Download to read offline

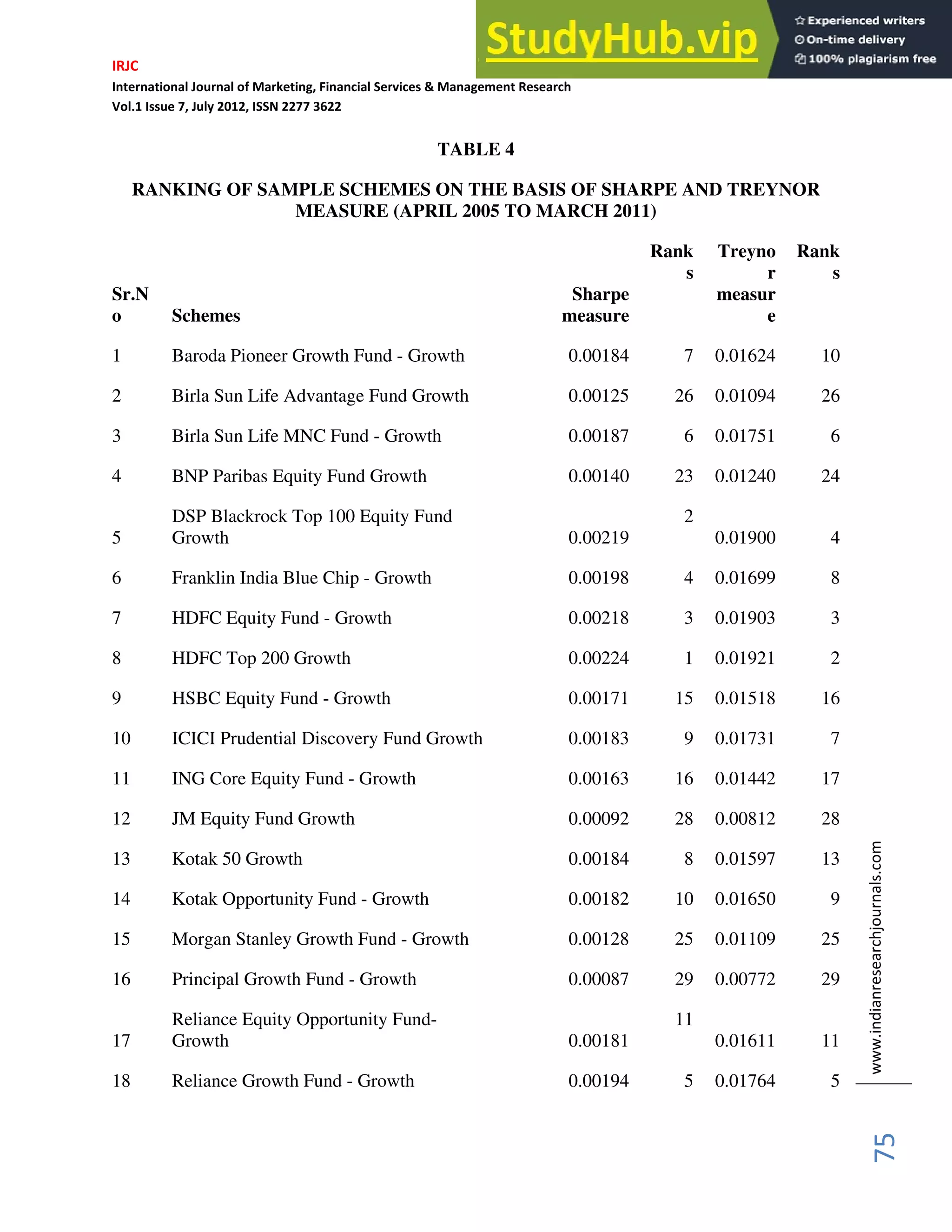

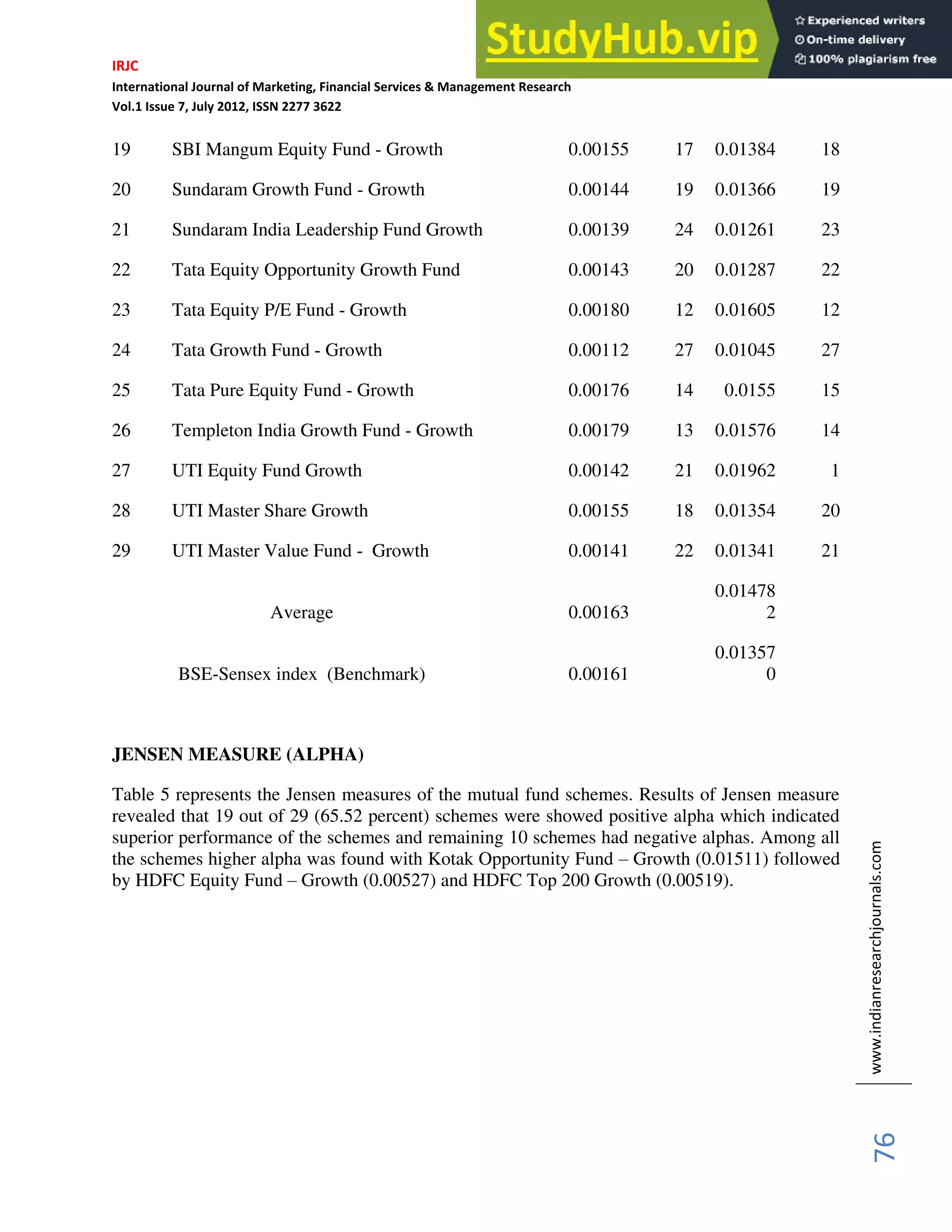

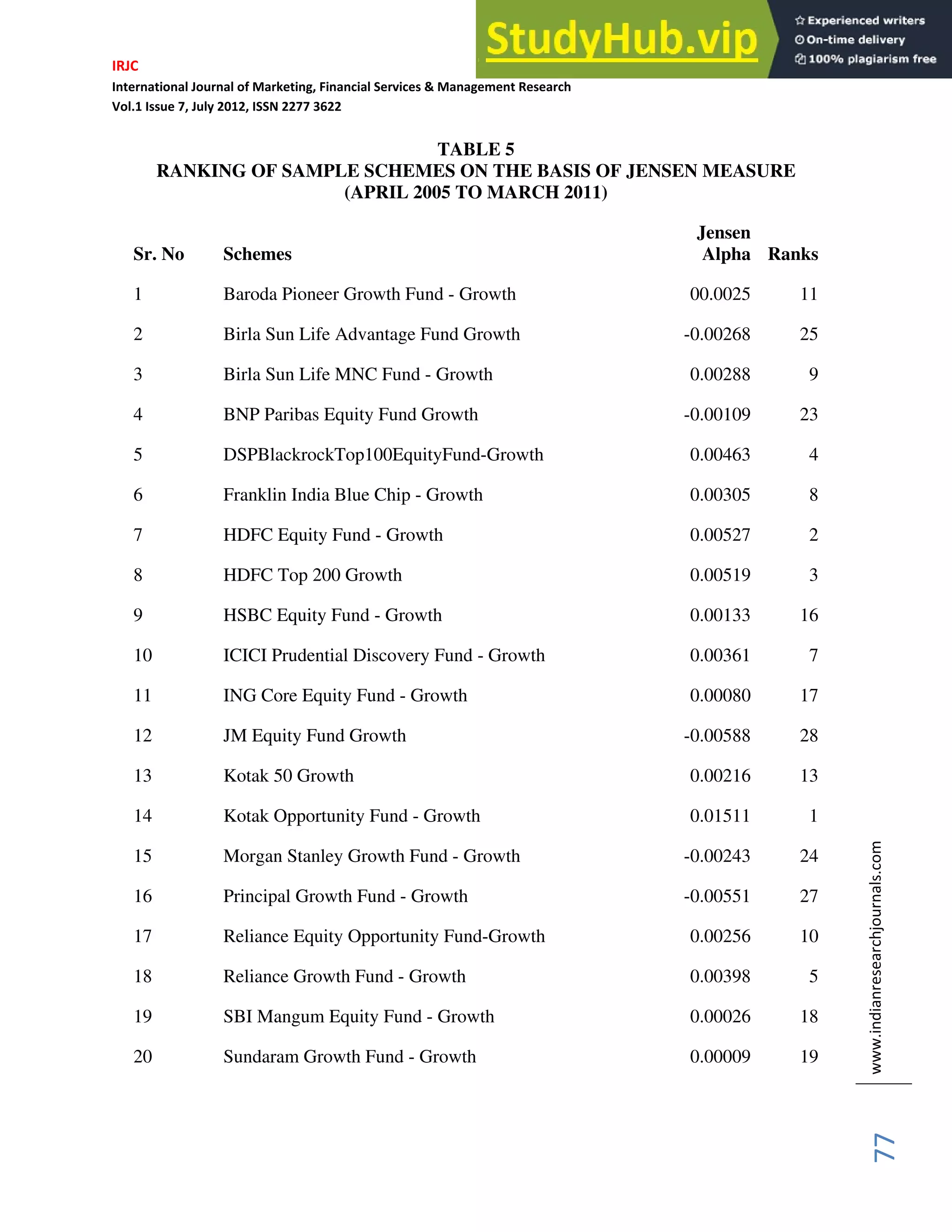

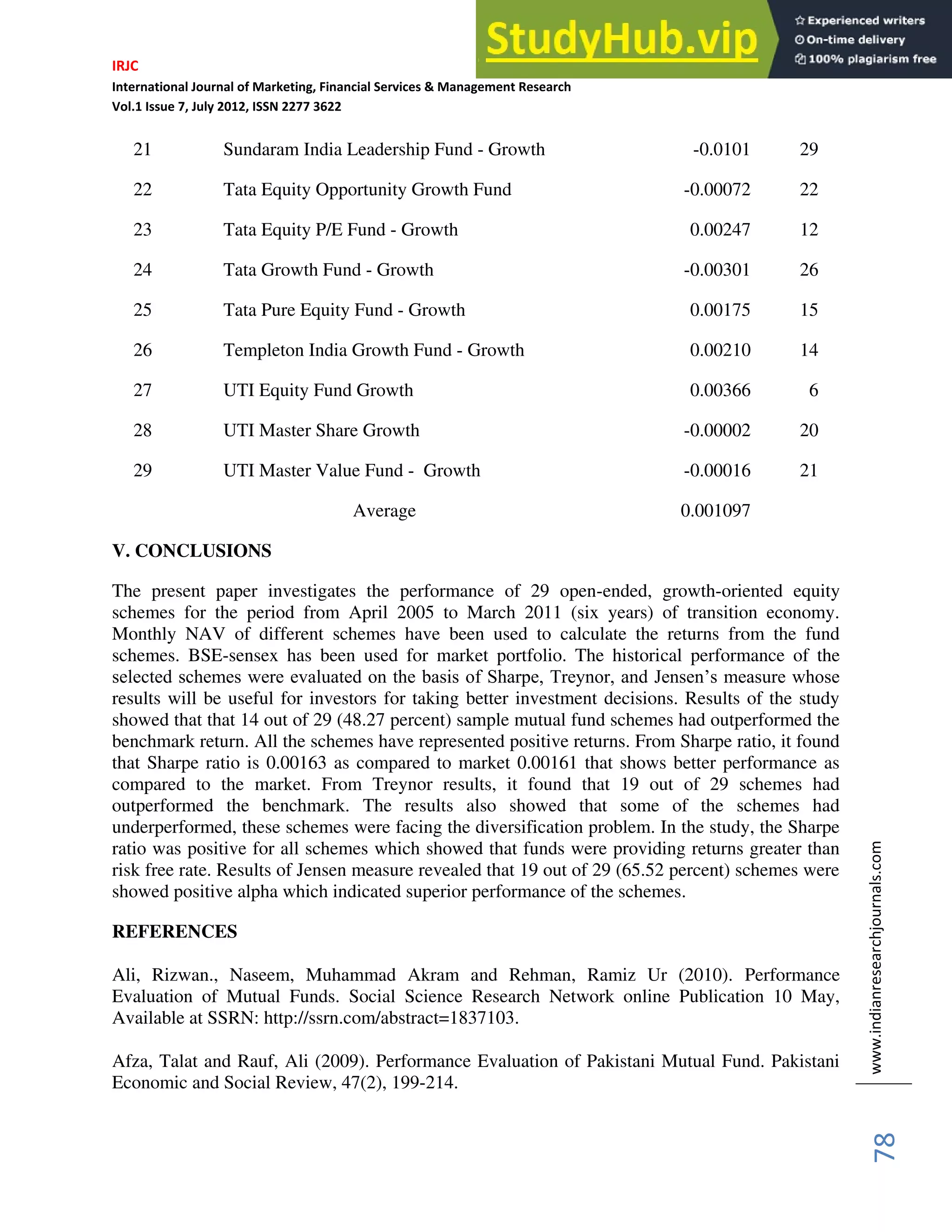

This document analyzes the performance of 29 Indian mutual fund schemes from April 2005 to March 2011 using various measures. It finds that 14 of the 29 schemes (48.28%) outperformed the benchmark index. The Sharpe ratio was positive for all schemes, indicating returns higher than the risk-free rate. Jensen's alpha was positive for 19 schemes (65.52%), showing superior performance. The study uses monthly net asset values to calculate returns and the BSE Sensex as the market portfolio for comparison. Various risk-adjusted return models like the Sharpe, Treynor, and Jensen measures are employed to evaluate the historical performance of the selected mutual fund schemes.