Downloaded 32 times

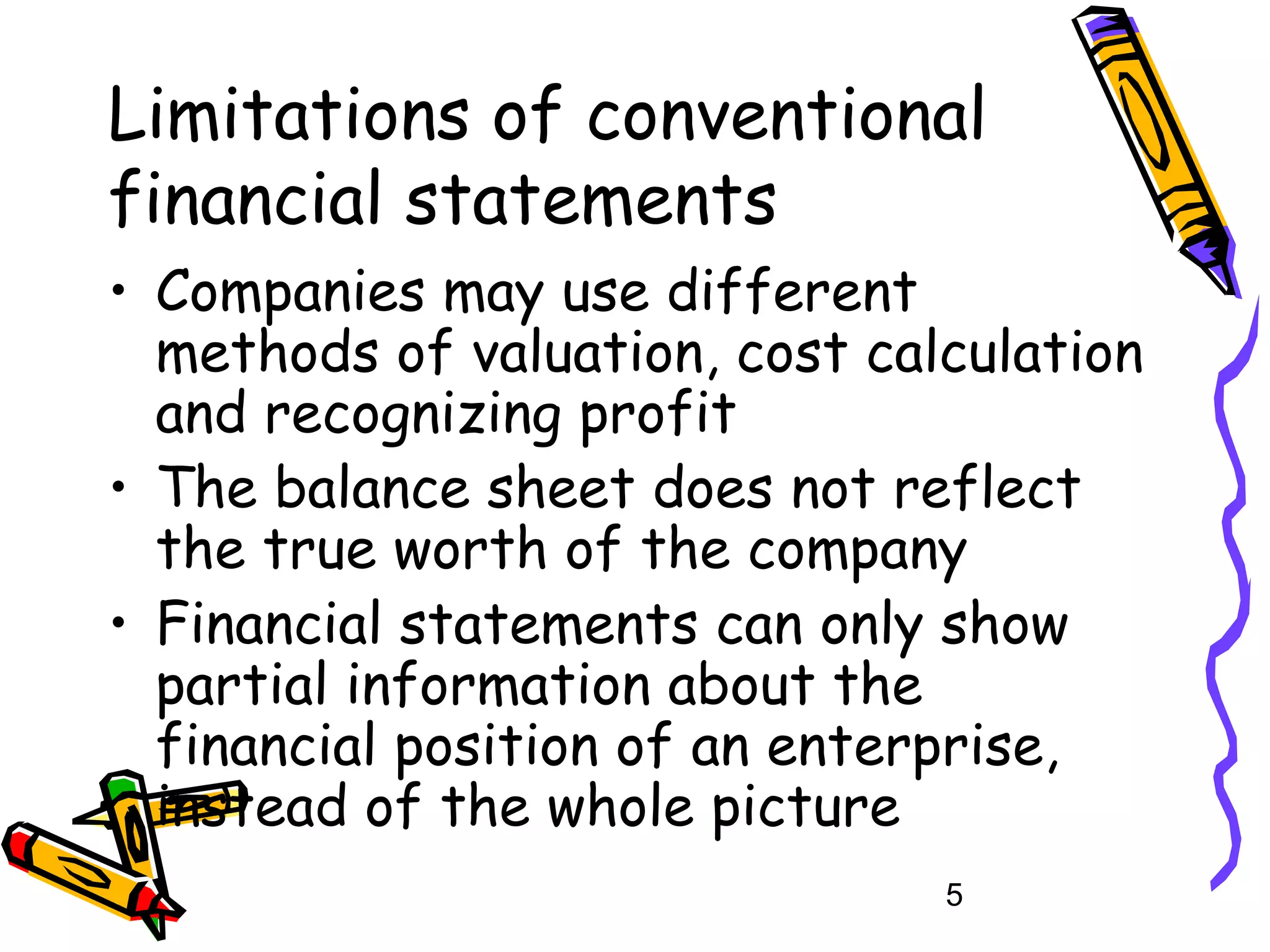

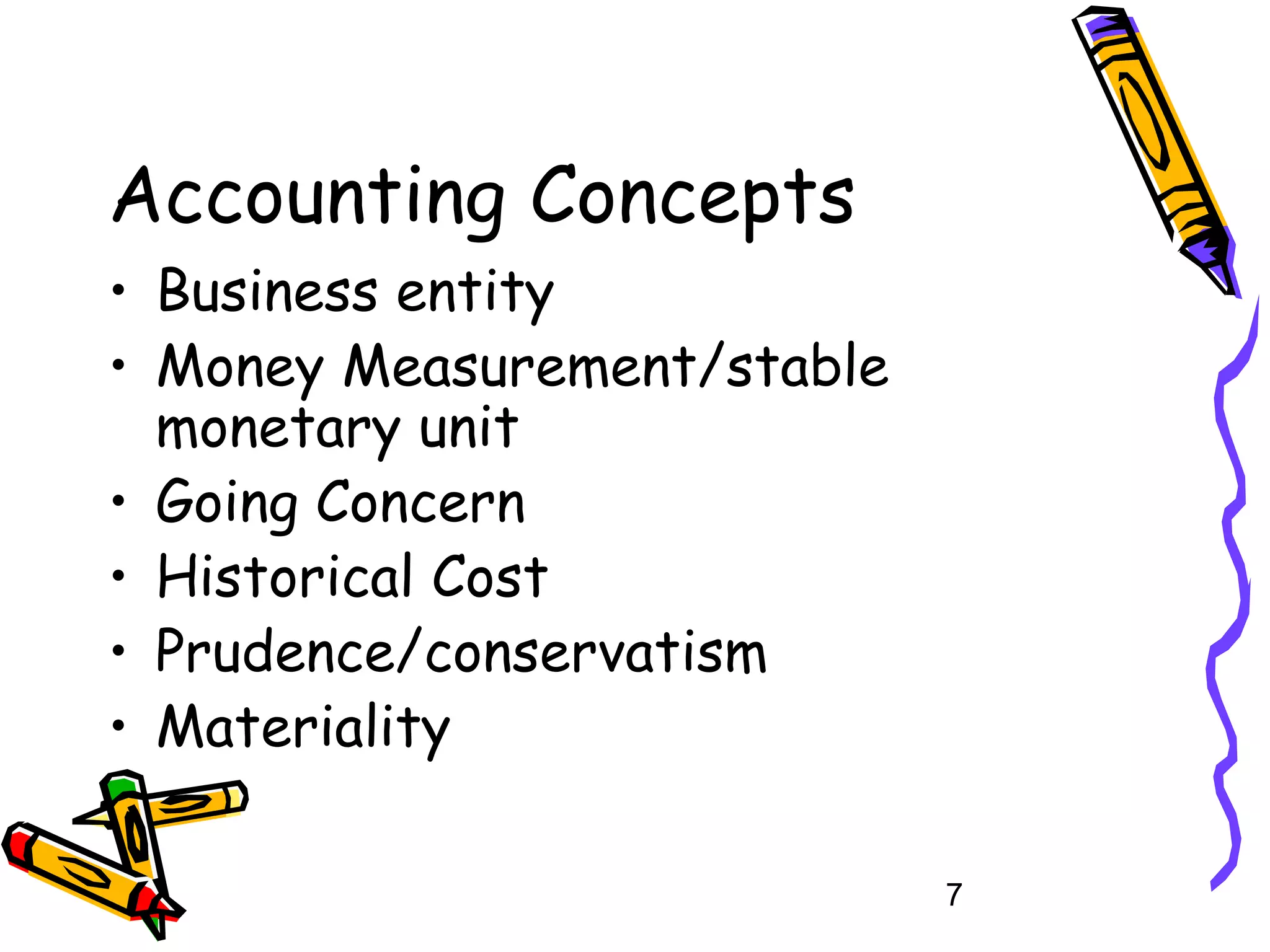

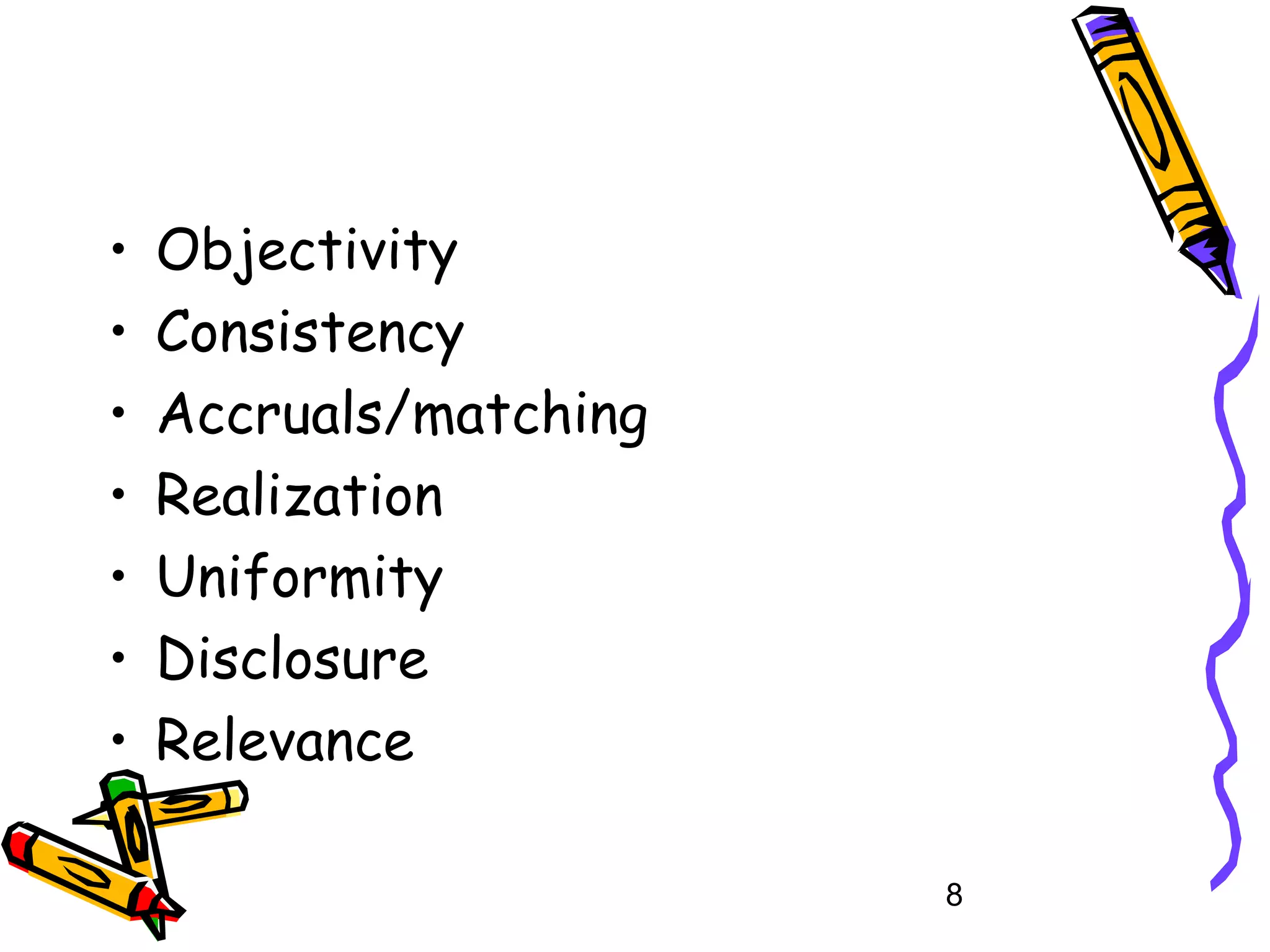

The document discusses key accounting concepts and principles such as business entity, money measurement, going concern, historical cost, prudence, materiality, objectivity, consistency, accruals/matching, realization, uniformity, disclosure, and relevance. It provides examples and explanations of how each concept is applied when preparing financial statements in accordance with generally accepted accounting principles. The concepts aim to ensure financial statements are useful, reliable and comparable.