Download to read offline

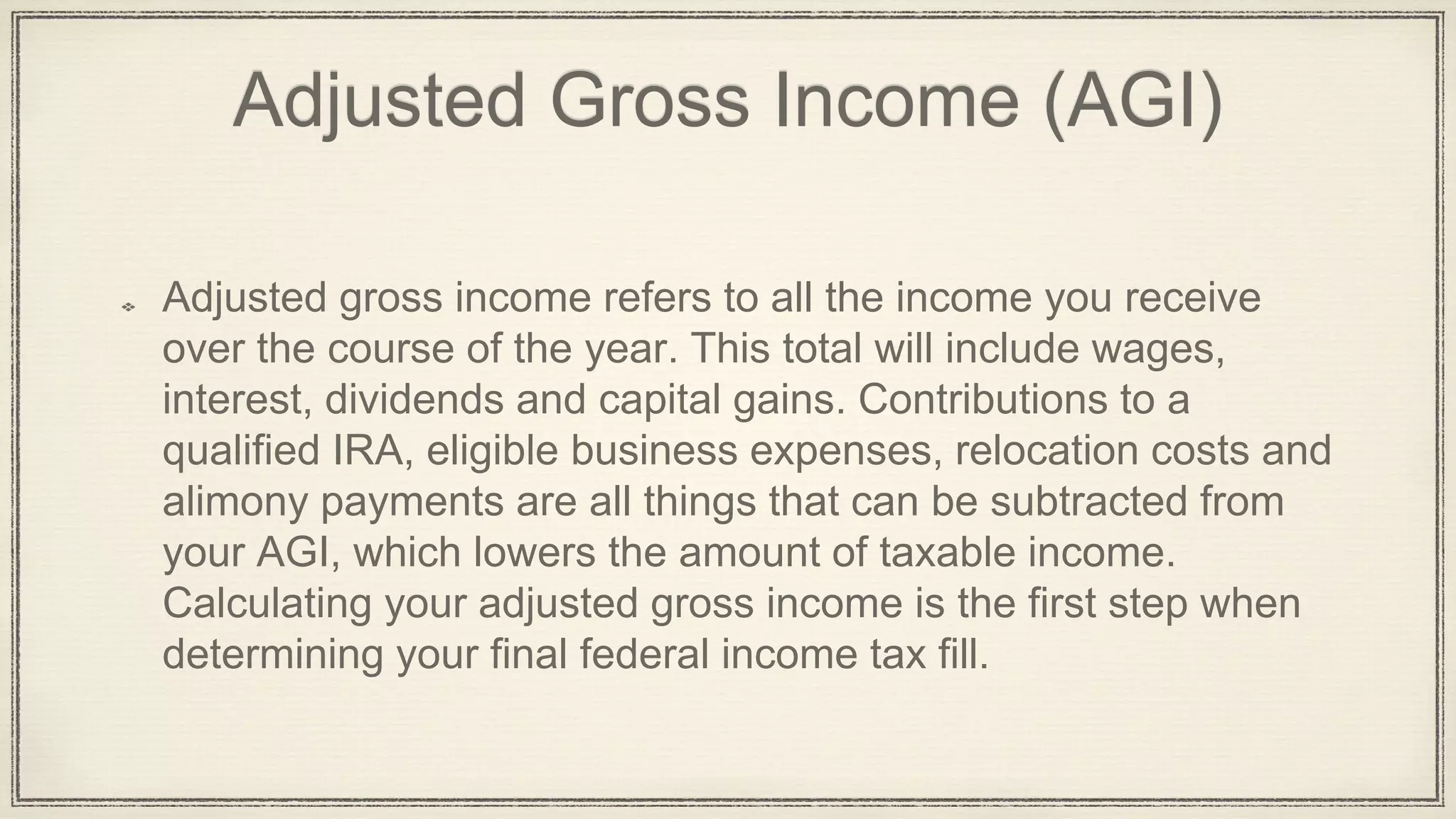

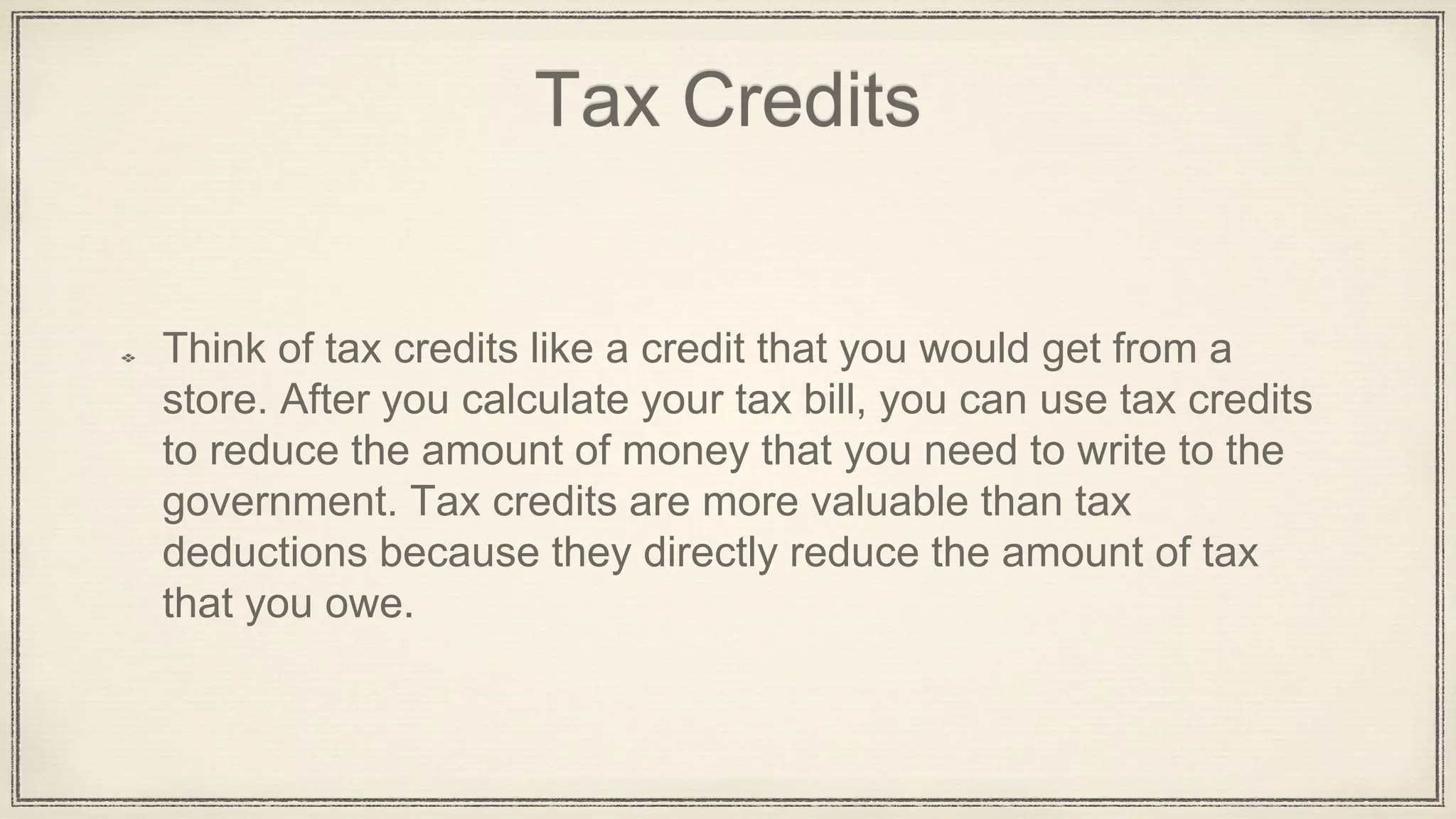

The document defines key tax terms to help understand filing taxes. It explains that adjusted gross income includes all income minus certain deductions like IRA contributions and alimony payments. Tax credits directly reduce taxes owed, while deductions lower taxable income. Itemized deductions subtract expenses from adjusted gross income. Standard deductions are fixed amounts subtracted based on filing status. Exemptions subtract amounts for dependents. The U.S. uses progressive taxation where higher incomes face higher tax rates. Taxable income is the final amount used to calculate taxes owed after deductions and exemptions. Withholding takes taxes from paychecks throughout the year. Voluntary compliance refers to taxpayers honestly reporting income.