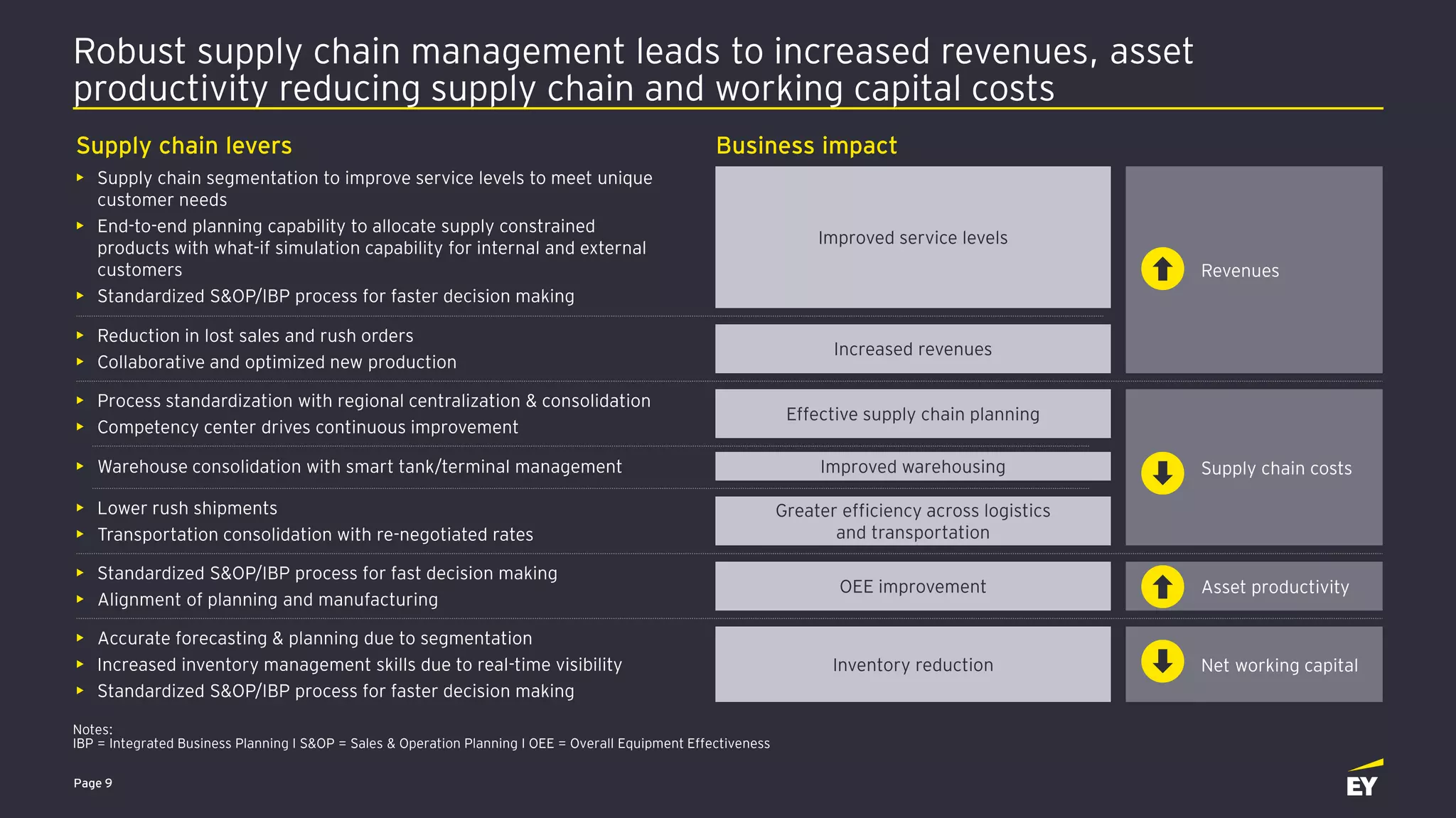

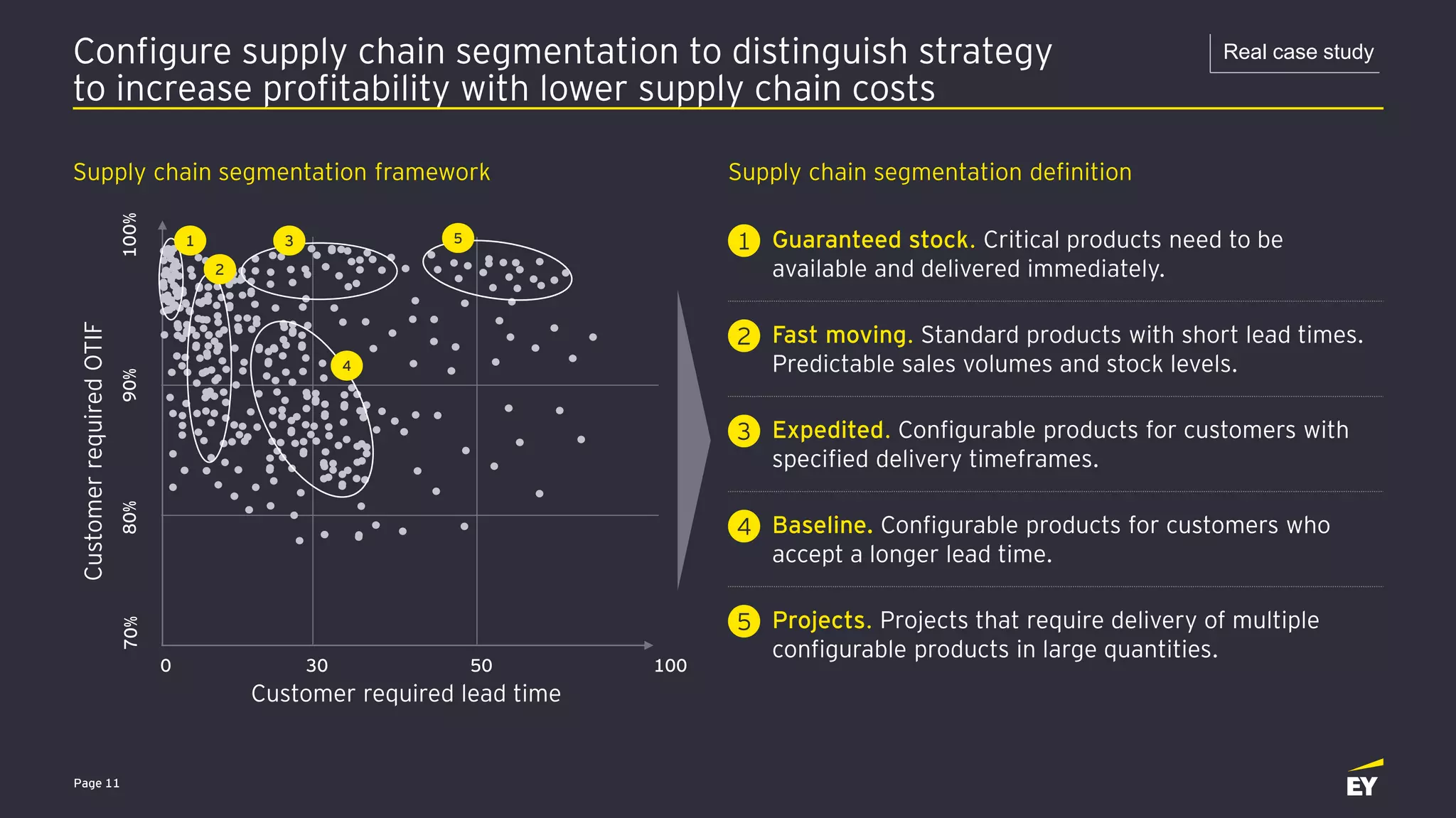

The document discusses developing an integrated chemical supply chain. It recommends segmenting the supply chain based on customer needs to improve profitability. It also recommends configuring an agile supply chain organization model with end-to-end planning capability and competence to respond quickly to customers. Automating decision making across the supply chain with intelligence can help manage new complexity at scale and speed. Developing an integrated approach in a phased manner with training and simulation ensures the capability is developed within each region or business unit.