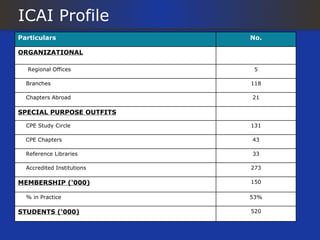

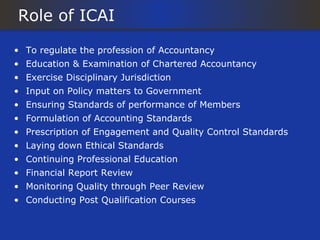

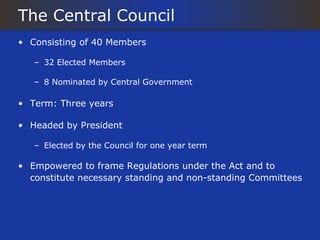

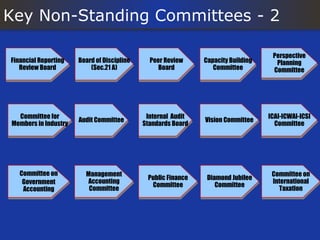

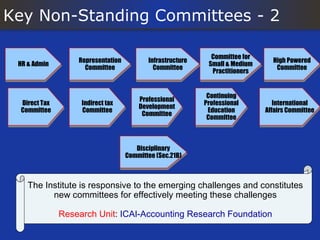

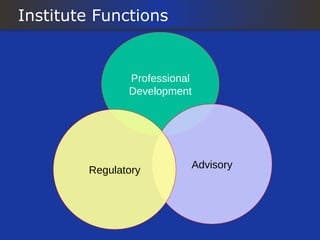

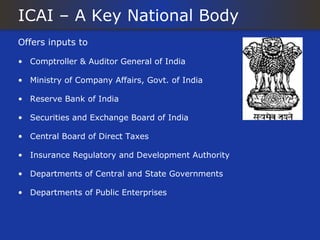

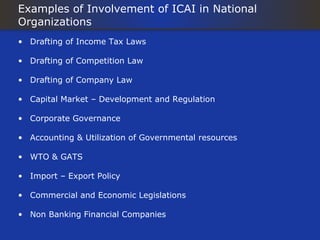

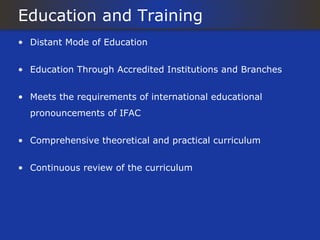

The Institute of Chartered Accountants of India (ICAI) was established in 1949 under the Chartered Accountants Act to regulate the profession of accountancy and provide education and training for chartered accountants; ICAI has over 150,000 members and 520,000 students and works to maintain accounting standards, provide continuing education and engage in other professional development activities; ICAI also aims to align Indian accounting standards with international standards and play an advisory role to the Indian government on financial and economic policy matters.

![The Institute of Chartered Accountants of India

[Set up by an Act of Parliament]

“ICAI Bhawan”, Indraprastha Marg, New Delhi – 110 002.

Phone: 91-11-39893989, 30110210

Website: www.icai.org](https://image.slidesharecdn.com/12927abouticaiindex-090704055604-phpapp02/85/About-ICAI-45-320.jpg)