Downloaded 11 times

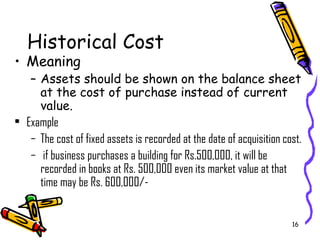

This document discusses key accounting concepts and principles: - The business entity concept treats the business and its owners as separate entities. - The historical cost principle records assets at their original cost rather than current value. - The matching principle recognizes revenues when earned and expenses when incurred to match revenues with related expenses over the same period. - The materiality concept means that only significant items are disclosed separately in financial statements.