Download to read offline

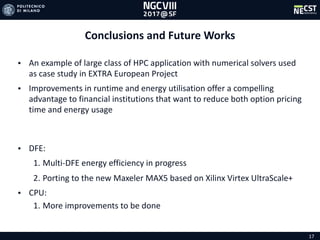

![16

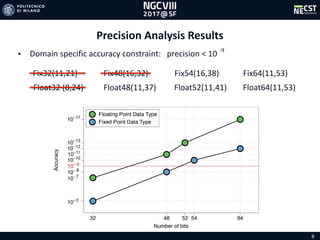

Speedups and Energy Efficiencies

s CPU 48 Cores Single DFE

DataSet30

DataSet780

Tabella 1-1

DataSet30 DataSet780

PU 1 Core 21 400

PU 24 Cores 7 36

PU 48 Cores 8 27

ingle DFE 5 6

s CPU 48 Cores Single DFE

DataSet30

DataSet780

Tabella 1-1-1

DataSet30 DataSet780

PU 1 Core 11 30

PU 24 Cores 7 36

PU 48 Cores 8 27

ingle DFE 11 12

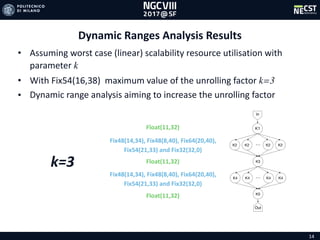

RunTime[s]

1

100

10000

CPU 1 Core CPU 24 Cores CPU 48 Cores Single DFE 8 DFEs

2,181

11,99

238,564240,017

3789,277

1,461,25

10,3310,49

158,81

DataSet30

DataSet780

SocketEnergy[Wh]

1

10

100

CPU 1 Core CPU 24 Cores CPU 48 Cores Single DFE 8 DFEs

8

6

27

36

400

55

87

21

DataSet30

DataSet780](https://image.slidesharecdn.com/asianoption5minpdf-170713144233/85/A-Scalable-Dataflow-Implementation-of-Curran-s-Approximation-Algorithm-16-320.jpg)

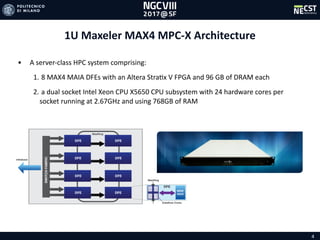

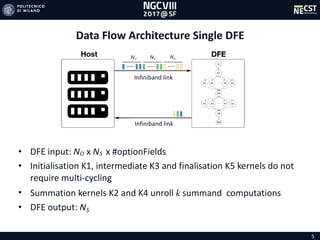

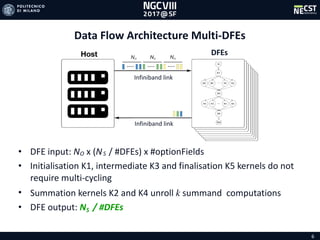

This document describes a dataflow implementation of Curran's approximation algorithm for pricing Asian options. The implementation computes the value at risk of a portfolio containing Asian options. It supports an arbitrary number of averaging points and achieves high precision using fixed-point arithmetic. Experimental results show that a single Maxeler dataflow engine can price portfolios over 10 times faster than a 48-core CPU. Further optimization including multi-DFE processing and porting to newer FPGA hardware could improve energy efficiency and performance.

![[Seminar] hyunwook 0624](https://cdn.slidesharecdn.com/ss_thumbnails/seminarhyunwook0624-200725001151-thumbnail.jpg?width=640&height=640&fit=bounds)