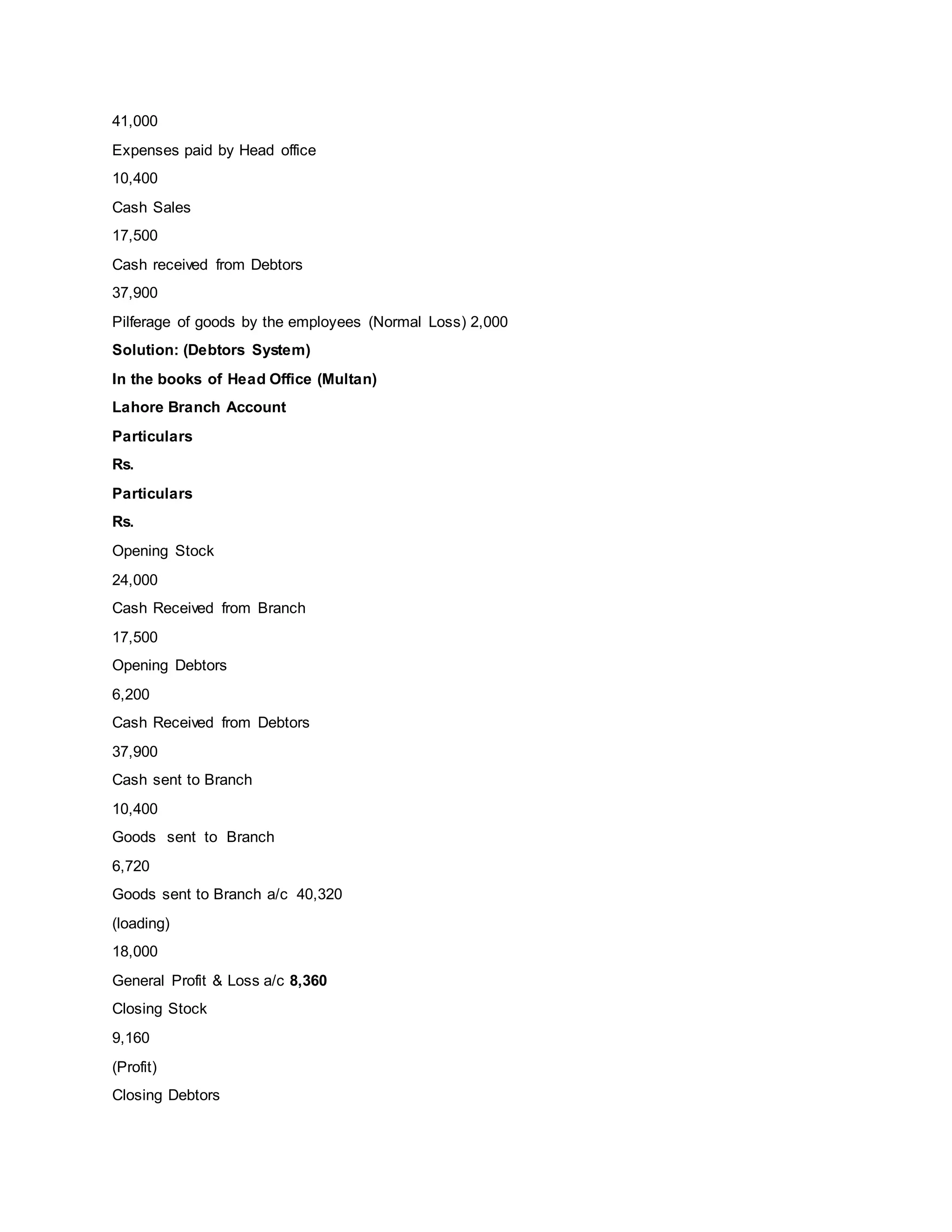

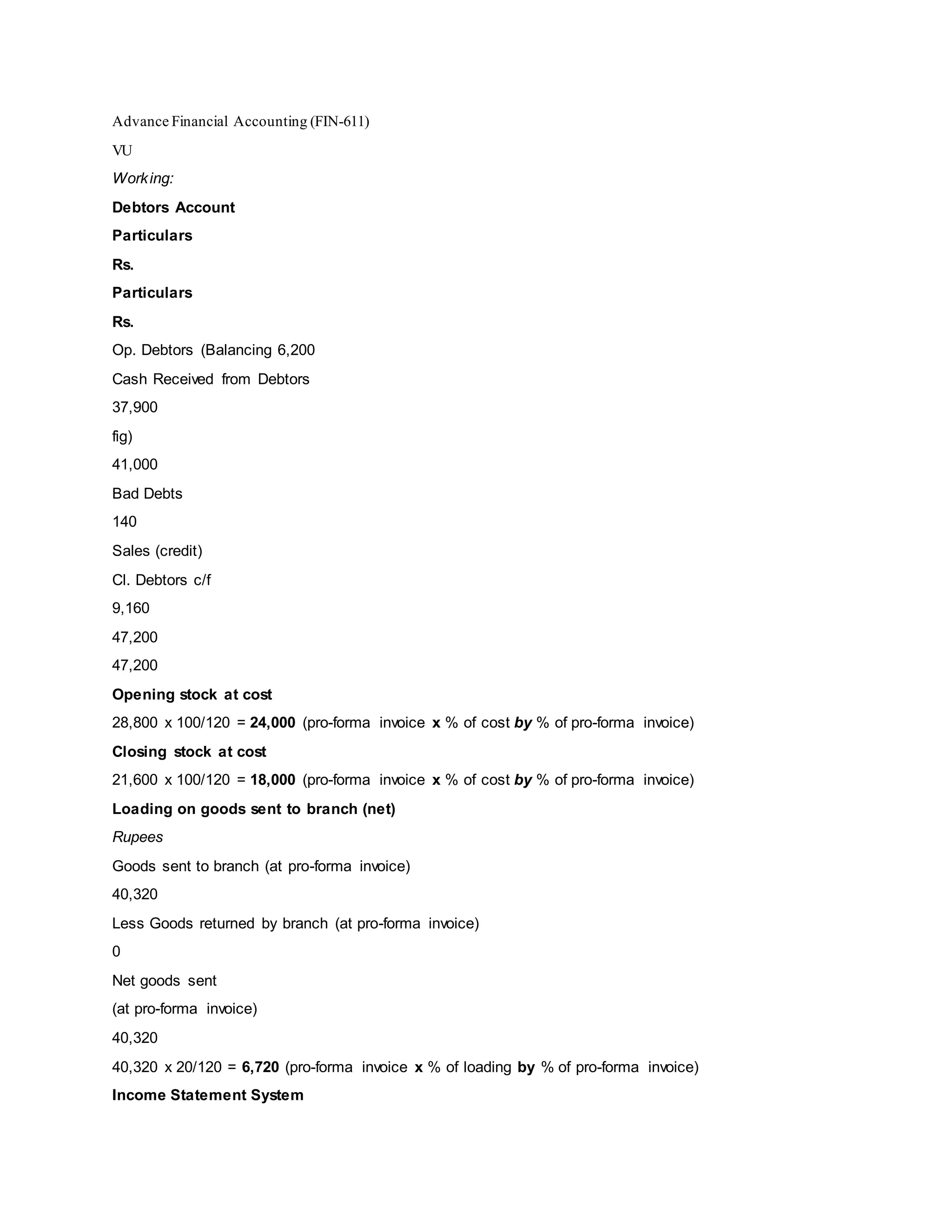

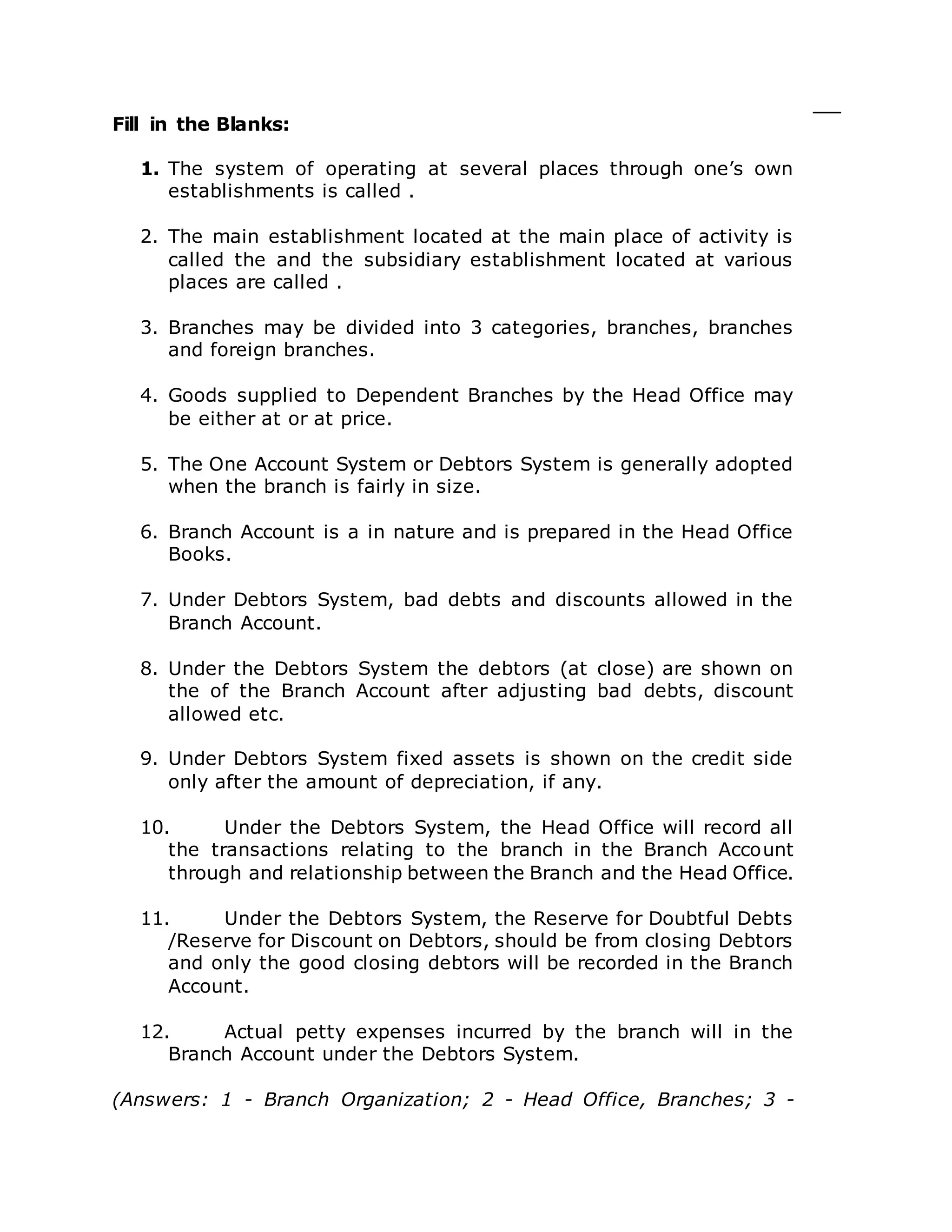

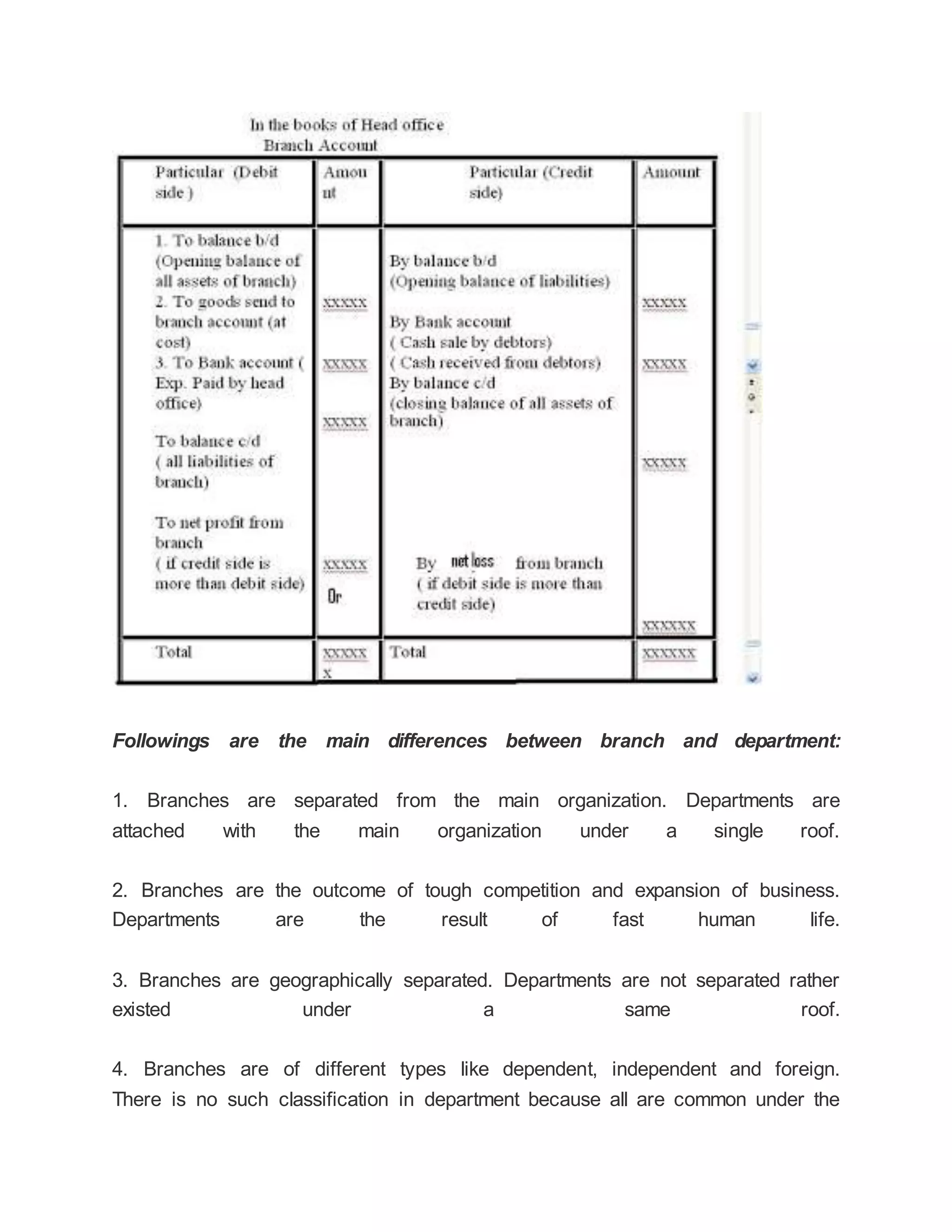

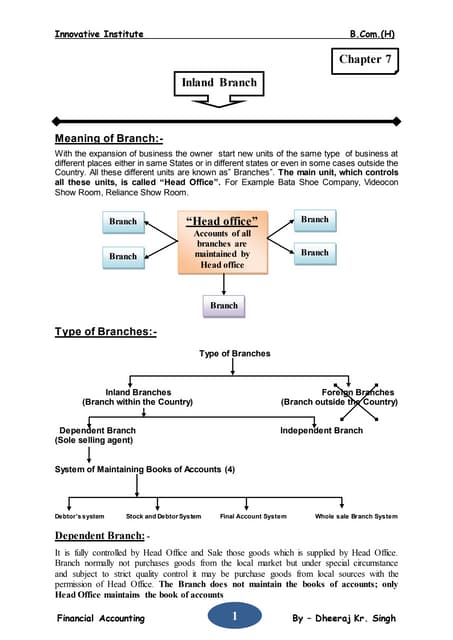

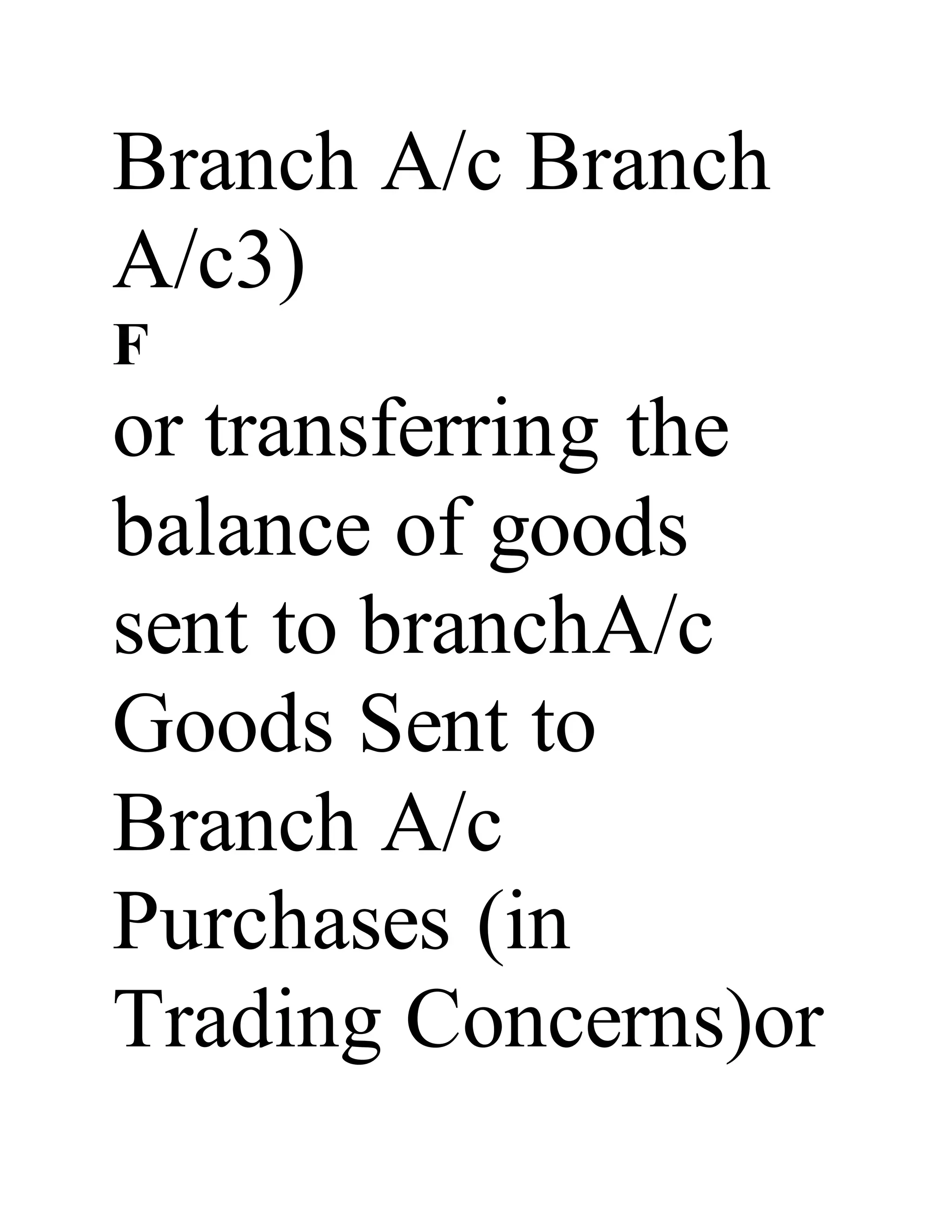

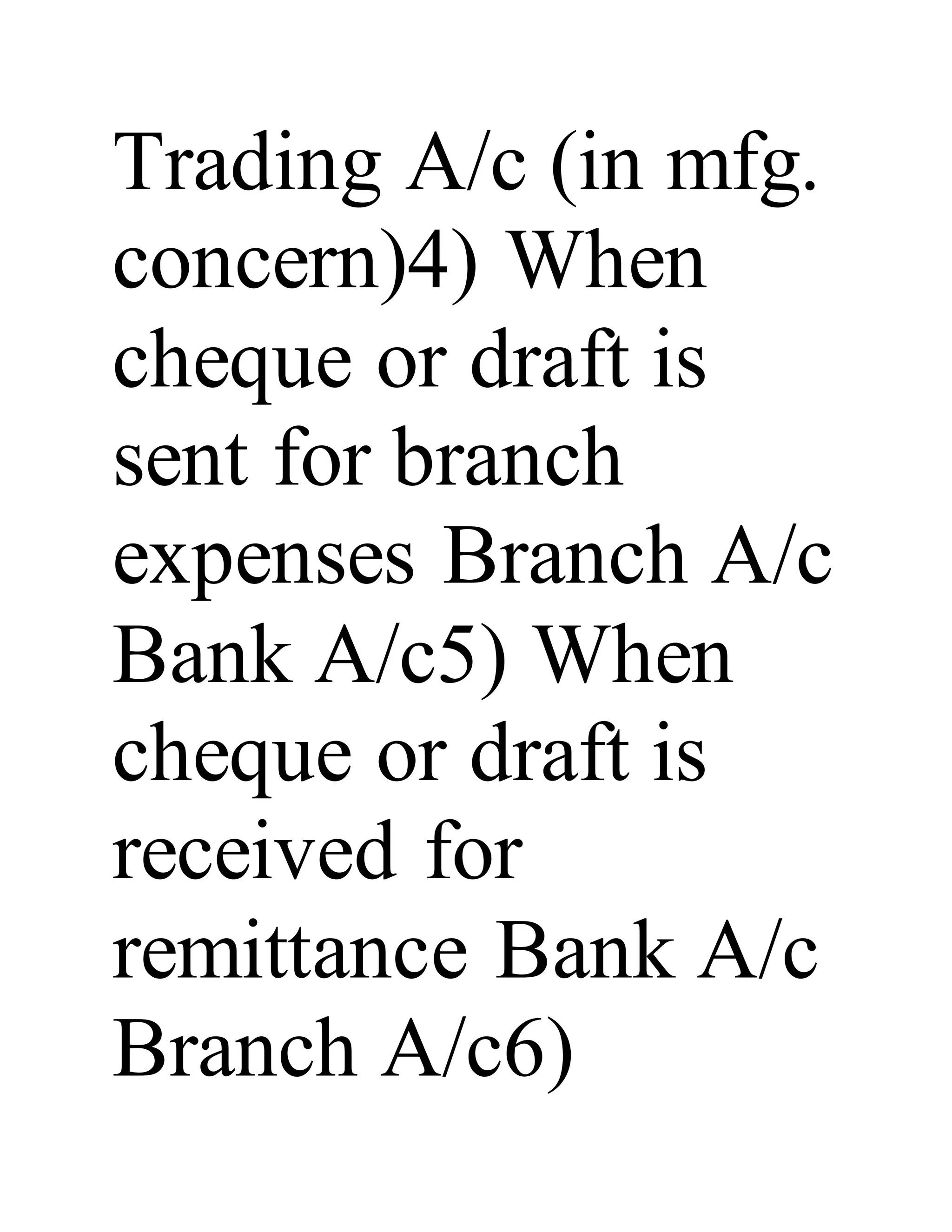

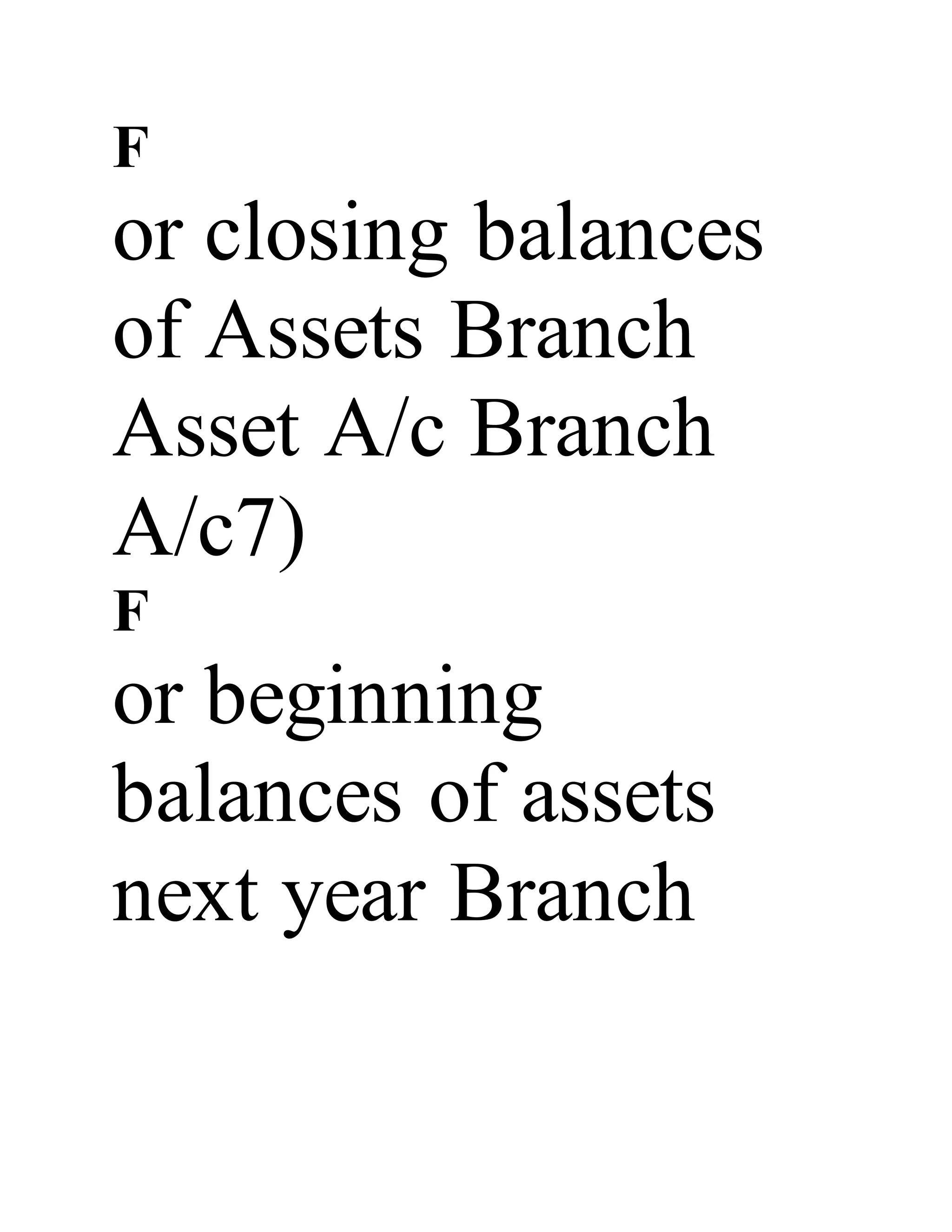

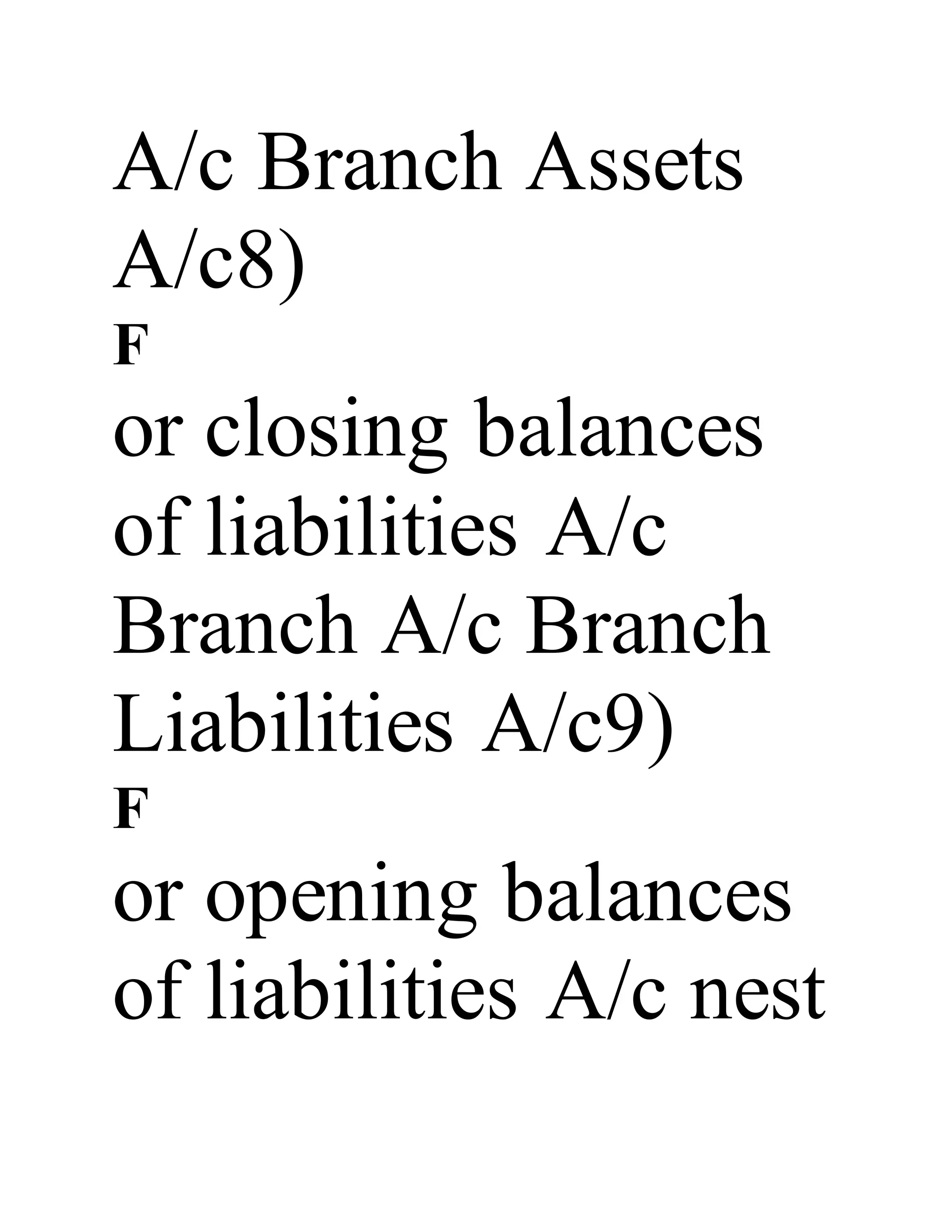

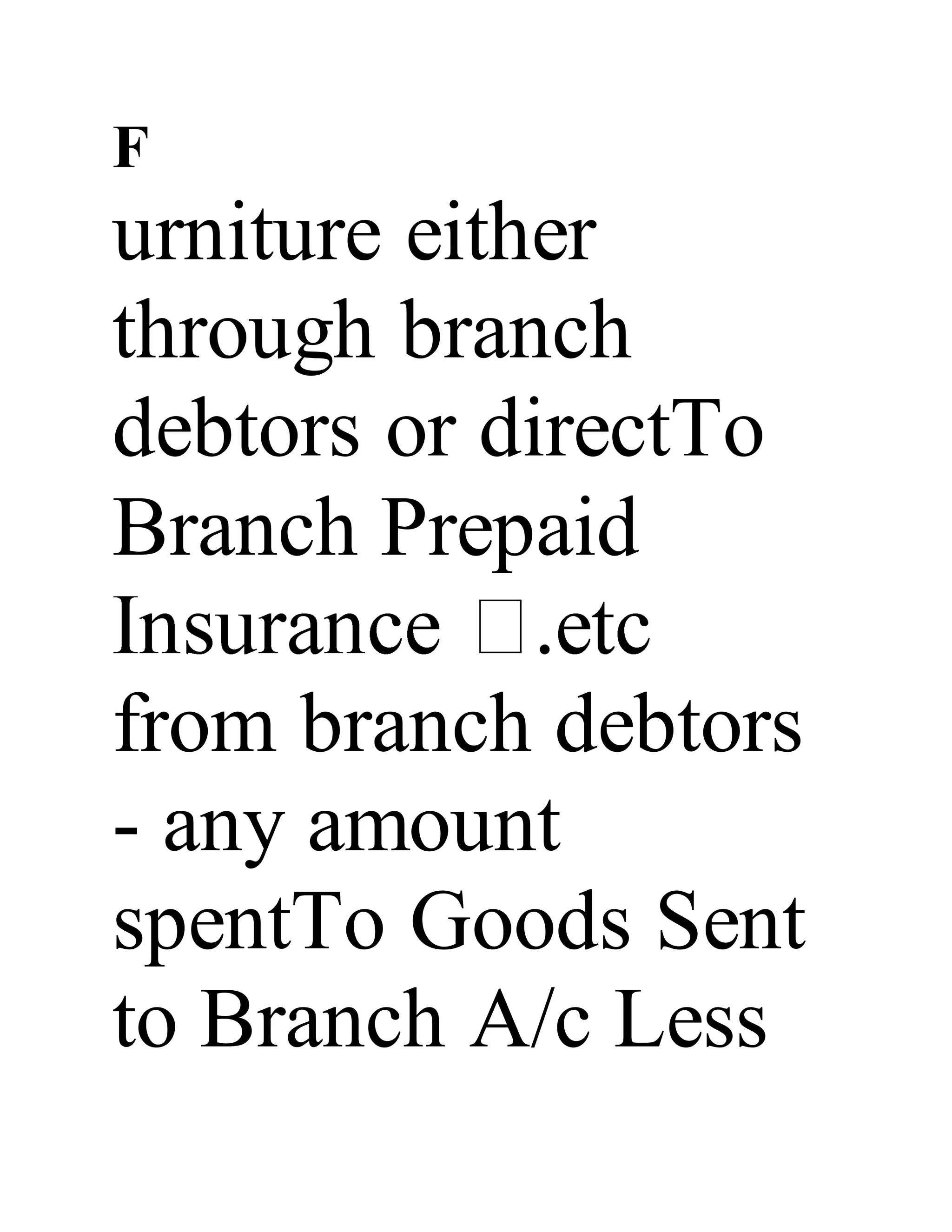

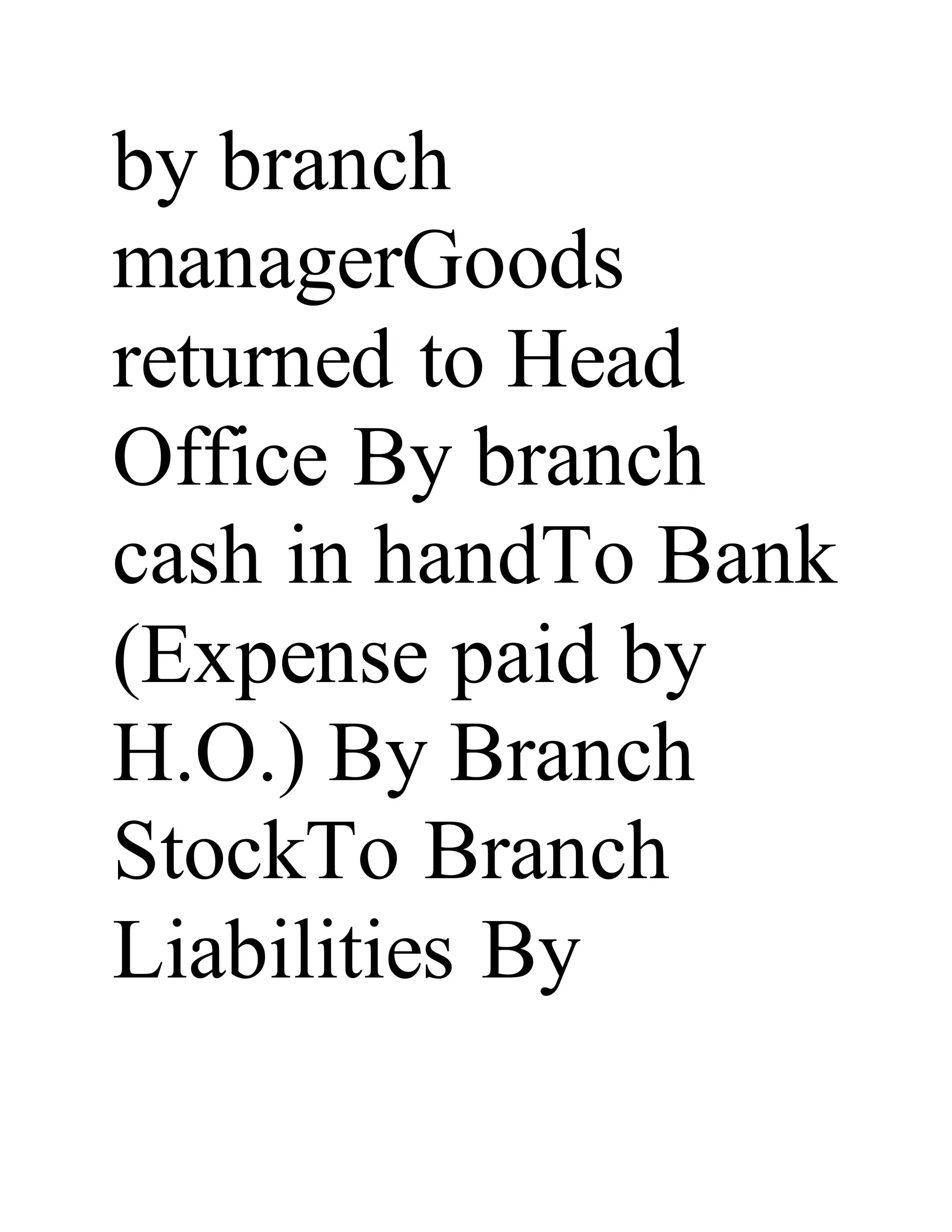

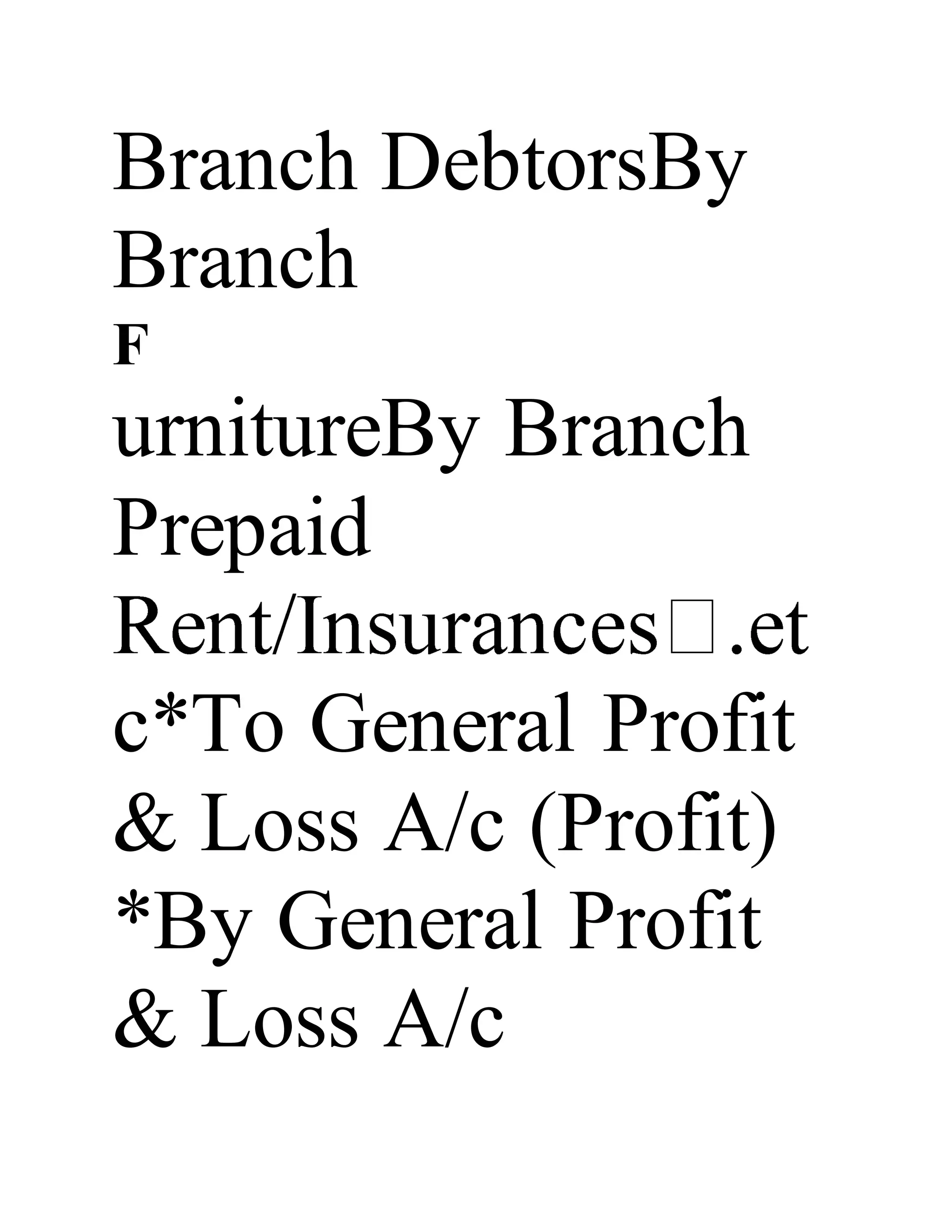

This document discusses different methods for accounting for branch operations in the books of the head office, including the debtor system, final account system, and stock and debtors system. The debtor system records branch transactions through a branch account in the head office books. The final account system determines branch profit/loss through a branch trading and profit/loss account. The stock and debtors system provides more detailed information on branch assets, liabilities, debtors, and inventory movements.

![Post notePost reviewPost replyPost note and like

1 hundred reads

1 thousand reads

Junior Isidro Luna liked this

ningegowda liked this

ningegowda liked this

Rwambo Rpc liked this

kevinlim186 liked this

Rukiya Shuaib liked this

kevinlim186 liked this

Sanjeev Gangwal liked this

Load more

Similar to Branch Accounting

Branch Accounting

bilalyasir

BRANCH ACCOUNTS

tanuj_baru

Introduction to Branch Lecture Notes[1]

pladop

Branch Accounting

Arpita Rathore](https://image.slidesharecdn.com/branchaccounts-150716065836-lva1-app6891/75/Branch-accounts-slide-share-106-2048.jpg)

![40711339-Branch-Accounting[1].pdf

fareh19

Branch Accounting

Iqra Mughal

47 Branch Accounts

Shivaram Krishnan

Branch Accounting

Sheniel Stephens

Accounting for Branches and Combined FS

Muhammad Fahad

Branch Accounts (Theory & Problems)

Amit Batra

Journal Entries for Receivables

Mary

Download and print this document

Read and print without ads

Download to keep your version

Edit, email or read offline

Choose a format:

.DOCX .PDF .TXT

Download

Recommended](https://image.slidesharecdn.com/branchaccounts-150716065836-lva1-app6891/75/Branch-accounts-slide-share-107-2048.jpg)

![Branch Accounting

bilalyasir

Advanced Accounting Branch Accounting, Branch Accounting, Presentation Branch...

BRANCH ACCOUNTS

tanuj_baru

Introduction to Branch Lecture Notes[1]

pladop

Branch Accounting

Arpita Rathore

Previous|NextPage 1 of 3

Read Unlimited Books for $8.99 per month

Start your free 14 days

No commitment.Cancel anytime.

“Movie lovers have Netflix, music lovers have Spotify — and book lovers (whether they read

literary fiction or best-selling potboilers) now have Scribd.”– NPR

“[Scribd] is a place where you can browse and skim and read whatever strikes your fancy…”–

Wired

“For less than the price of buying one new book a month (e- or otherwise), you can wander

through more than 50,000 books.”– Entrepreneur

“This has got to be the next best thing to sliced bread. I can finish reading one book and go grab

another instantly”– Wendy Brooks, a Scribd reader](https://image.slidesharecdn.com/branchaccounts-150716065836-lva1-app6891/75/Branch-accounts-slide-share-108-2048.jpg)