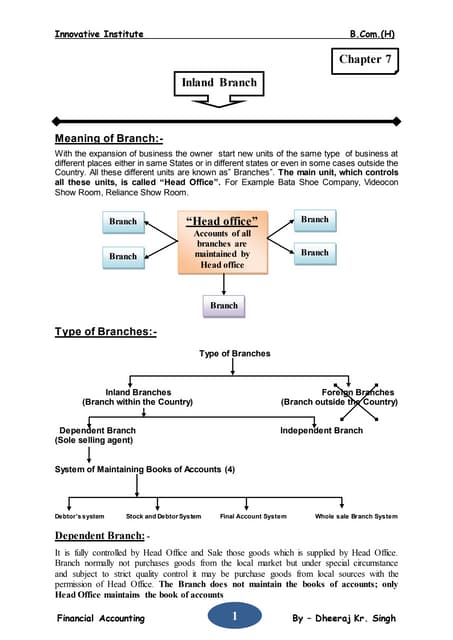

This document discusses accounting for branches and divisions of a business entity. It defines branches and divisions as separate economic units from the home office, but not separate legal entities. Branches carry out sales and collections at a distance from the home office. Divisions have more autonomy than branches. The document outlines different accounting systems and ledger accounts used by branches and the home office to record transactions between them. It provides an example to illustrate the journal entries and combined financial statements for a home office and its branch.