Download to read offline

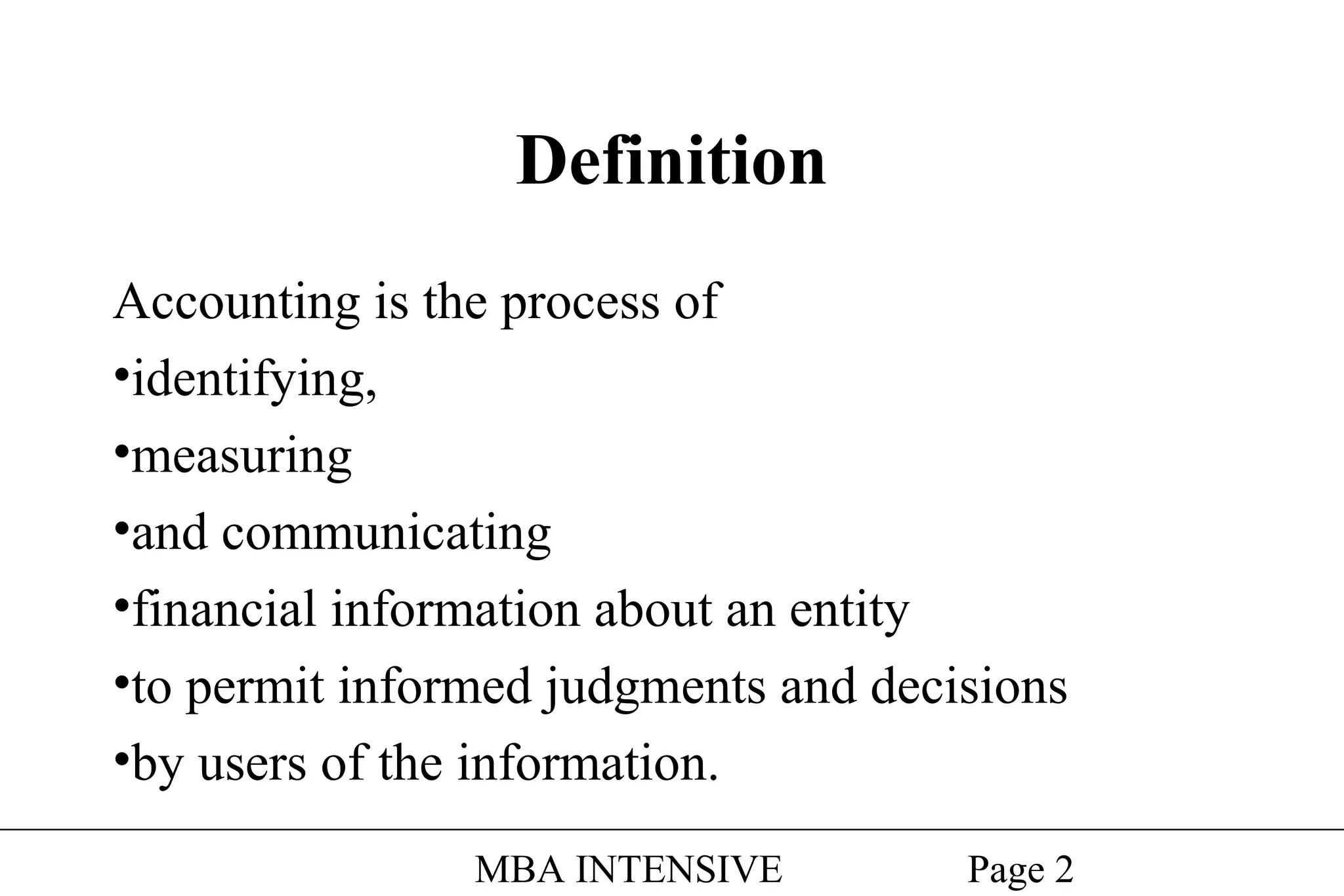

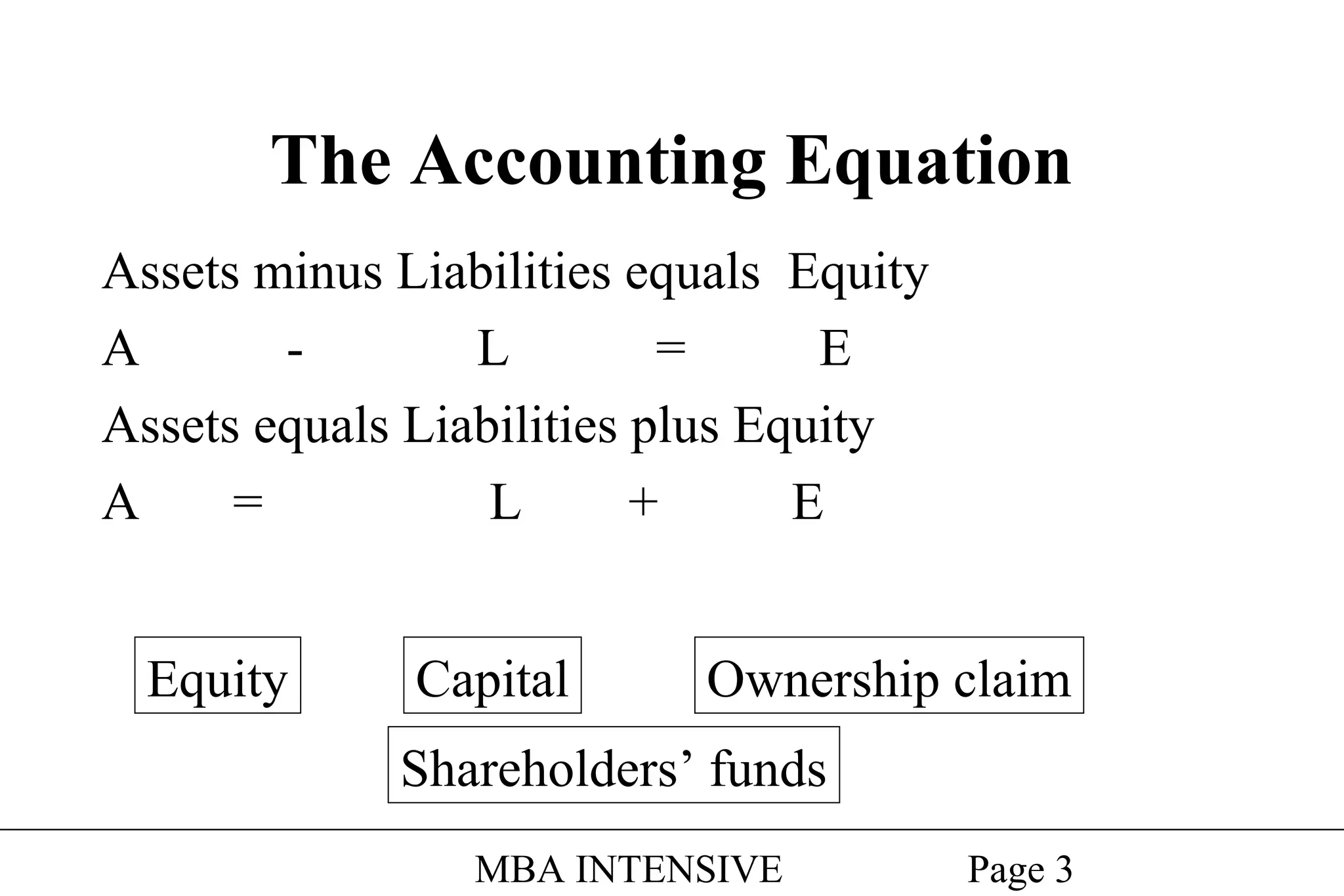

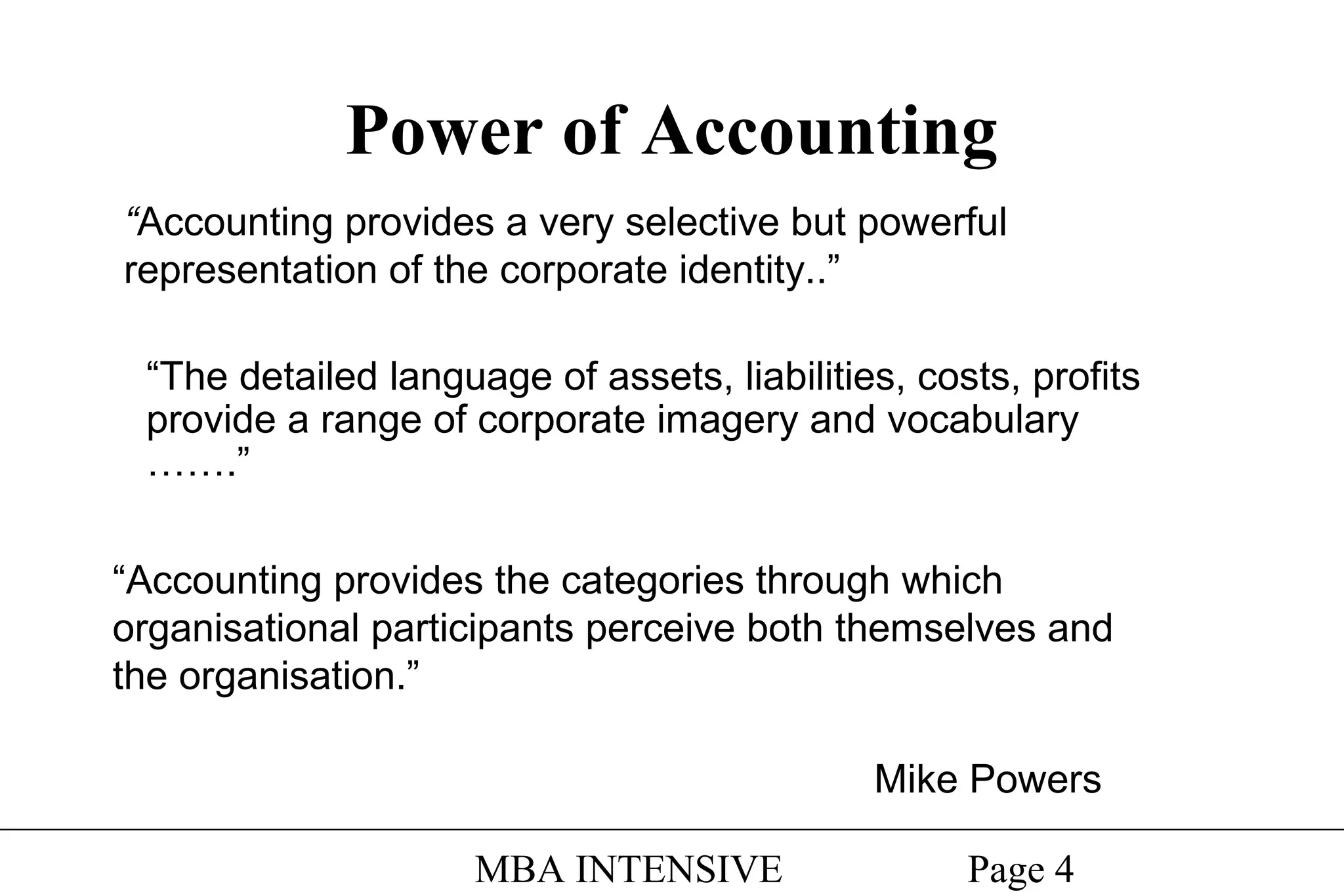

This document provides an overview of accounting and financial statement analysis. It defines accounting and describes the accounting equation and key financial statements. It discusses how accounting provides a representation of a company and can be creative. The roles and uses of accounting are outlined. The document then covers analyzing and interpreting financial statements, including calculating and using ratios to assess a company's profitability, liquidity, asset management, financial structure, and market value. Limitations of ratio analysis are also noted.