroleum refinery, pharmaceuticals and foods & beverages. Growing awareness among manufacturers of chemicals and consumers, related to environment and increasing emissions impacting the eco system have led to highly intense competition in the global market for catalysts.

As per research reports, the global industrial catalyst market is estimated at roughly USD 17.5 bn (depicted in Figure 5) as of FY15 and is forecasted to grow at a CAGR of 4% - 5% during FY15 to FY20, on account of rising consumption of chemicals and their applicability. The APAC region remains the major market followed by North America and Europe. In the forecast period, the APAC region is expected to continue to witness strong growth driven by India and China

Indian Plastic industry is making significant contribution to the economic development and growth of various key sectors in the country such as: Automotive, Construction, Electronics, Healthcare, Textiles, FMCG , etc. It 2 has grown at 10% CAGR over the last five years to reach 13.4 MTPA in FY15. Current low penetration level and hence, low per capita consumption (~9.7 Kg) along with increased growth in end use industries could propel the growth of plastics further. Plastic industry is estimated to grow at ~10% in the near future reaching 21.6 MTPA by FY20.

India’s chemical industry contributes approximately 7% to the country’s GDP and accounted for ~13-14% of the total Indian exports in 2015. The Indian chemical industry accounts for ~4% of the global chemical industry. Indian chemical industry is currently estimated at ~USD 151 billion (including pharmaceuticals) and has been growing at 9.8% CAGR over the past three years. The demand growth is expected to primarily be fuelled by domestic consumption because per capita consumption of most of the chemicals is much lower than global averages. Moreover, with a strong outlook for key end user industries, the demand for chemical products is expected to surge in the coming years.

The western coast of India has been the key hub for chemicals and petrochemicals industry with Gujarat and Maharashtra alone accounting for 62% of major chemical and petrochemicals production across India. Since production clusters are concentrated in one particular region, better infrastructure and logistics are required to supply chemical products across the country. The lengthening of supply lines makes the distribution of chemicals more transport intensive. The involvement of a large number of stakeholders (shipping lines, transport agencies, environmental agencies, etc.) in the transportation of chemical products increases the logistics and supply chain complexity of the chemicals industry.

There has been significant progress in the adoption of Plasticulture techniques in the last decade, however the low penetration levels suggest it needs to grow at a rapid pace from now. On the demand side awareness of the available options and subsidies, its relevance and applicability could improve the adoption rate. From the supply side industry needs to take efforts to bring down the capital cost, work on creating an environment where Plasticulture culture is a norm than exception. Concentrated efforts in direction of demonstration, spreading word of mouth, and building credibility by performance & after-sales services could help shape the industry.

India is the fourth largest global producer of agrochemicals after the US, Japan and China. This segment generated a value of USD 4.4 billion in FY15 and is expected to grow at 7.5% per annum to reach USD 6.3 billion by FY20. Approximately 50% of the demand comes from domestic consumers and the rest from exports. During the same period, the domestic demand is expected to grow at 6.5% per annum and exports at 9% per annum.

More from TATA Strategic Management Group- Chemicals Vertical (20)

Want to move your career forward? Looking to build your leadership skills while helping others learn, grow, and improve their skills? Seeking someone who can guide you in achieving these goals?

You can accomplish this through a mentoring partnership. Learn more about the PMISSC Mentoring Program, where you’ll discover the incredible benefits of becoming a mentor or mentee. This program is designed to foster professional growth, enhance skills, and build a strong network within the project management community. Whether you're looking to share your expertise or seeking guidance to advance your career, the PMI Mentoring Program offers valuable opportunities for personal and professional development.

Watch this to learn:

* Overview of the PMISSC Mentoring Program: Mission, vision, and objectives.

* Benefits for Volunteer Mentors: Professional development, networking, personal satisfaction, and recognition.

* Advantages for Mentees: Career advancement, skill development, networking, and confidence building.

* Program Structure and Expectations: Mentor-mentee matching process, program phases, and time commitment.

* Success Stories and Testimonials: Inspiring examples from past participants.

* How to Get Involved: Steps to participate and resources available for support throughout the program.

Learn how you can make a difference in the project management community and take the next step in your professional journey.

About Hector Del Castillo

Hector is VP of Professional Development at the PMI Silver Spring Chapter, and CEO of Bold PM. He's a mid-market growth product executive and changemaker. He works with mid-market product-driven software executives to solve their biggest growth problems. He scales product growth, optimizes ops and builds loyal customers. He has reduced customer churn 33%, and boosted sales 47% for clients. He makes a significant impact by building and launching world-changing AI-powered products. If you're looking for an engaging and inspiring speaker to spark creativity and innovation within your organization, set up an appointment to discuss your specific needs and identify a suitable topic to inspire your audience at your next corporate conference, symposium, executive summit, or planning retreat.

About PMI Silver Spring Chapter

We are a branch of the Project Management Institute. We offer a platform for project management professionals in Silver Spring, MD, and the DC/Baltimore metro area. Monthly meetings facilitate networking, knowledge sharing, and professional development. For event details, visit pmissc.org.

New Explore Careers and College Majors 2024.pdfDr. Mary Askew

Explore Careers and College Majors is a new online, interactive, self-guided career, major and college planning system.

The career system works on all devices!

For more Information, go to https://bit.ly/3SW5w8W

The Impact of Artificial Intelligence on Modern Society.pdfssuser3e63fc

Just a game Assignment 3

1. What has made Louis Vuitton's business model successful in the Japanese luxury market?

2. What are the opportunities and challenges for Louis Vuitton in Japan?

3. What are the specifics of the Japanese fashion luxury market?

4. How did Louis Vuitton enter into the Japanese market originally? What were the other entry strategies it adopted later to strengthen its presence?

5. Will Louis Vuitton have any new challenges arise due to the global financial crisis? How does it overcome the new challenges?Assignment 3

1. What has made Louis Vuitton's business model successful in the Japanese luxury market?

2. What are the opportunities and challenges for Louis Vuitton in Japan?

3. What are the specifics of the Japanese fashion luxury market?

4. How did Louis Vuitton enter into the Japanese market originally? What were the other entry strategies it adopted later to strengthen its presence?

5. Will Louis Vuitton have any new challenges arise due to the global financial crisis? How does it overcome the new challenges?Assignment 3

1. What has made Louis Vuitton's business model successful in the Japanese luxury market?

2. What are the opportunities and challenges for Louis Vuitton in Japan?

3. What are the specifics of the Japanese fashion luxury market?

4. How did Louis Vuitton enter into the Japanese market originally? What were the other entry strategies it adopted later to strengthen its presence?

5. Will Louis Vuitton have any new challenges arise due to the global financial crisis? How does it overcome the new challenges?

This comprehensive program covers essential aspects of performance marketing, growth strategies, and tactics, such as search engine optimization (SEO), pay-per-click (PPC) advertising, content marketing, social media marketing, and more

Acquisition Route to Growth in Indian Specialty Chemicals

1. 12 z CHEMICAL NEWS APRIL 2016

T

he highly fragmented Indian specialty chemicals

industry currently has revenues of USD 30 Bn

and is expected to grow ~14% per annum over

the next decade. It is observed that companies

who have invested in product development have grown

rapidly and have also expanded globally. Hence, these

companies become attractive for large global players and

equity investors. Recent M&A transactions in the speciality

chemicals space show that most speciality chemical

companies were able to attract valuations in excess of

10X EBITDA multiples. The pace of deal making activity is

expected to continue with attractive valuations as India is

the preferred investment destination in Asia, say Manish

Panchal, Karthikeyan K.S., and Kiran Dukare of Tata

Strategic Management Group.

INDUSTRY: CURRENT STATE

Specialty chemicals are relatively high value products

compared to commodity chemicals. In today’s highly

competitive environment, specialty chemicals have the

potential to help end use sectors to differentiate their

products with respect to the competition. These chemicals

play an important role in several end use industries

such as dyes & pigments, flavors & fragrances, leather,

construction, paper and personal care segments.

India will see a surge in domestic consumption of

specialty chemicals driven by its demographic dividend

and increasing disposable income. This will change

the landscape of the Speciality Chemicals market in

India which currently has revenue of ~USD 30 Bn and

is expected to reach USD 80 Bn by 2023. At 14% CAGR

specialty chemical industry is expected to grow much

faster than India’s GDP growth.

The factors contributing to high growth in Indian

Specialty Chemical industry are:

z Buoyant domestic demand due to high growth in end

use industry and possible inflection points in several

segments in the near future (Refer Figure 1)

z Encouraging export opportunities due to bleak

forecasts for Chinese chemical industry (owing to

increasing cost pressure, tightening pollution control

norms and appreciation of Chinese Yuan against USD)

z GOI initiatives like proposed changes in customs &

excise duty rates on certain inputs/ raw materials

to reduce costs and improve competitiveness of

domestic industry in sectors like speciality chemicals &

petrochemicals

z Technology up-gradation fund (TUF) and National

Innovation Fund for chemical industry

z Stable IPR regime with well-defined IPR policy makes

India a preferred destination for knowledge based

chemicals and R&D centre

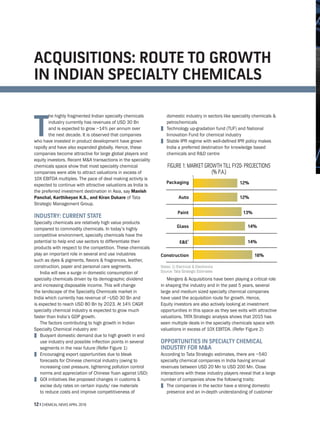

FIGURE 1: MARKET GROWTH TILL FY20- PROJECTIONS

(% P.A.)

Notes: 1) Electrical & Electronics

Source: Tata Strategic Estimates

Mergers & Acquisitions have been playing a critical role

in shaping the industry and in the past 5 years, several

large and medium sized specialty chemical companies

have used the acquisition route for growth. Hence,

Equity investors are also actively looking at investment

opportunities in this space as they see exits with attractive

valuations. TATA Strategic analysis shows that 2015 has

seen multiple deals in the specialty chemicals space with

valuations in excess of 10X EBITDA. (Refer Figure 2)

OPPORTUNITIES IN SPECIALTY CHEMICAL

INDUSTRY FOR M&A

According to Tata Strategic estimates, there are ~540

specialty chemical companies in India having annual

revenues between USD 20 Mn to USD 200 Mn. Close

interactions with these industry players reveal that a large

number of companies show the following traits:

z The companies in the sector have a strong domestic

presence and an in-depth understanding of customer

ACQUISITIONS: ROUTE TO GROWTH

IN INDIAN SPECIALTY CHEMICALS

12%

12%

13%

14%

14%

16%

E&E

1

Glass

Paint

Auto

Packaging

Construction

2. CHEMICAL NEWS APRIL 2016 z 13

needs. Over the years, companies have fine-tuned

their products thereby making them unique in terms of

value proposition for Indian market and neighbouring

geographies

z Several companies, though small in size, have

established unique positioning and are today leaders

in their product segments. As a result, revenues from

exports are higher than domestic revenues for such

companies

z Numerous companies lack resources and know-

how to scale up operations. With access to the right

technology, technical expertise and other resources

they can provide better solutions and value proposition

Source: VC Circle, DealCurry, TSMG Deal Tracker

Investee

Sector

EBITDA

Multiple

(EV/

EBITDA)

Investee Investor Company Deal

Year

Deal Type Stake

%

Deal

Value

(INR

Cr)

Revenue

Multiple

(EV/R)

Agro Chemicals

Agro Chemicals

& Seeds

Specialty

Chemicals

Oleo Chemicals

Agro & Pharma

Ingredients

Specialty

Chemicals

2015

2015

2014

2015

2015

2015

SH Kelkar & Co.

Exit through

IPO

Agreed

Stake Buy

Stake Buy

Stake Buy

Stake Buy

Stake Buy

100%

45%

76%

7%

4%

3%

4.7X

1.9X

1.6X

1.9X

2.8X

2.5X

2,400

130

213

34

95

60

24.8X

11.2X

22.0X

11.1X

16.4X

10.0X

Vinati Organics

Dhanuka Agritech

Lighthouse

partners lip

FIGURE 2: SOME RECENT TRANSACTIONS IN SPECIALTY CHEMICAL SPACE IN 2015

for the Indian market

z A significant portion of specialty chemical companies

in India are family owned businesses and some of the

1st generation entrepreneurs are facing a succession

void due to unwillingness of 2nd generation to join the

business. Such owners are looking for strategic buyers

who may give better valuation

Because of the above factors, several speciality

chemical companies are looking for alliances, partnerships,

and exit options. This offers attractive options for chemical

companies looking to enter into high margin downstream

businesses. They can take the M&A route to gain access to

new technologies and customer segments.

3. 14 z CHEMICAL NEWS APRIL 2016

WHY M&A ROUTE?

Companies resort to acquisitions for variety of reasons as

summarised in Figure 3

z Speed to market - Several domestic specialty

chemical players have built an established network

of distributors and channel partners across the vast

geographic landscape of India. These companies also

have a team of skilled people and possess required

licences and clearances. The M&A option provides an

opportunity to leverage these strengths and create

a pan-India presence from day one. Several large

domestic and global manufacturers have realized this

advantage.

The recent agreement by Clariant to acquire Vivimed’s

personal care business and German chemical

distributor Brenntag’s agreement to acquire the

speciality chemicals distribution business of Pioma

Chemicals are good examples of how global speciality

chemical player use acquisitions to increase their

presence in emerging markets and add synergies to

their product portfolio and customer base.

z Integrated presence along value chain – M&A

provides both backward integration option to secure

feedstock or intermediates and forward integration into

downstream products to build an integrated presence

in the value chain. For example, Arkema acquired

Ihsedu Agrochem in 2012 to get access to castor oil

since India is one of the largest producers of castor oil

in the world. Through this Arkema was able to secure

consistent access to castor oil for manufacturing bio-

based polyamides at competitive prices.

z Product-portfolio expansion – Most of the upstream

chemical segments are generally low-margin high

volume commodity businesses. Many companies

in such segments are often looking to expand into

downstream specialty segments which may give higher

margins.

z Acquisitions for financial return - Many private-equity

and financial investors have shown keen interest in

investing and acquiring speciality chemical companies

as they are less prone to business cyclicality and offer

higher return on investment.

While growing through M&A does offer significant

benefits, only the successful M&A’s create sustainable

value. Therefore, it is imperative for companies to ensure

that they adopt a proven approach for M&A activity. TATA

Strategic recommends the following levers for successful

M&A’s.

LEVERS FOR SUCCESSFUL M&A

Various levers are necessary for a successful M&A in India

as summarised in Figure 4

1 Define strategic intent – A decision for persuing M&A

should be based on a clearly defined strategic intent.

As mentioned earlier, speed to market, access to select

segments or raw materials could be some examples.

But, there could be specific needs such as brand

acquisition, getting access to technologies, adjacencies

etc. An in-depth evaluation on why the company needs

to make an acquisition and whether the strategic intent

is in line with its global vision and aspirations is a must.

2 Target Screening - It is said that “Well begun is half

done”. This is particularly true in case of identification

of right M&A targets. While specialty chemical

companies in India are aplenty, understanding their

business realities is the key to decide whether they

§ Define M&A

Objective

§

§

Strategy

Development

Implementation

Planning

§ Develop target

search criteria

§

§

Target

Identification

Target

Evaluation

§ Market Context

§

§

§

Synergy/Merger

Benefit Potential

Internal Valuation

Letter Of Intent

§ Deal Strategy

§

§

Deal Negotiation

Deal Closure

§ Strategic Due

Diligence

§

§

§

Financial Due

Diligence

Legal Due Diligence

Deal Valuation

§ Business Process

Integration

§

§

Financial & Legal

Integration

Organization and

Culture Integration

Transaction Execution

Pre Due

Diligence

Due

Diligence

Deal

Execution

M&A

Strategy

Target

Screening

Post Merger

Integration

Reasons behind selling stake

Consolidation of product portfolio

Stronger presence across the value chain

Good exit opportunities for PE/VCs

Succession issues

Faster expansion of product portfolio

Trading companies can venture into manufacturing

Reasons behind acquisitions

FIGURE 3: MOST COMMON REASONS BEHIND M&A IN

SPECIALTY CHEMICALS SPACE

Source: Tata Strategic Research

FIGURE 4: LEVERS FOR SUCCESSFUL M&A

Source: Tata Strategic Research