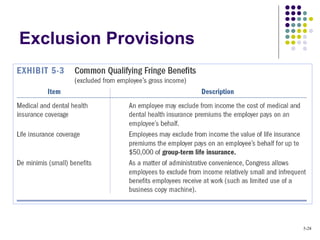

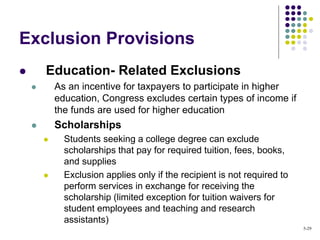

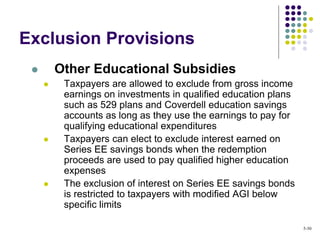

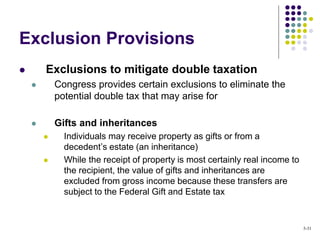

This chapter discusses gross income and exclusions. It defines gross income for tax purposes and explains when taxpayers recognize income. It discusses the various sources of income, including income from services, property, annuities, and other sources. It also covers the major exclusion provisions that allow taxpayers to exclude or defer certain types of income from gross income, such as municipal bond interest, home sale gains up to $250,000, education-related exclusions, and foreign earned income up to $97,600.

![ Foreign earned income

A maximum of $97,600 (2013) of foreign earned income can be

excluded from gross income for qualifying individuals

A maximum of $13,664 (2013) of employer-provided foreign

housing also may be excluded (but only to the extent that costs

exceed $15,616 (2013))

To be eligible for the foreign earned income and housing

exclusions, the taxpayer must be a resident or live in the foreign

country for 330 days in a consecutive 12-month period

Example: Courtney is considering a one-year rotation in one of EWD’s

overseas offices where she will be paid $120,000 for 340 days in residence.

How much income can Courtney exclude in 2013?

Ans: $90,915 [$97,600 full exclusion × 340/365 (days in foreign

country/days in year)].

Exclusion Provisions

5-33](https://image.slidesharecdn.com/acct-321-chapter5-140523090302-phpapp01/85/ACCT321-Chapter-05-33-320.jpg)