Downloaded 188 times

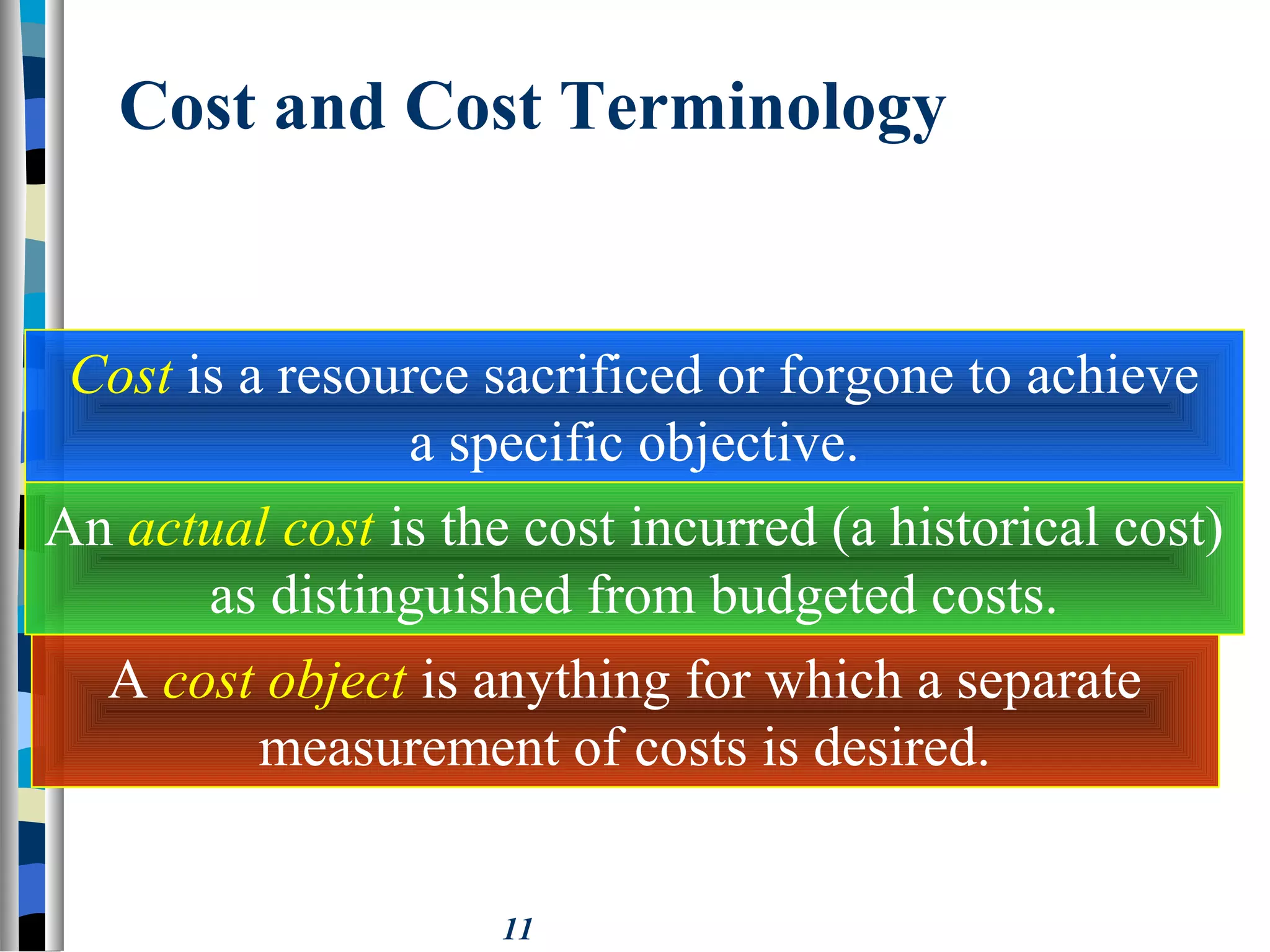

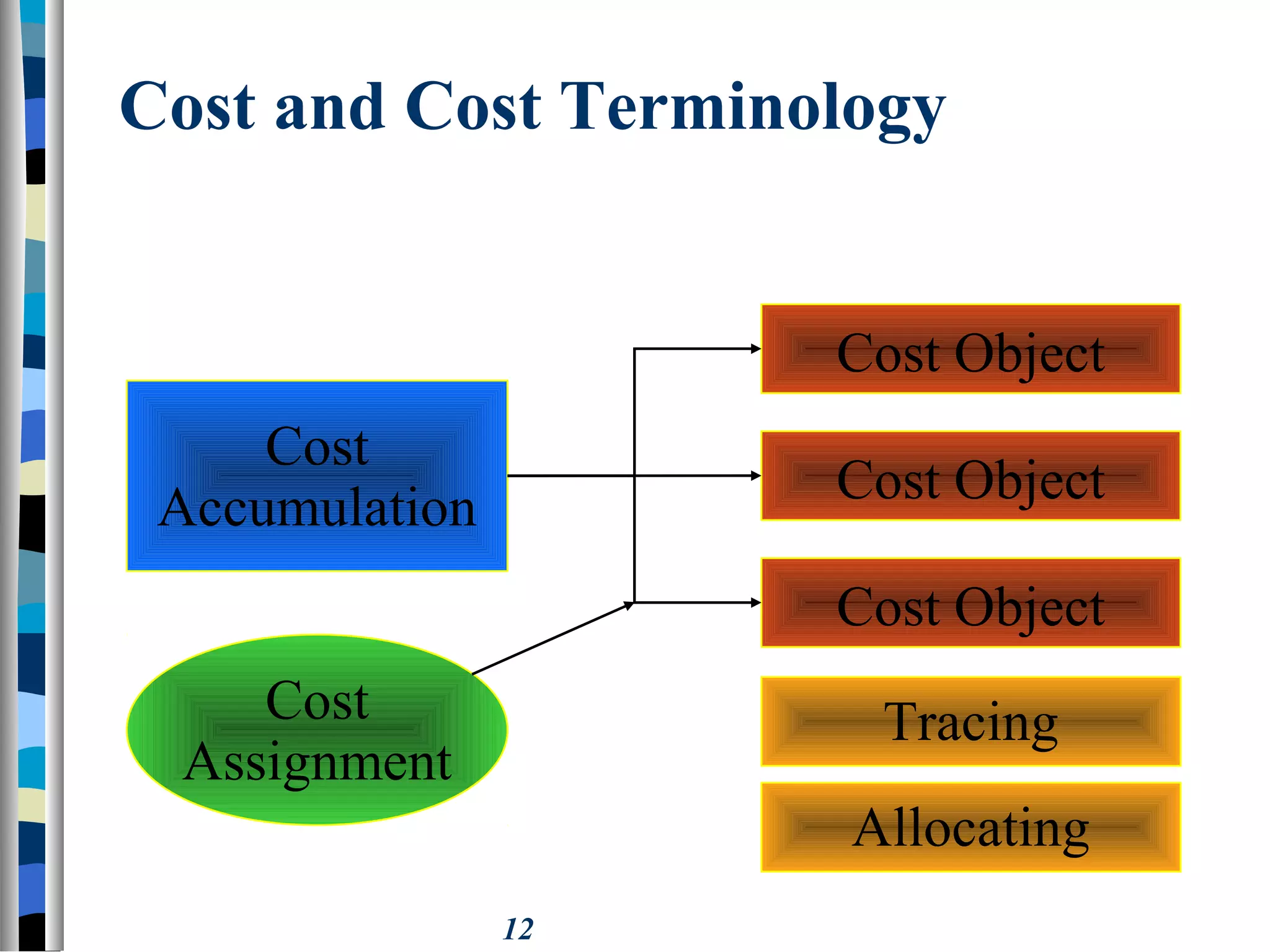

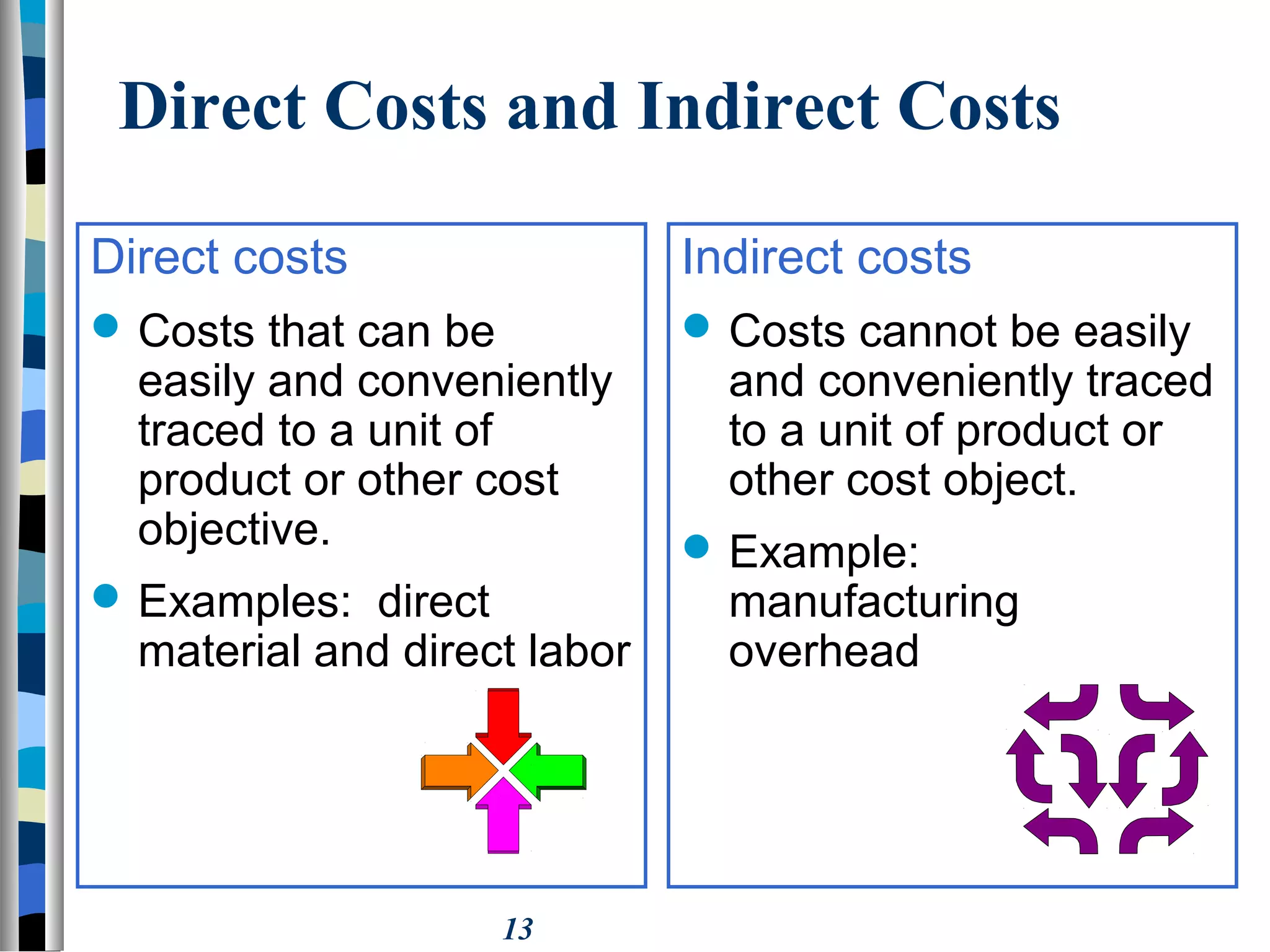

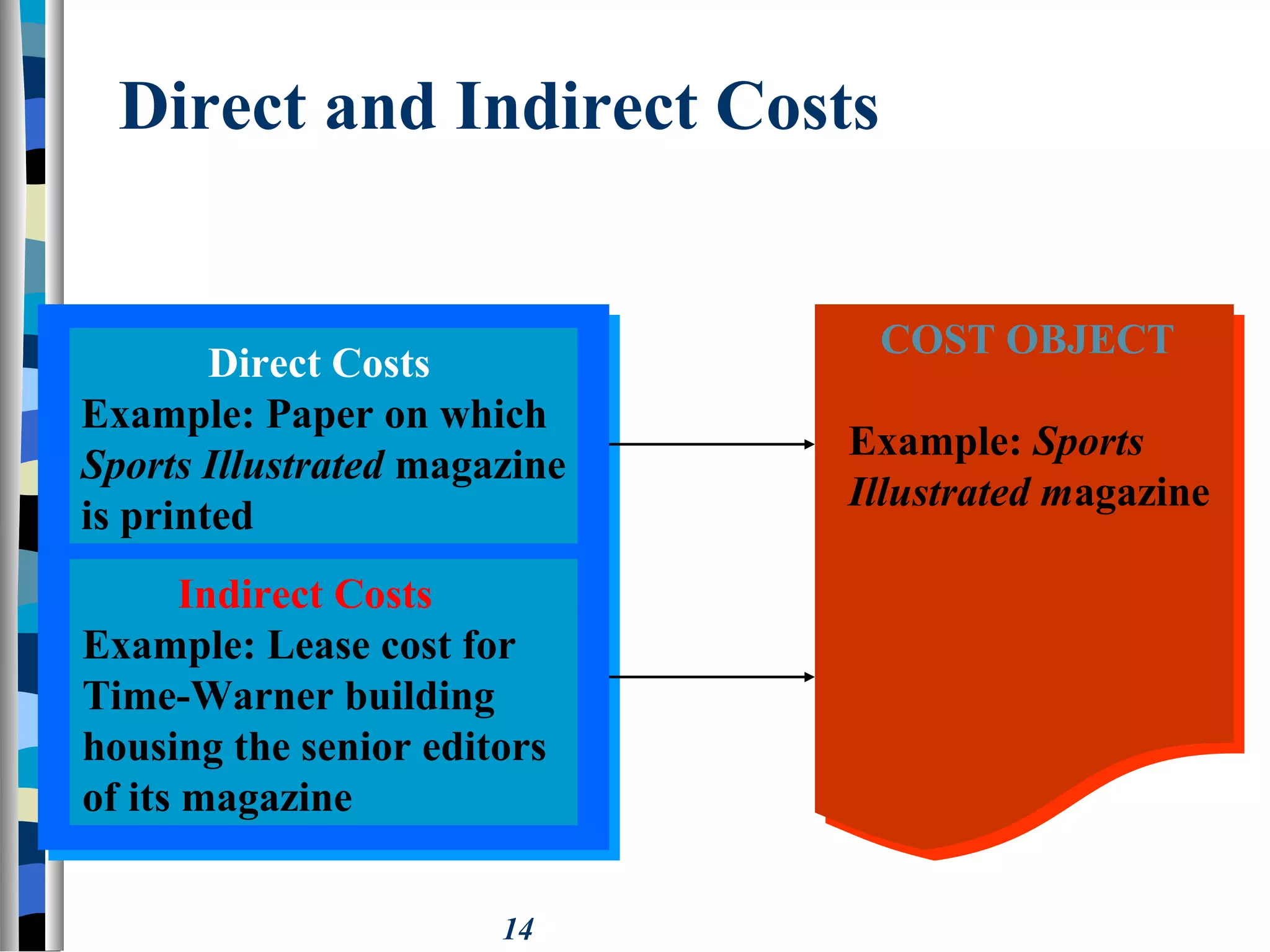

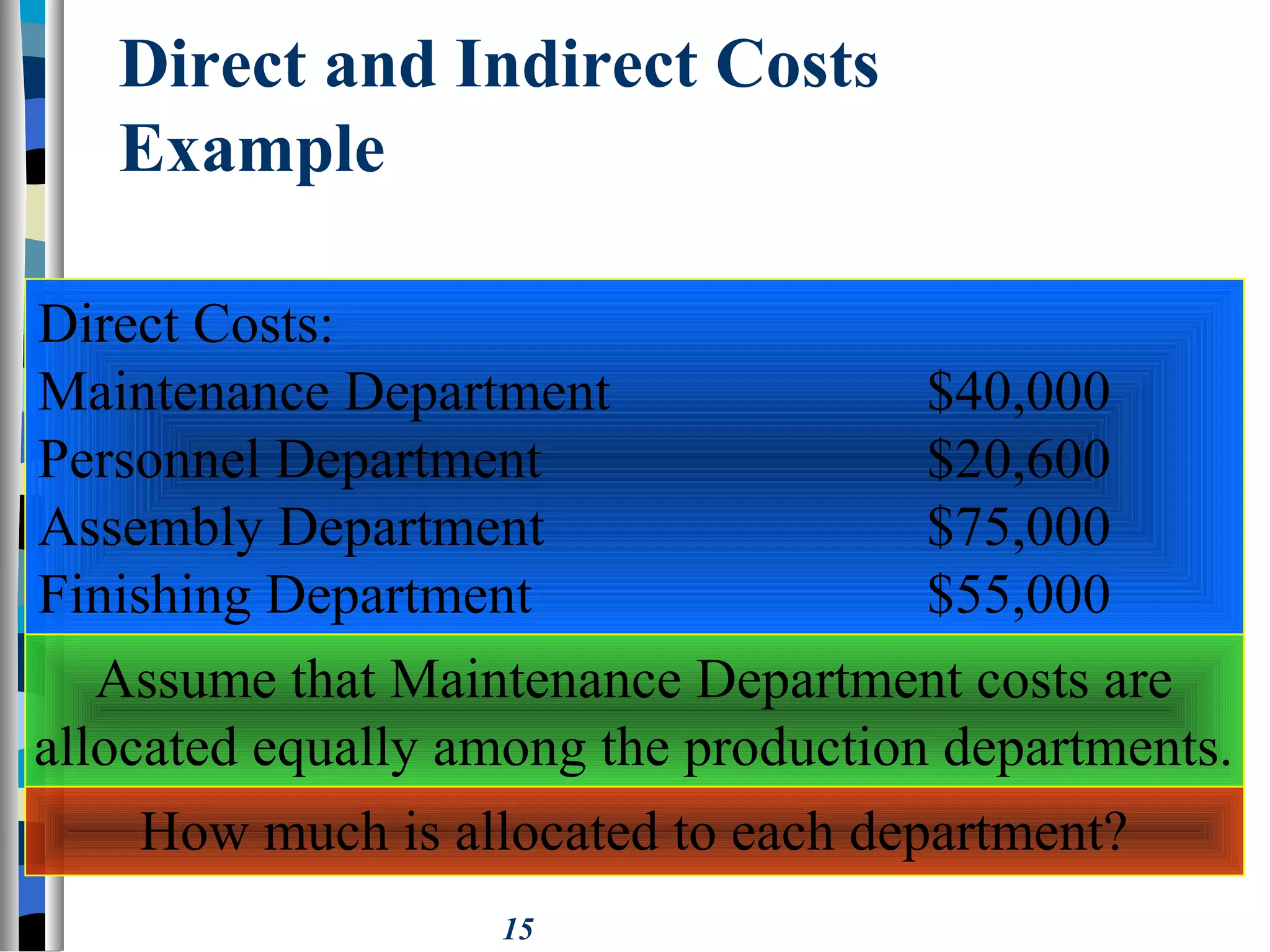

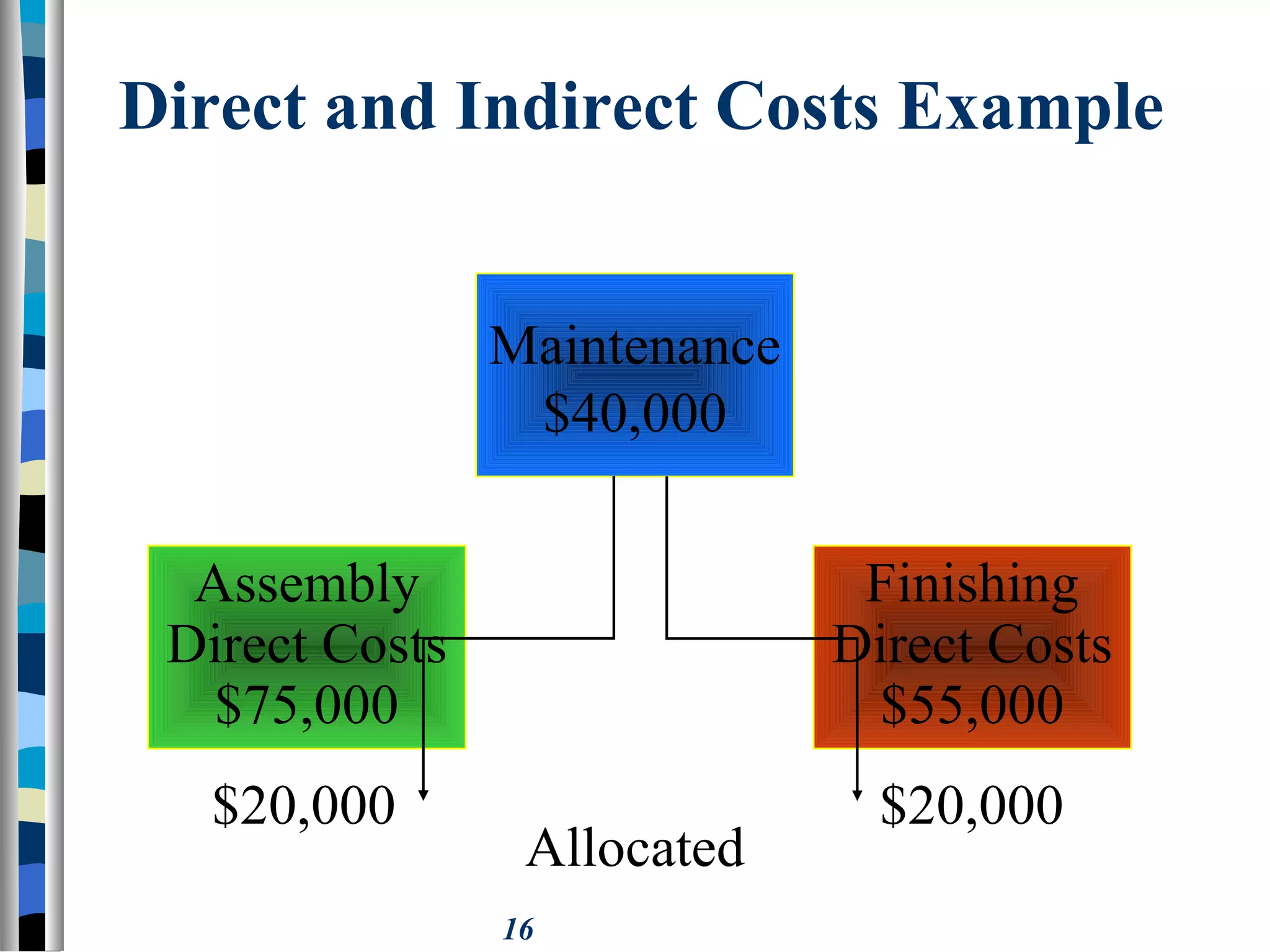

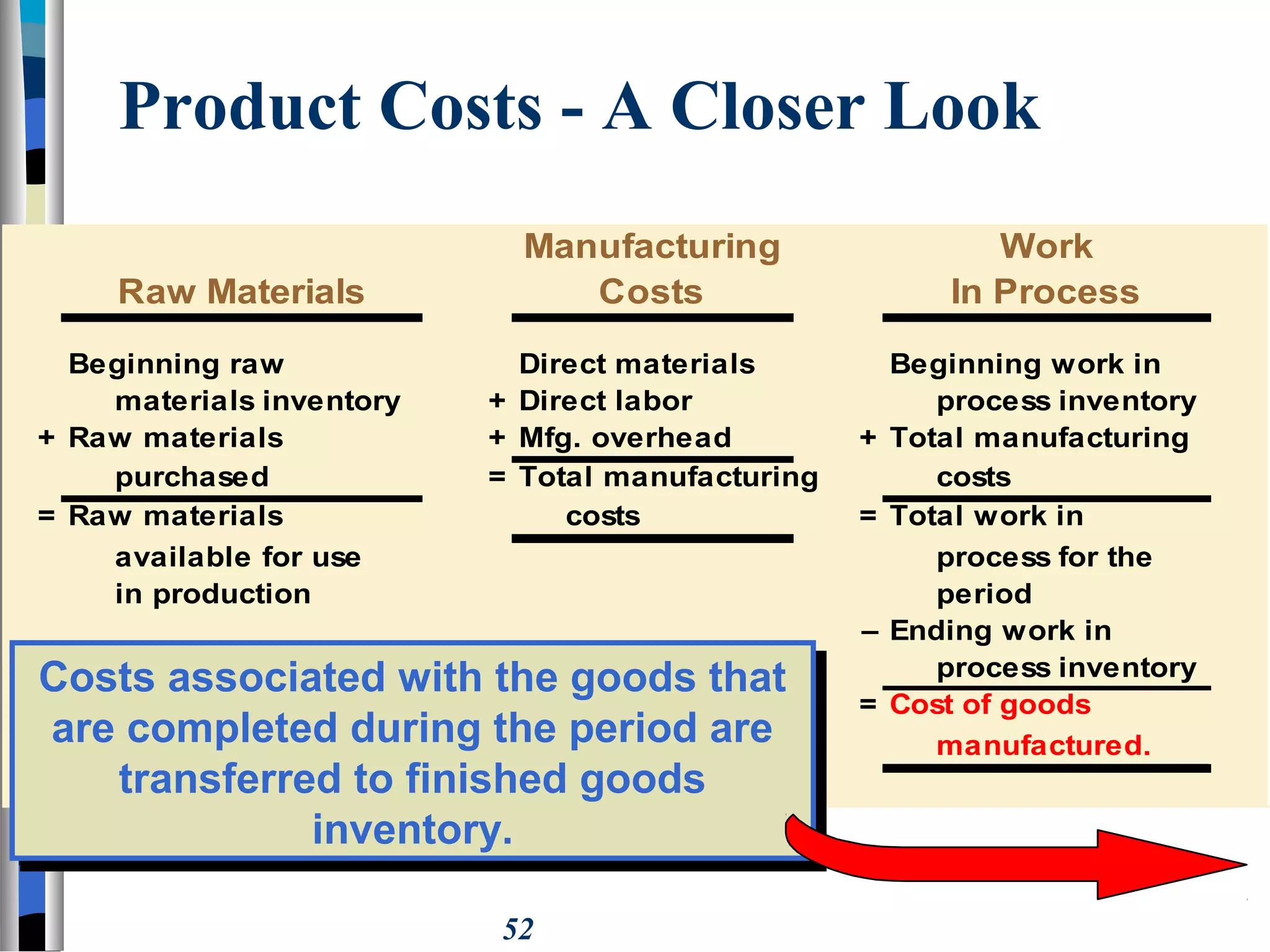

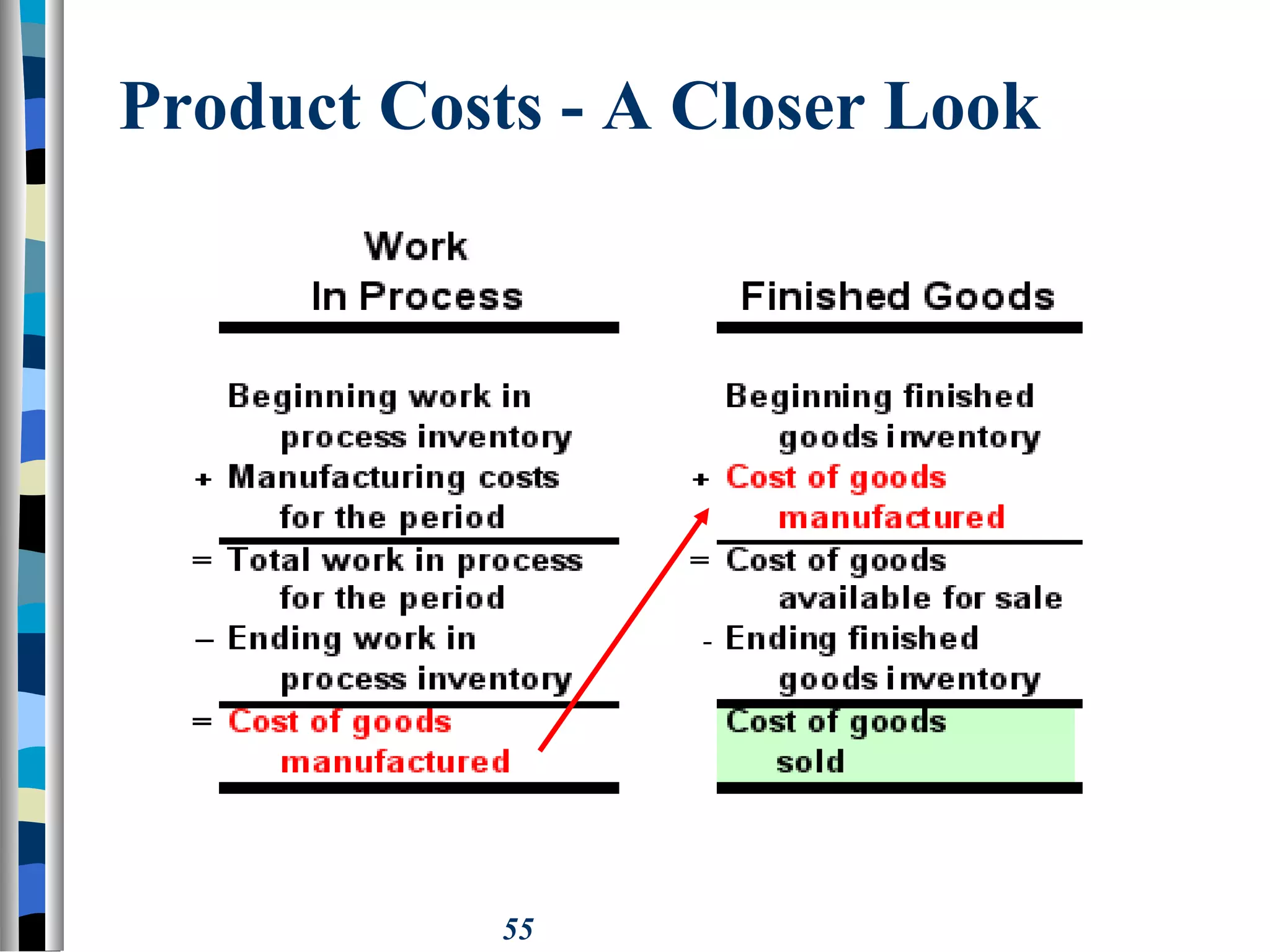

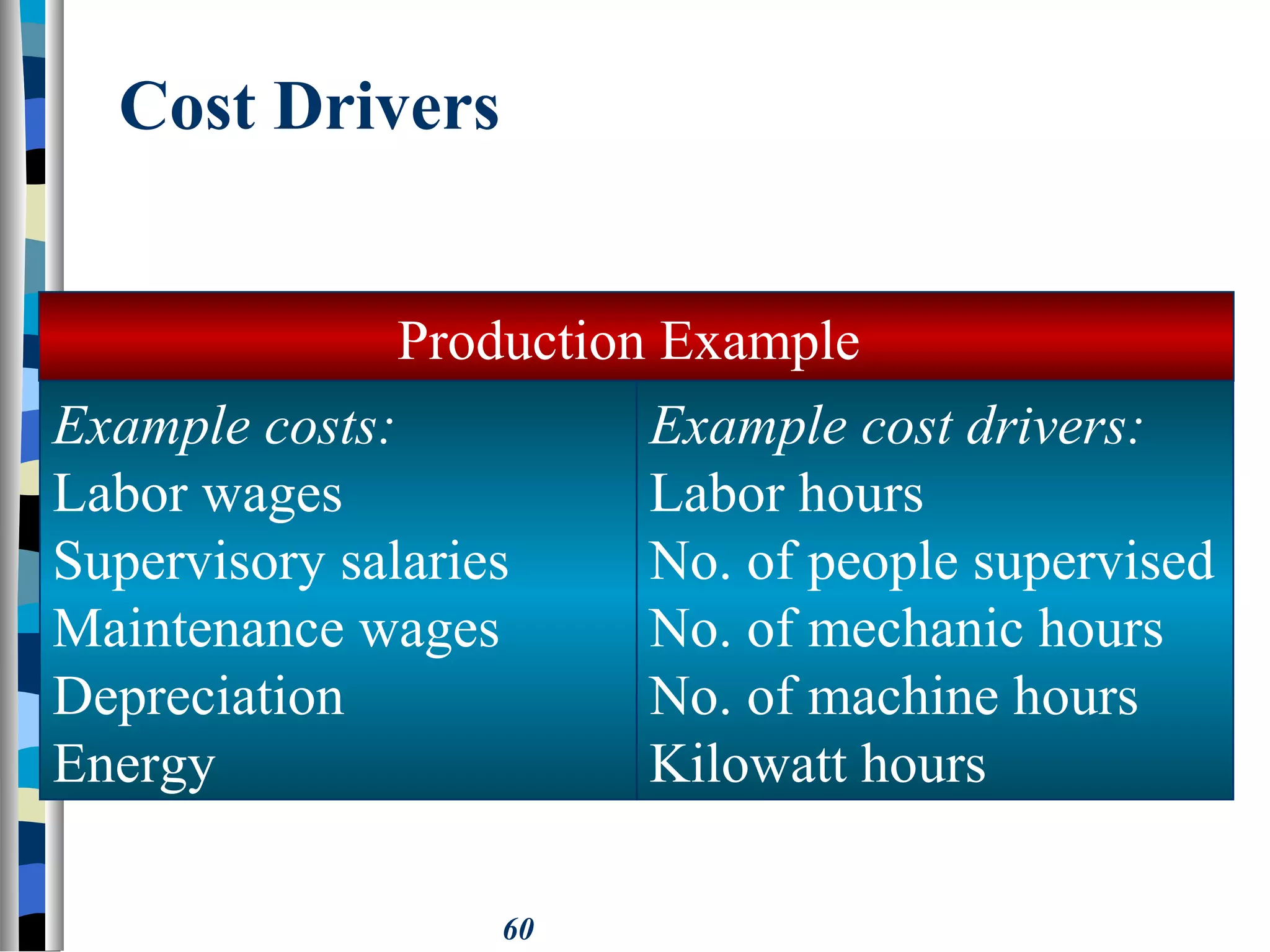

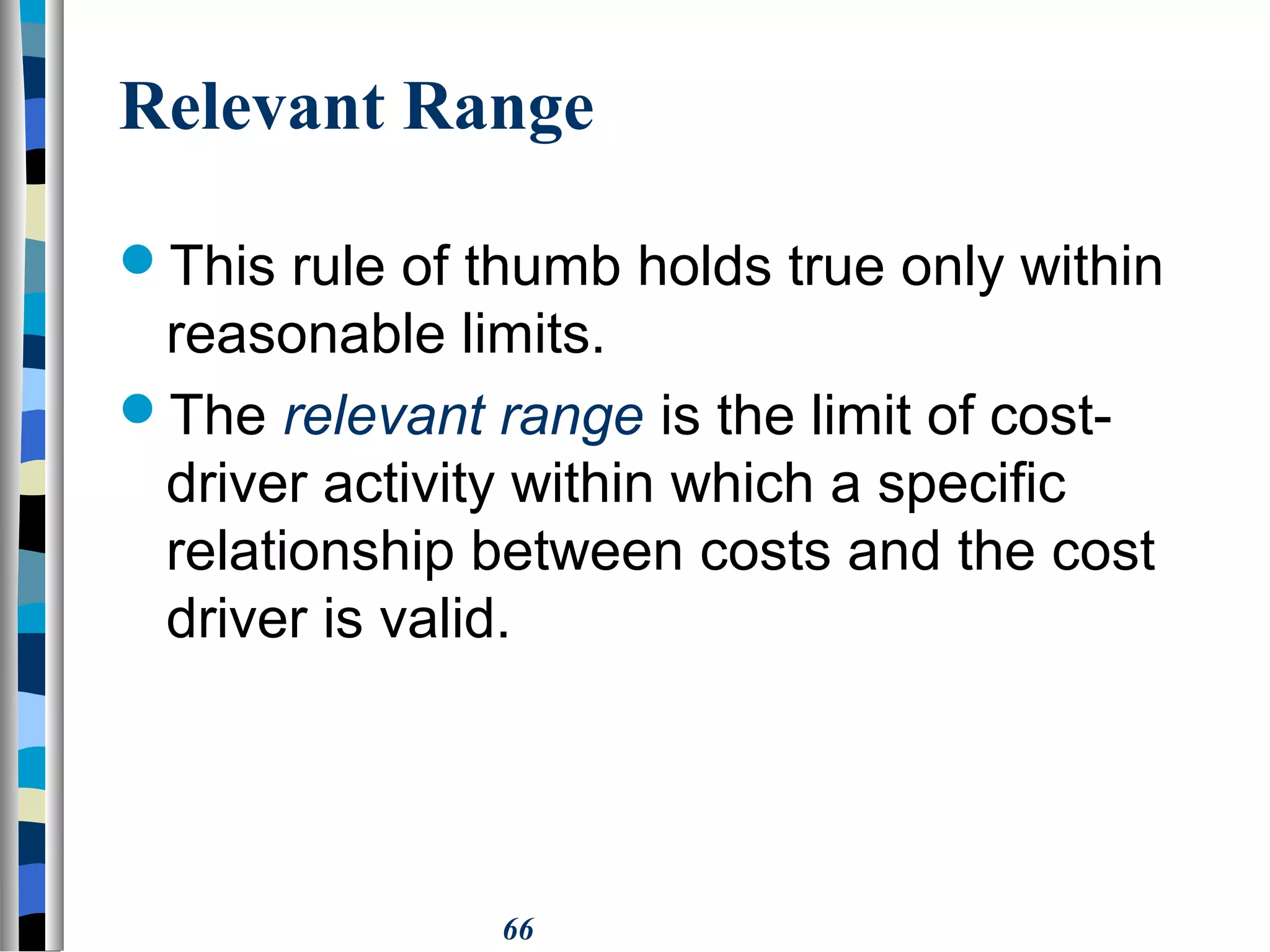

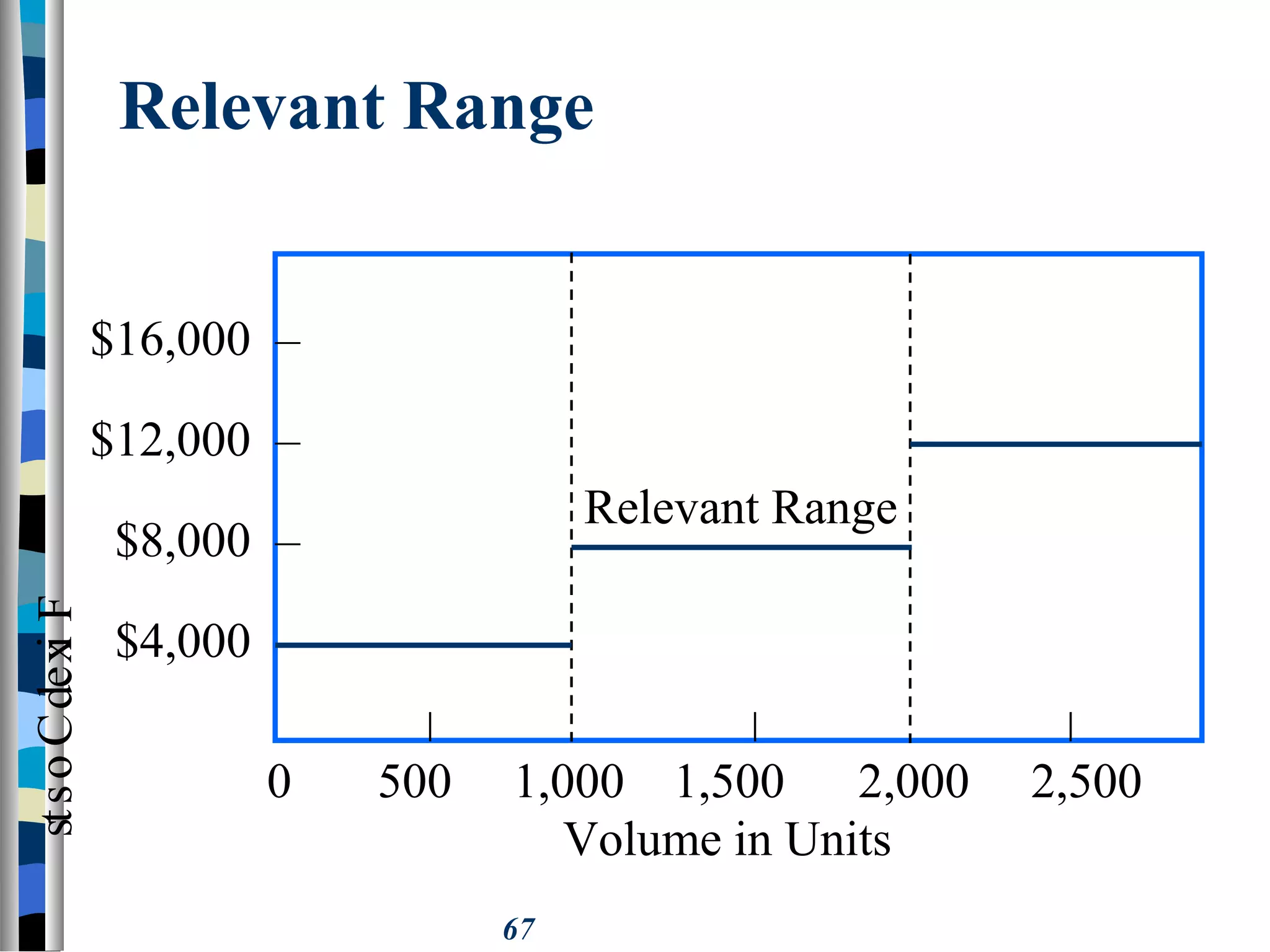

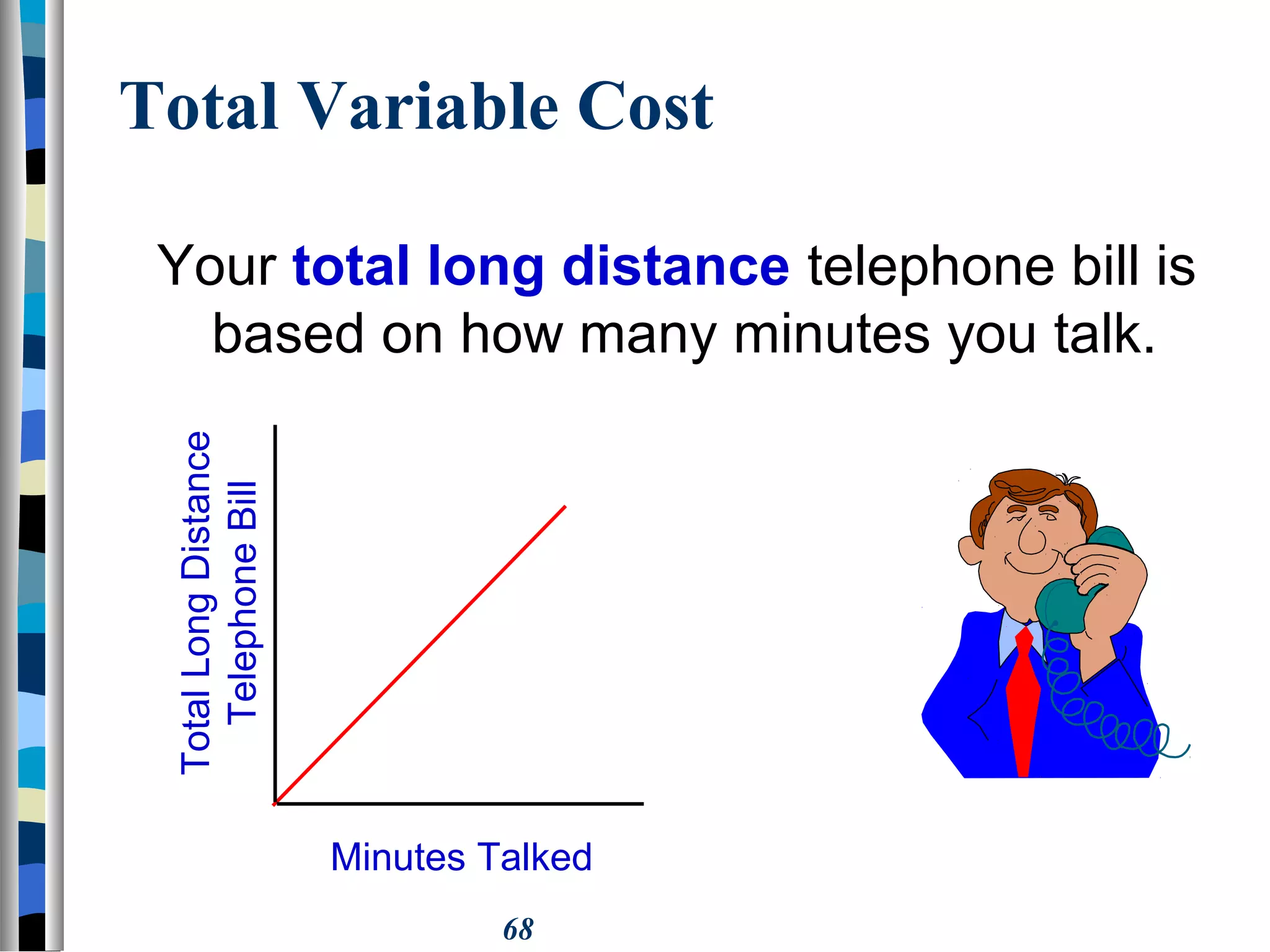

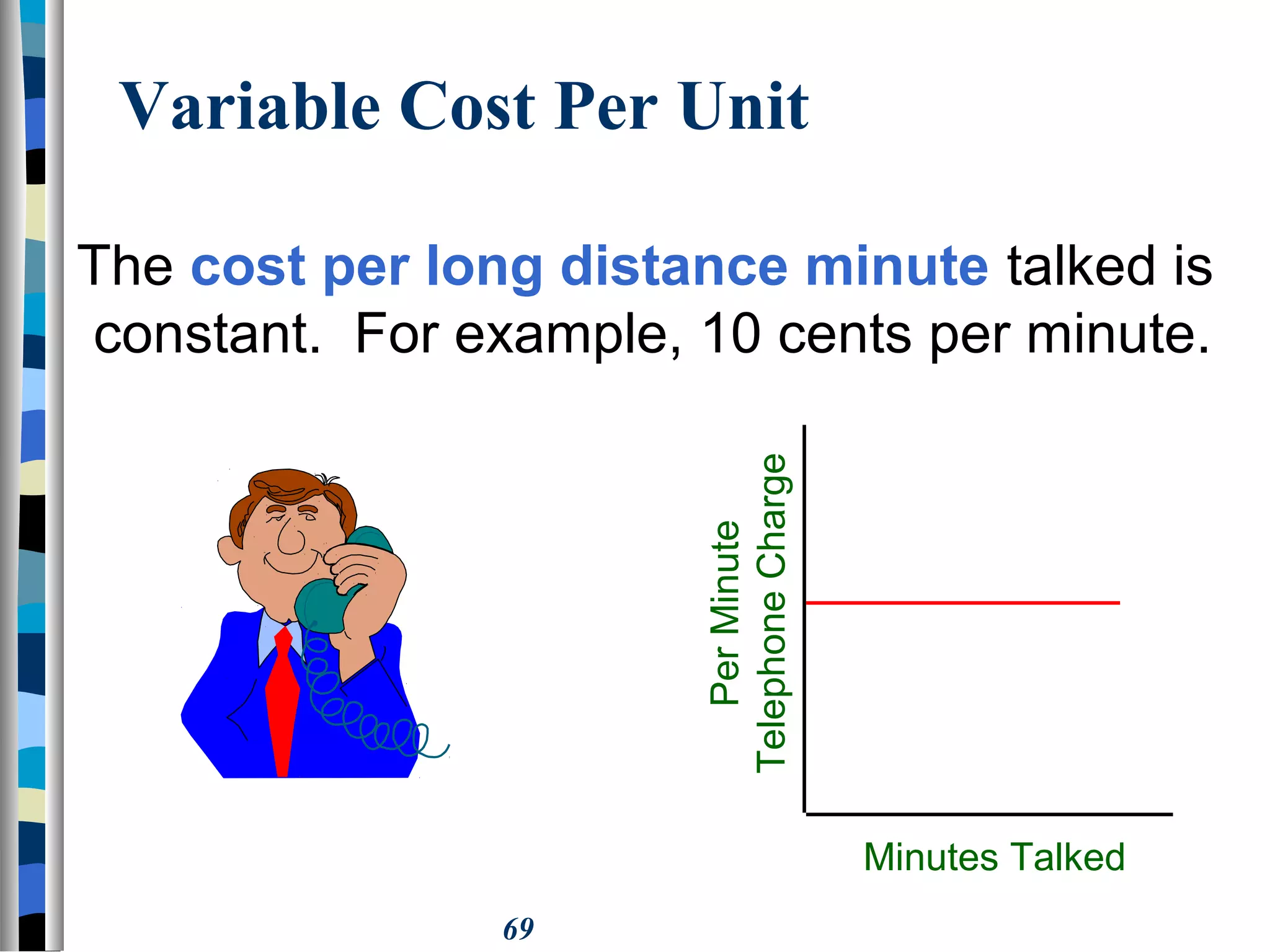

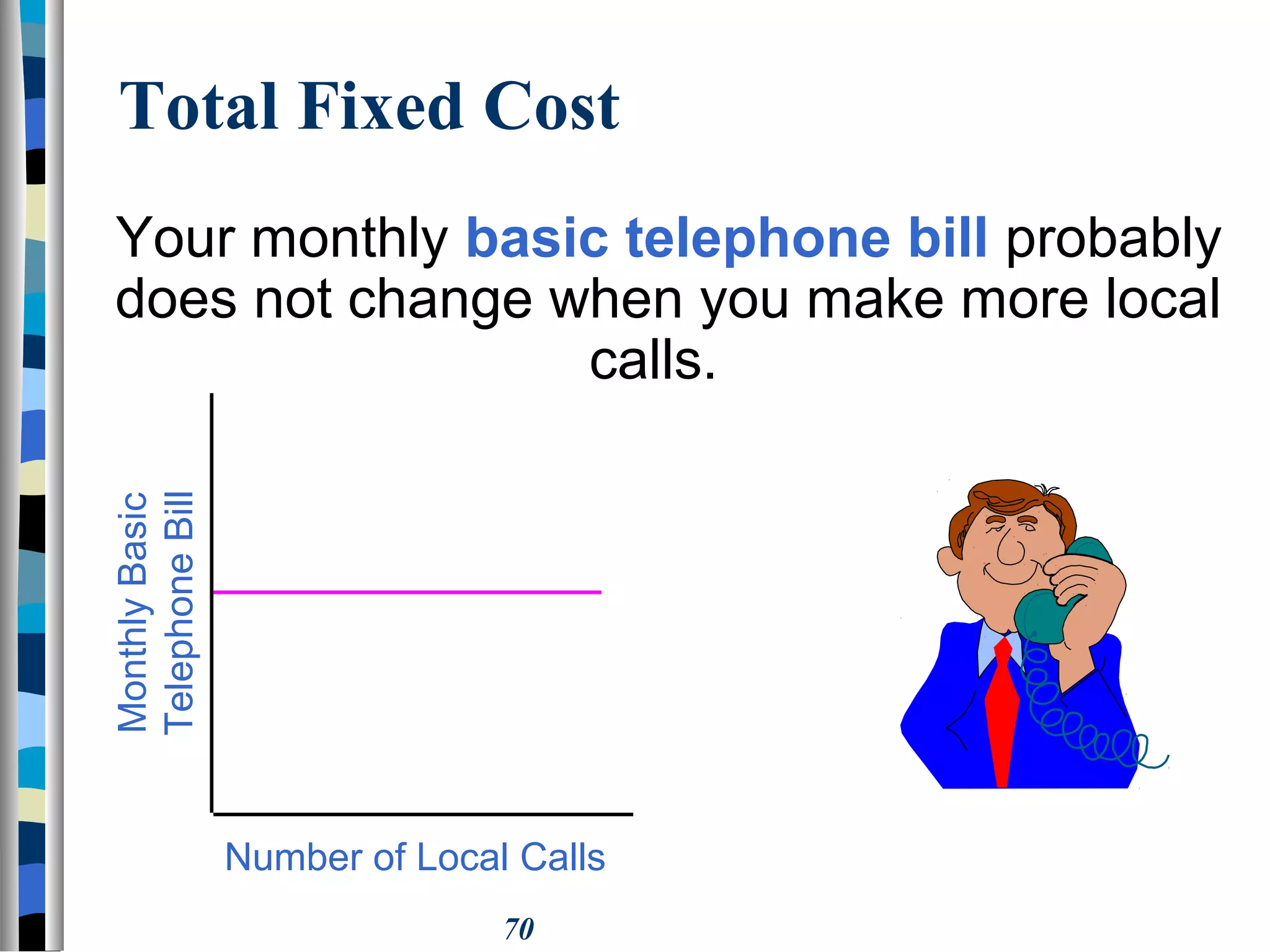

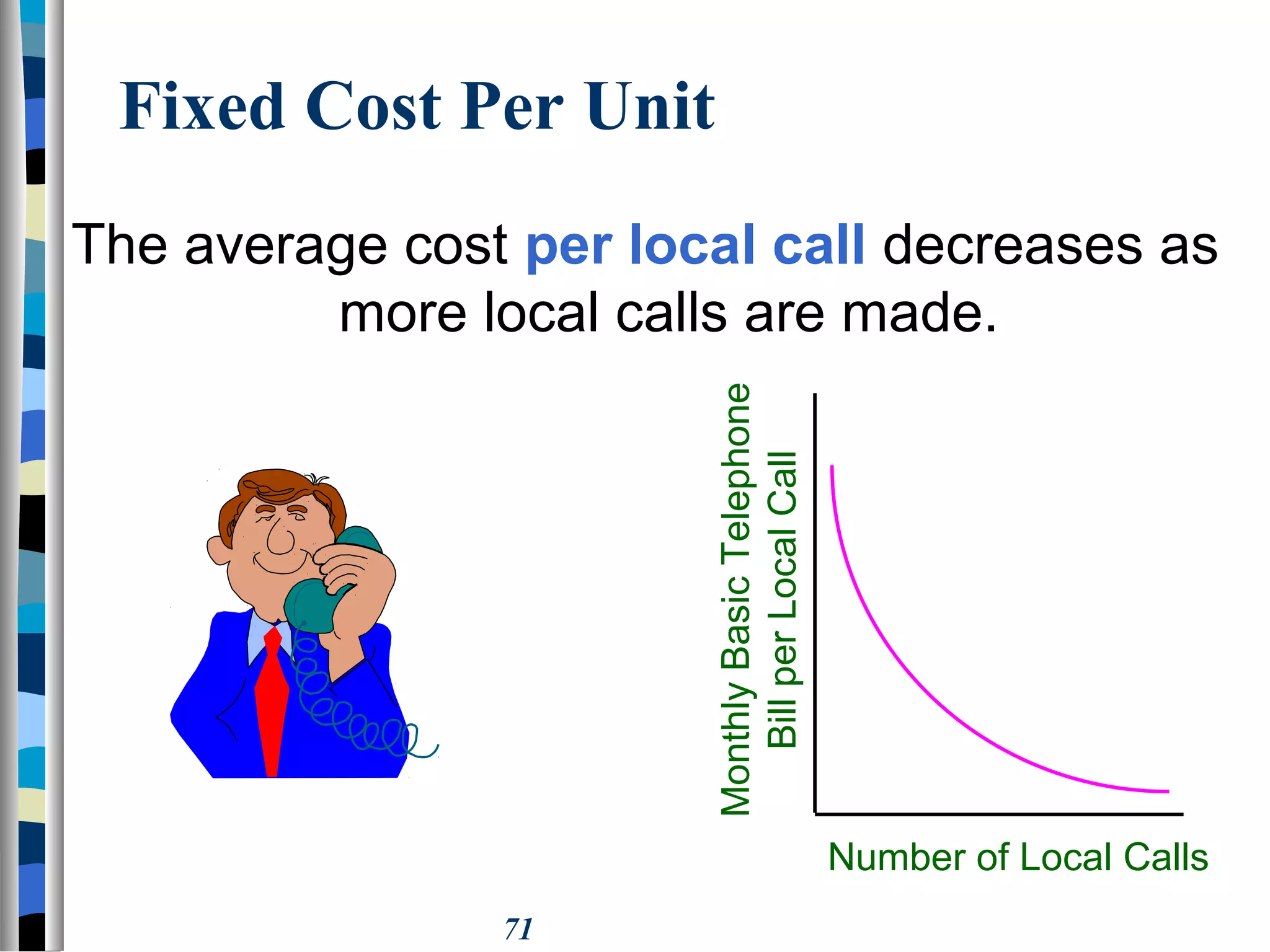

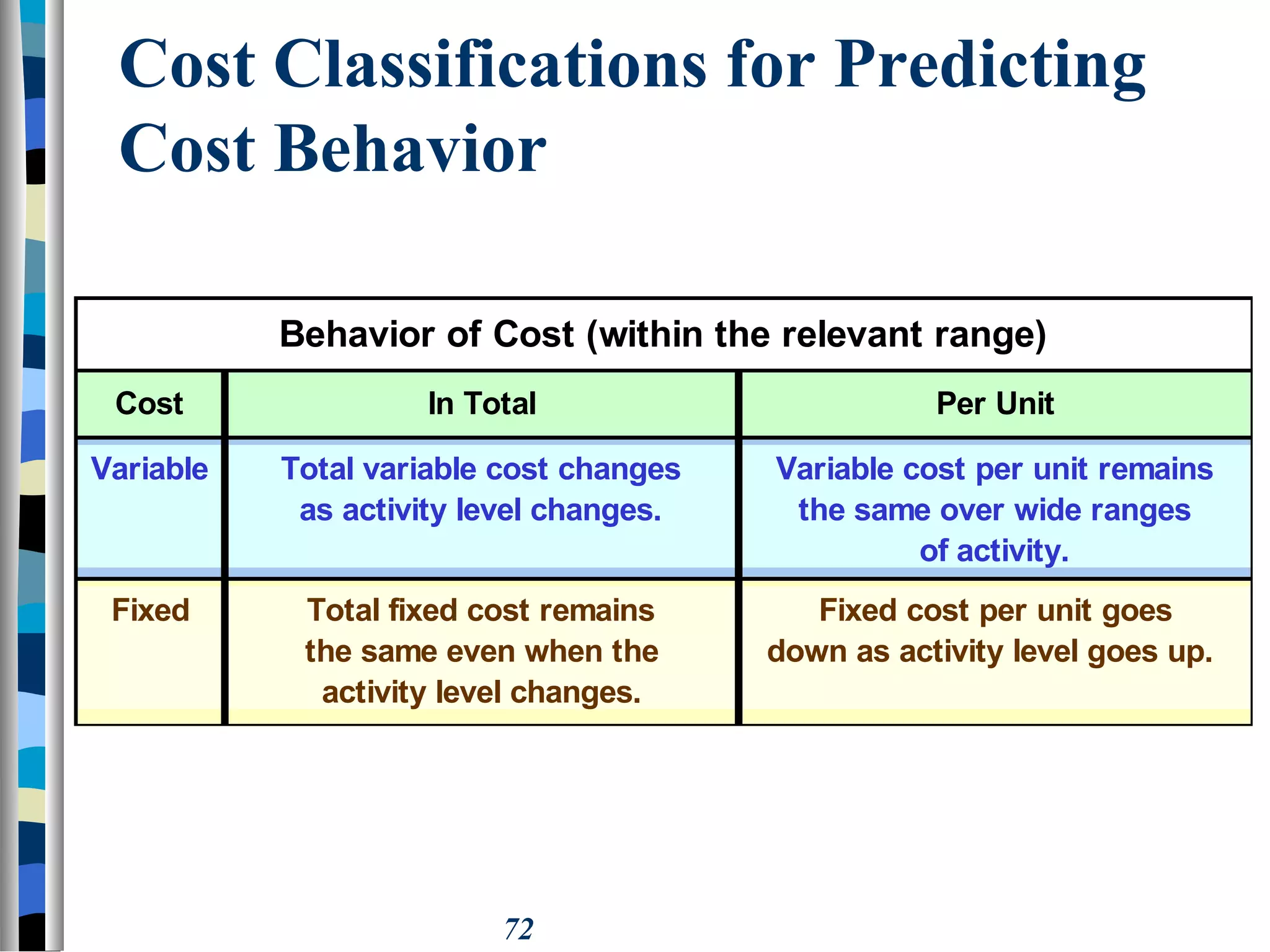

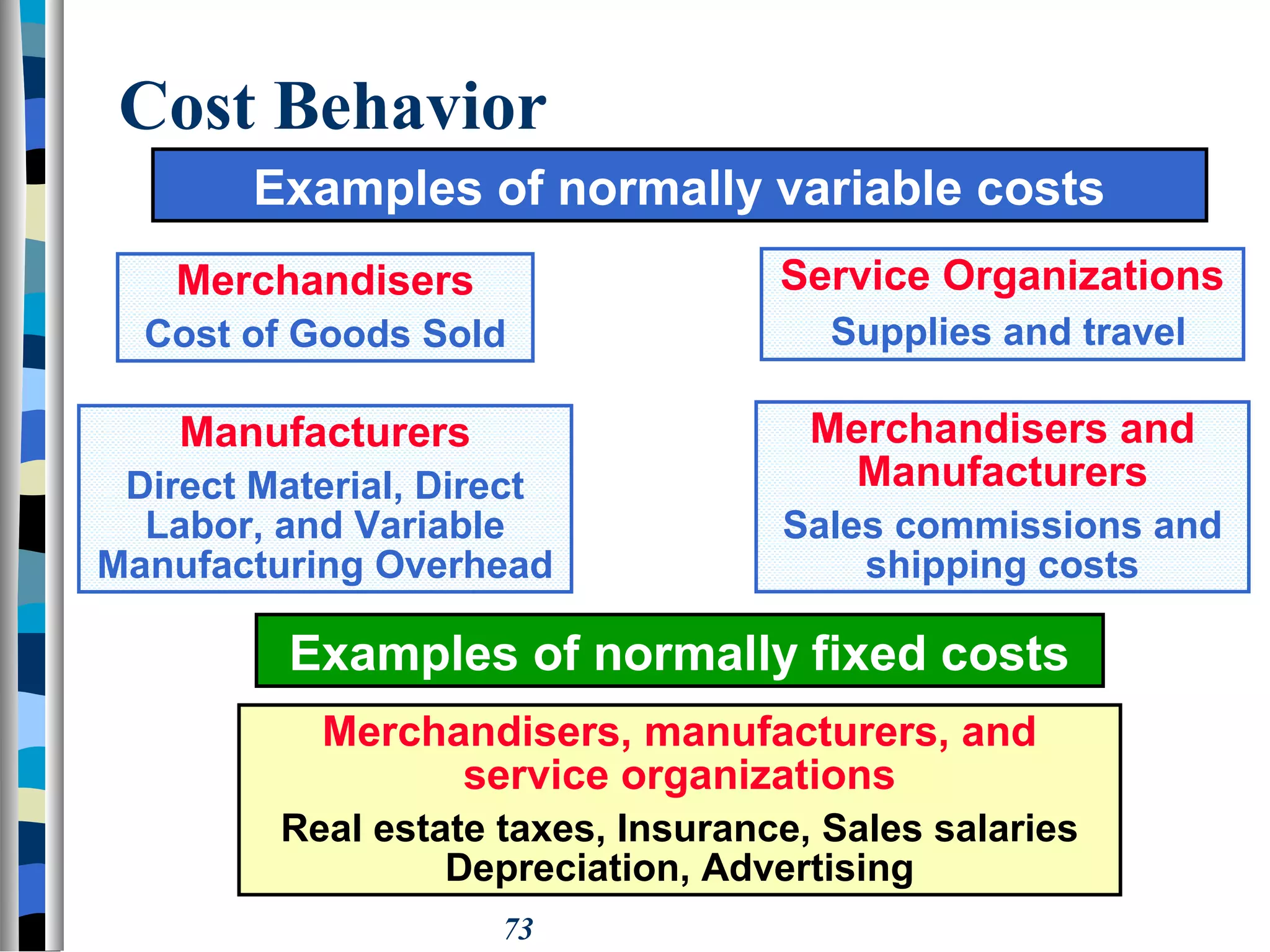

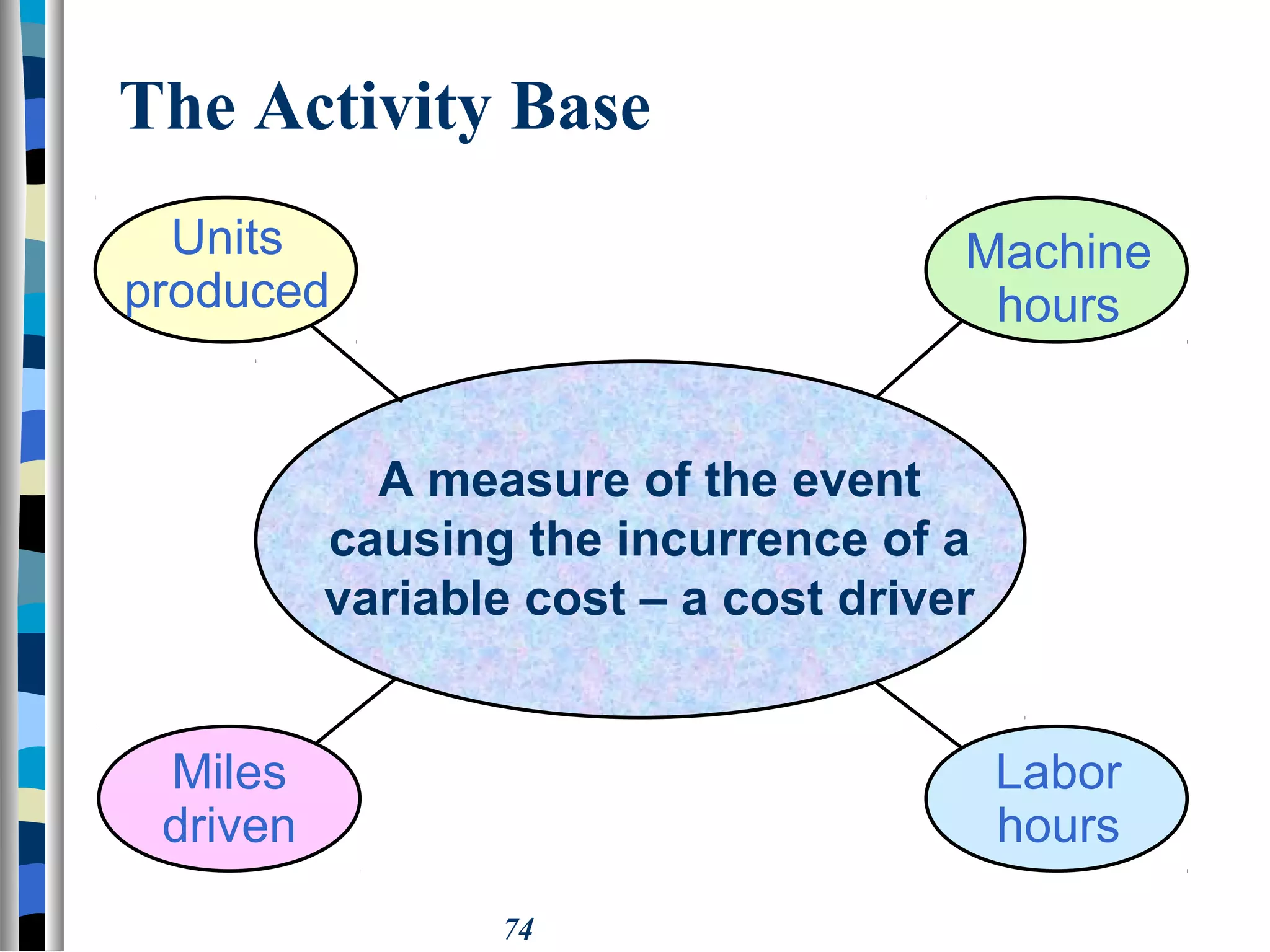

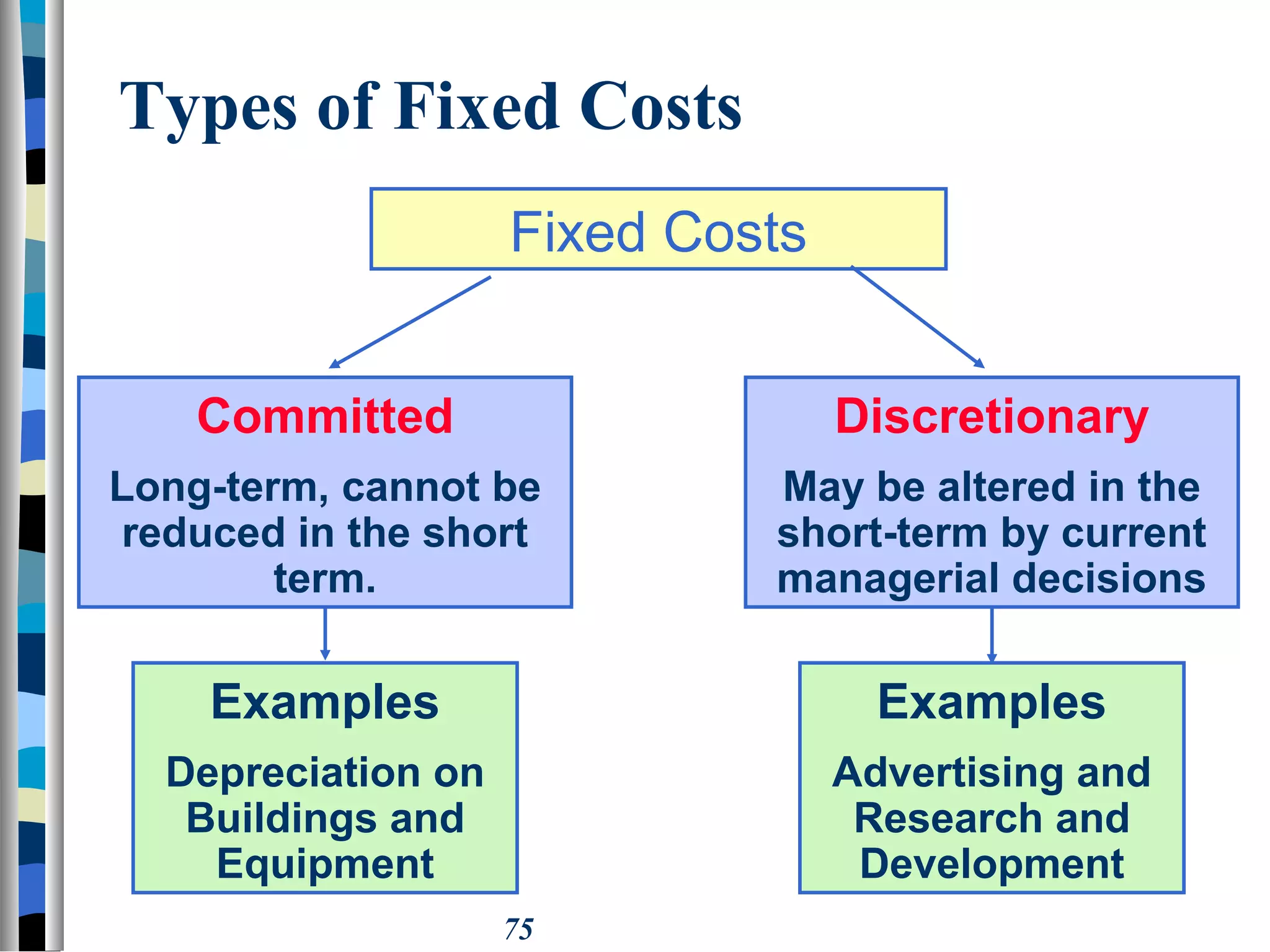

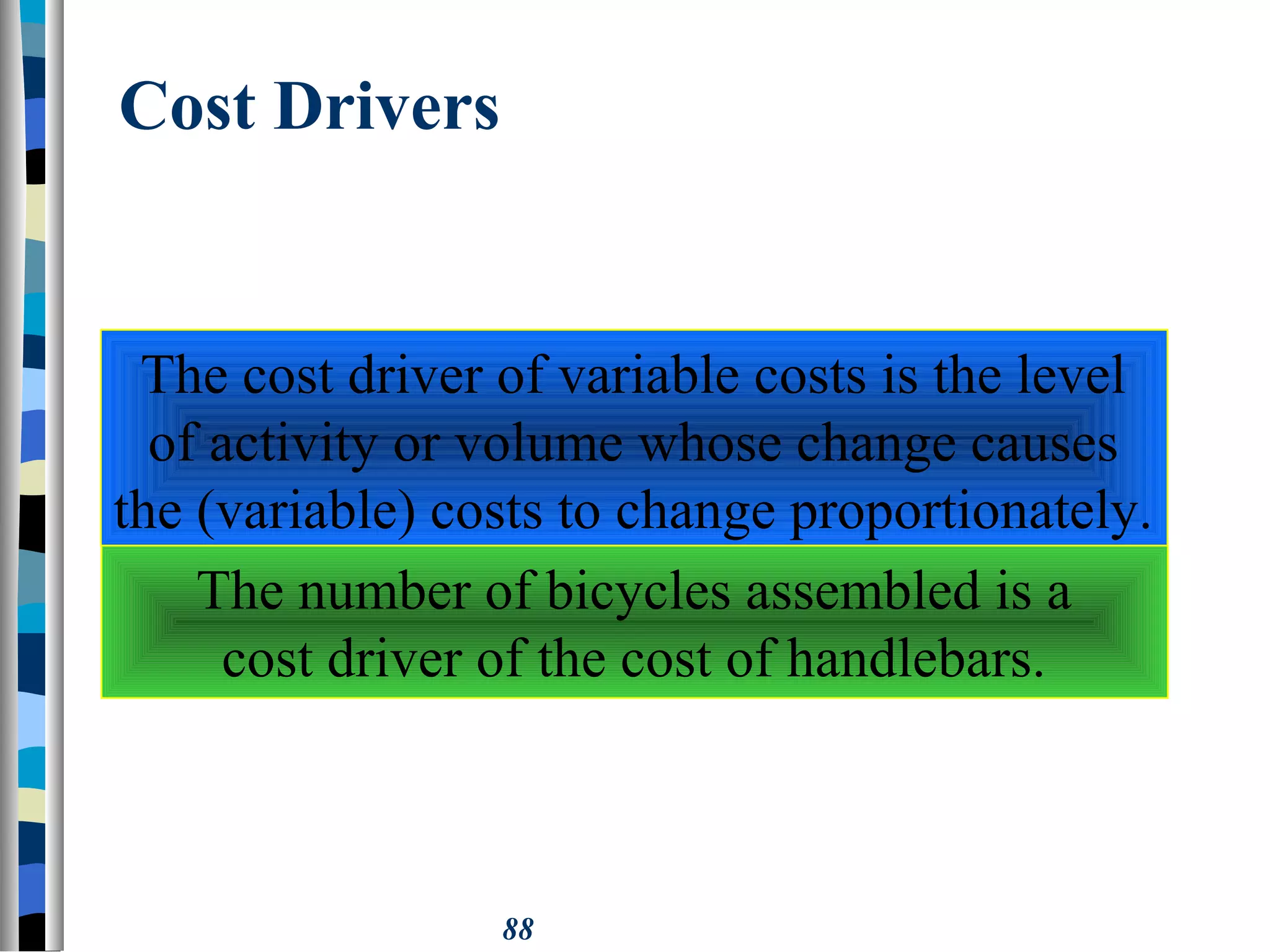

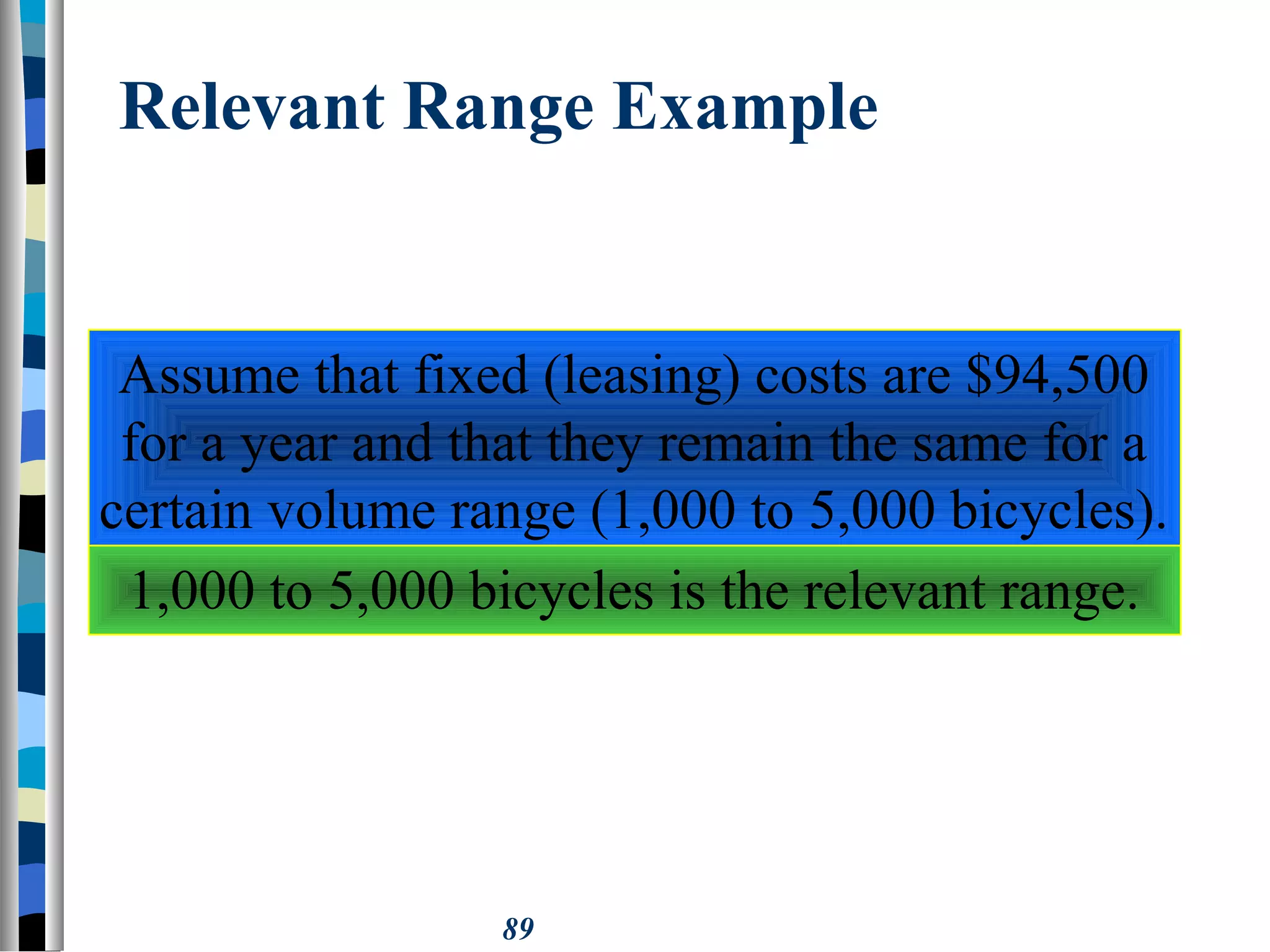

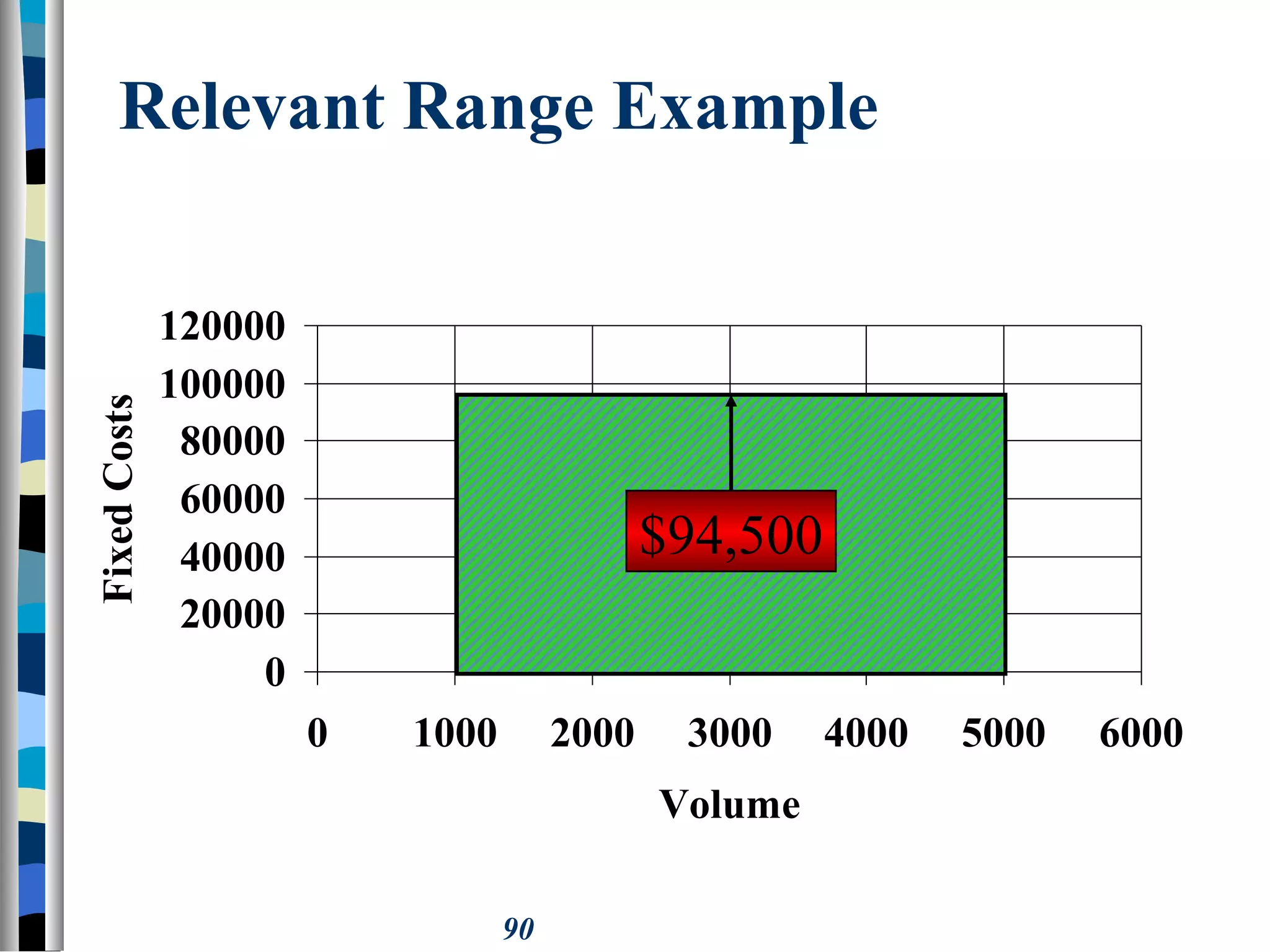

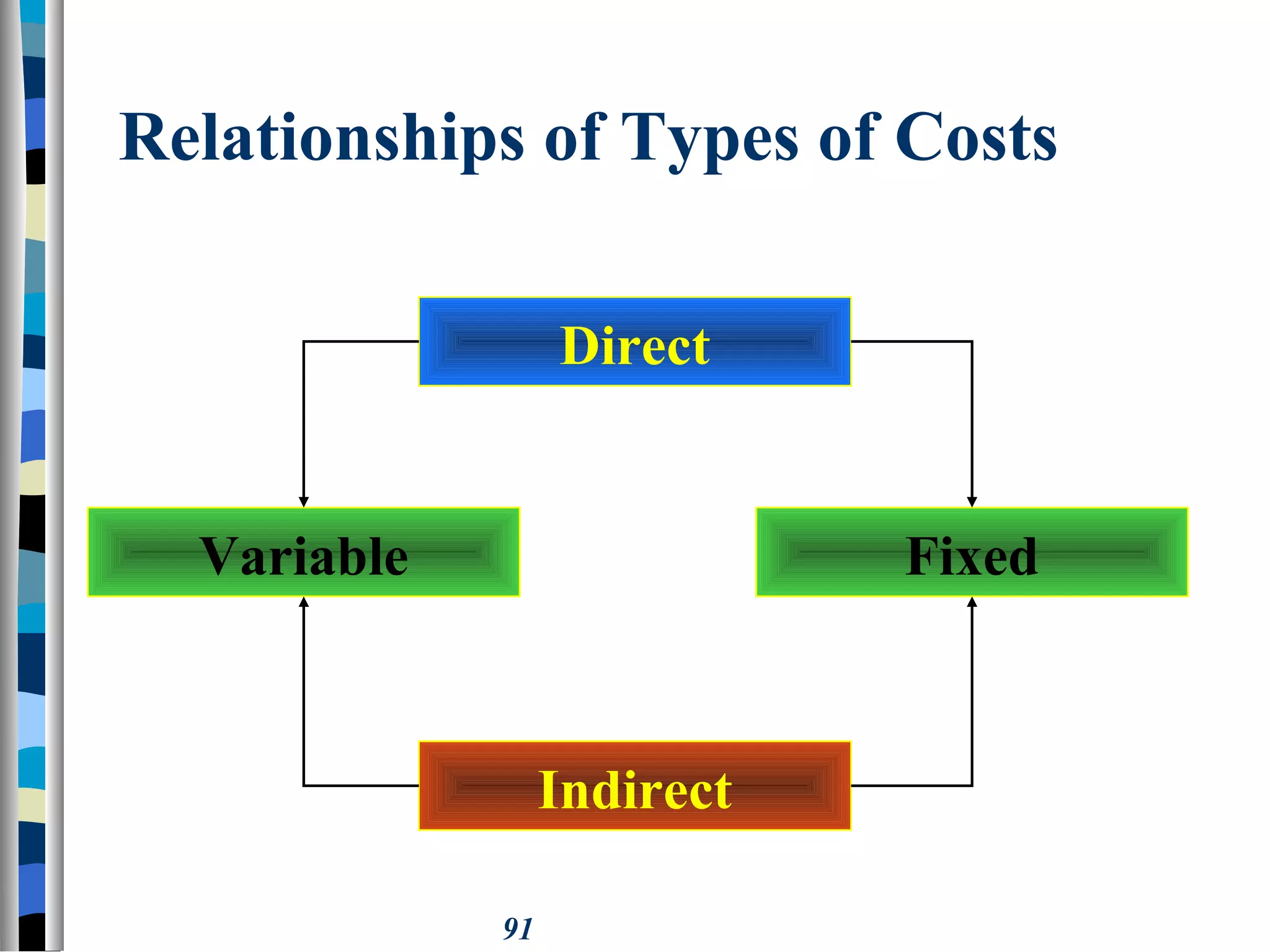

This document provides an introduction to managerial accounting and cost concepts. It defines key terms such as direct costs, indirect costs, product costs, period costs, cost drivers, cost behavior, and classifications of costs as either variable or fixed. Cost behavior is explained as how costs are affected by and change with business activity levels. Cost drivers are the specific activity measures that cause costs to change, such as labor hours or machine hours. Variable costs change directly with changes in the cost driver, while fixed costs remain unchanged within the relevant range of activity.